-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Tianqi Lithium (002466.CH) - Darkness before Dawn

Monday, November 11, 2019  9670

9670

Tianqi Lithium

| Recommendation | Accumulate |

| Price on Recommendation Date | $28.040 |

| Target Price | $32.000 |

Weekly Special - 3306 JNBY Design Limited

Investment summary

Results in the First Three Quarters Fell Sharply

In the third quarter of 2019, Tianqi Lithium reported a revenue of RMB1.2 billion, down by 18.3% yoy. The net loss attributable to shareholders was RMB53.92 million. The net loss excluding non-recurring items was RMB93.09 million. In the first three quarters, Tianqi Lithium accumulatively reported a revenue of RMB3,797 million, down by 20.2% yoy. The net profit attributable to the parent company was RMB139 million, down by 91.7% yoy; the net profit attributable to parent company excluding non-recurring items was RMB15.5 million, down by 99% yoy. Meanwhile, the Company released its result guideline in 2019. The annual net profit attributable to shareholders ranged from RMB80 million to RMB120 million, down by 96%-94.6% yoy. This means that Tianqi Lithium will record a net loss of RMB19-59 million in the fourth quarter.

The Company's Financial Statements Were Hit by the Decline in Lithium Prices and the Financial Expenses Incurred by Asset Acquisition

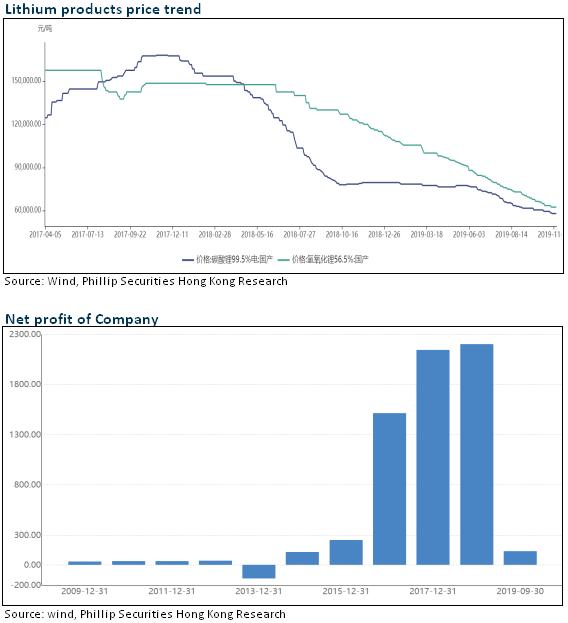

The market price of the Company's main products, battery-grade lithium carbonate and lithium hydroxide, has been going down all the way since 2018. In the third quarter of this year, their average price was approximately RMB66,000 and RMB75,000 per ton, a significant decrease of 33-44% compared with the average price of RMB97,000 and RMB135,000 in the same period last year. Dragged by this, the gross margin of the Company's products has dropped from a record high of 73.7% in the first quarter of 2018. The gross margin of the Company in the first three quarters of this year was 61%, 61% and 53%, respectively, down by 12.6 ppts, 10.3 ppts and 11.5 ppts yoy.

The Company invested USD4.07 billion in the acquisition of SQM's equity, which generated USD3.5 billion in debt. Long-term borrowings rose from RMB1.88 billion in the same period last year to RMB28.2 billion. The net liability ratio reached 266%. The financial expenses for the first three quarters were as high as RMB510 million, RMB500 million and RMB640 million. The financial expenses for the single quarter were higher than the RMB470 million for the whole year of 2018. The main reason for the Company's result setback is the surge in financial expenses incurred by asset acquisition.

In addition, the result of SQM after the acquisition did not meet expectations, which reduced the Company's return on investment quarter by quarter. The return on investment in the first three quarters was RMB139 million, RMB94 million and RMB77 million, respectively.

Stock Placement Was Approved, which may Reduce Financial Pressure

The Company's stock placement has been approved by the China Securities Regulatory Commission. The shares will be placed to all shareholders in proportion of 3 shares for every 10 shares. The Company plans to raise no more than RMB7 billion, which is intended to be used to repay the annexation loan for the purchase of SQM equity. In addition, the Company plans to use multiple financing modes including short-term and medium-term bills, USD bonds and convertible bonds to buffer the pressure from repayment of principal and interest of the annexation loan and reduce financial expenses. If the fundraising is successful, the Company's financial pressure will be effectively buffered.

Benefited from the recovery of the supply and demand structure, Lithium prices are expected to bottom out

Currently, the price of lithium carbonate is below RMB60,000 per ton, which is lower than the cost line of many companies. The industry is on the eve of high-cost capacity clearing. On the demand side, the power battery will usher in the peak season in the short term. In the medium and long term, the new European emission standards and the electric vehicle subsidy policy will support the demand for raw material lithium. In general, the future decline of lithium prices is limited, and the upward elasticity will gradually emerge.

As a leading enterprise with high-quality resources, Tianqi Lithium is expected to continue to benefit from the volume and price recovery brought by the acceleration of global electrification by virtue of the technological and scale advantages. The Company's Phase I of lithium hydroxide project of 24,000 tons in Kwinana is expected to enter the continuous production and capacity improvement by the end of the year; the Phase II expansion of Talison has been commissioned. The operation was initiated in an all-round way.

Valuation and Investment thesis

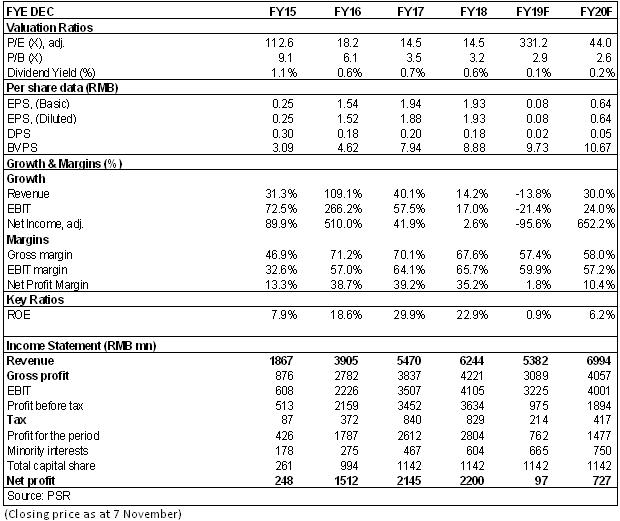

Tianqi Lithium not only holds shares of companies with the world's largest scale and best lithium ore resources in production, but also has the world's largest processing capacity on extracting lithium from ores, which make Tianqi Lithium the best investment object in upstream sectors of domestic new energy vehicle industry chains. We expected diluted EPS/BVPS of the Company to RMB 0.08/0.64 and 9.73/10.67 of 2019/2020. And we accordingly gave the target price to 32, respectively 3.3/3.0x P/B for 2019/2020. "Accumulate" rating. (Closing price as at 7 November)

Risk

New business progress slower than expected

Lithium series Product price falling

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()