-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Market Brief

The articles are produced in Chinese only.

Author

倪國權先生 (Alex Ni)

助理經理

曾任職鋼材交易員及廣告公司主任,所以特別喜歡研究資源類及消費類股票。歡迎來電賜教或交流心得。

Phone:

22776779

Email:

alexni@phillip.com.hk

助理經理

曾任職鋼材交易員及廣告公司主任,所以特別喜歡研究資源類及消費類股票。歡迎來電賜教或交流心得。

Phone:

22776779

Email:

alexni@phillip.com.hk

TANG PALACE (CHINA) HOLDINGS.LTD (1181.HK)

Tuesday, November 6, 2018  4300

4300

Stock Commentary Date: 05/11/2018

Stock: TANG PALACE (CHINA) HOLDINGS.LTD (1181.HK)

Closing price: $1.15 (04/11/2018)

52 weeks range: $1.09 – 1.891

Shares outstanding: 1,068,617,500

Market Capitalization : HK$ 1229 Million (04/11/2018)

Target Price (12 months): Neutral

Business Summary:

1. Tang Palace (China) Holdings Ltd. is an investment holding company engaged in the restaurants operation. The company operated through its own brands as well as through franchising.

2. The brands operated by the Company include: Tang's Cuisine (唐宮壹號),Tang's Palace (include Tang Palace Seafood Restaurant and Tang Palace, 唐宮 包括唐宮海鮮和唐宮),Social Place (唐宮小聚),Canton Tea Room (唐宮茶點)and Ninja House Japanese Restaurant (忍者居)。The company also operated franchise brand “Pepper Lunch” and formed a partnership with their Malaysia business partners to operate “PappaRich” (金爸爸).

3. The company operated 58 restaruants and 6 other restaurants under joint ventures (as on 30 June 2018). The company mainly operated through three business segments: the Southern China region, the Eastern China and the Northern China region. The largest section was in Eastern region

Business Report:

1. For the six months ended 30 June 2018, revenue of the Group increased by RMB 80.4 million or 12.2%, to RMB 740.2 million as compared to the same period 2017. Although the Group managed to increase the revenue in this competitive industries, the rising cost affected the company's profit. Net income decreased by 15% RMB 53.16 million.

2. The Group's Southern China segment and Western China segment performed well in the first half of 2018 due to its strategic change and reflected on the Group's revenue, revenues were increased by 26% to RMB 192.9M and 96% to RMB 45.6M respectively. While Northern China as well as Eastern China segment revenue grew by 6% to RMB 199 million and 3% to RMB 329 million. The Group's net income decrease was also contributed by the 35% drop in net income with the Eastern China Segment.

3. The Group's largest cost were inventories consumed (which includes food consumables, utensils etc) and staff. In the first half of 2018, both items increased by 17% and 18%, from RMB 232 million to RMB 273 million and RMB 191 million to RMB 227 million respectively.

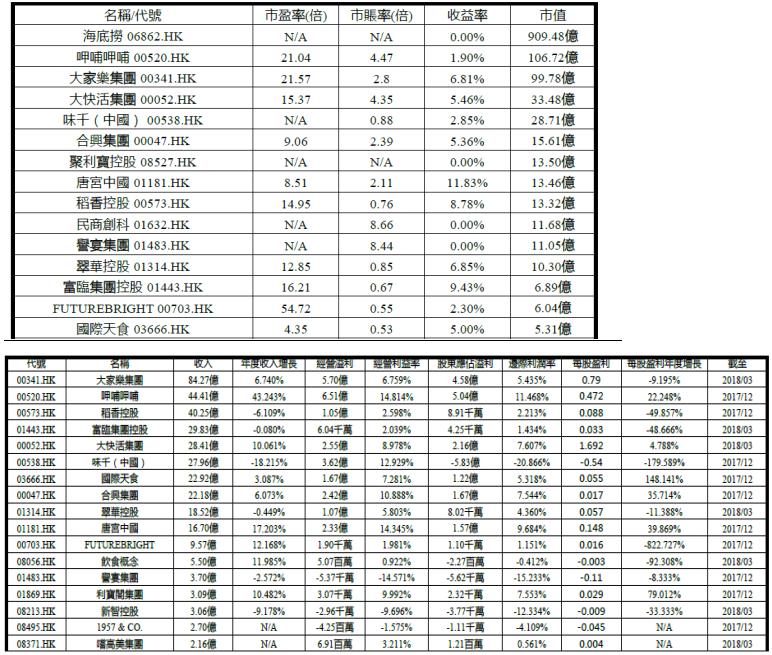

Peer Comparison:

SWOT ANALYSIS:

Strength :

- China's catering service market generated approximately RMB 4000 billion revenue in 2017. It is expected this sector to continue to grow at a CAGR of 9.6% from 2017 to 2022.As for Hong Kong, the market generated approximately HKD 107 billion in revenue in 2016 and expected to grew by a moderate CAGR of 4.7% from 2016 to 2021.The focus is clearly in China

- The company recognised the rapid growth in the online takeway business and formed a close relationship with various platforms such as waimai baidu (百度外賣), daojia.com (到家美食), ele.me (餓了麼) and meituan.com (美團網) in order its online sales.

Weakness :

- Lack of brand diversification

.

Opportunities :

- Online take away business.

- Sales of convenient dishes thru online store, “WeiMall”

Threat :

- Rising staff as well as basic materials

- Slowdown in economy due to trade war, which in turn slowdown consumption.

「註:本人倪國權為證監會持牌人士。截至本評論文章發表日止,本人及/或其有聯繫者並無持有全部提及之証券的所有相關財務權益。」; Or

” I, Ni Kwok Kuen Alex, am a licensed person under the Securities and Futures Commission. Until the date this commentary was published, neither I and/or my affiliates are the beneficiary of the securities mentioned herein or are entitled to any financial interests in relation thereto. “

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()