-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CEB GREENTECH (1257. HK) - Performance meets Expectations and the Strong Growth of Biomass

Friday, March 9, 2018  13173

13173

CEB GREENTECH(1257)

| Recommendation | Buy |

| Price on Recommendation Date | $7.790 |

| Target Price | $9.360 |

Weekly Special - 3306 JNBY Design Limited

Summary of Investment

- The annual result is in line with expectations and the growth momentum of biomass is strong;

- Strong project expansion ability and efficient operation and management;

- Benefiting from government support, the industry remains booming;

Investment Rating

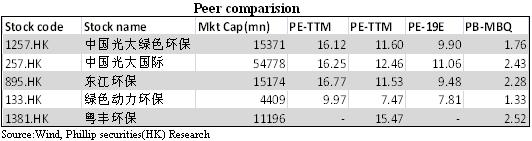

Based on the business layout, the company founded three management centers, including clean energy, solid waste and environmental restoration. While consolidating existing main business, the company actively enhances natural gas, soil, soil remediation to brew a new growth point. Based on the fundamentals of good quality and the boom of the biomass and hazardous waste industry, we expect the net profits attributable to the parent company in 2018-2019 will reach HKD1345 / 1680 million, and the EPS will be HKD0.65/0.81, equivalent to the PE of HKD12.0 / 9.6, respectively. The target price of HKD 9.36 and an Buy rating is given. (Closing price as at 7 March 2018)

The Annual Result Achieved Amazing Growth

According to the 2017 full-year result announcement, CEB Greentech recorded a revenue of HKD4,581 million, up by 52.7% yoy, EBITDA was HKD1,518 million, up by 54.4% yoy, and the profit attributable to shareholders was HKD954 million, up by 51.6% yoy. The EPS was HKD0.52. The final dividend was Hong Kong 9 cents per share. The result growth is consistent with our previous expectations.

The overall gross margin was 31.32%, down by 1.73% yoy, which was mainly due to the increased proportion of the biomass business with lower gross margin, and the net profit margin was 20.87%, basically unchanged from the same period of last year. The administration expense ratio was 5.16%, decreased by 1.42pct yoy. The financial expense ratio was 2.74%, up by 0.49% yoy.

The company continued to increase cash to HKD3,343 million, increased by HKD2,351 million compared with that in the end of the previous year. The asset-liability ratio was 39%, down by 5pct compared with that in the end of the previous year, and the current ratio was 2.16, which was 0.94 higher than that in the end of the previous year, and the amount of outstanding financing was still HKD3.56 billion. Abundant funds and sound financial structure provide a solid guarantee for subsequent expansion.

The Growth Momentum of Biomass Business is Strong

The continuous increase of total processing capacity drives the continuous growth of operation revenue. In 2017, the aggregate on-grid electricity was about 1,393GWH, up by 125% yoy. The company processed 1.68 million tons of biomass raw materials, an increase of 131% yoy, and processed 249,000 tons household garbage, up by 239% yoy. The increase of total processing capacity drives the increase of the company's operation revenue. The revenue from operation services was HKD1,549 million, up by 69% yoy. Revenue accounted for 34% compared with the previous year's 30.5%. The revenue from construction services was about HKD2,953 million, up by 44% yoy. The revenue proportion decreased from 68% to 64%. Revenue structure has slightly improved.

Biomass grows fast and contributes main source of income. The annual revenue from biomass was HKD3.994 billion, up by 63% yoy, accounting for 87% of the total revenue. The revenue from biomass operation services increased by 124% yoy to 1.03 billion, while the yield of biomass construction services increased by 47.3% yoy to 2,893 million. Due to the small number of current projects, the revenue of the hazardous waste treatment business increased by 12.7% yoy to 378 million, while the revenue from solar energy and wind power project operation services was 209 million (-2.8%).

Steady Progress has been Made in Project Acquisition and Construction

New breakthroughs have been made in market development. In the last year, the company has newly obtained 19 projects and 1 copy of the supplementary agreement, involving investment of HKD5,473 million, including 9 biomass and waste integration projects, 3 biomass electricity and heat cogeneration projects, 7 hazardous waste treatment projects; the newly added biomass processing capacity was 2.1 million tons/year, the new household waste treatment capacity was 2,000 tons/day, and the new hazardous waste designed processing capacity was 170,000 tons per year. Among other things, Zhejiang Lishui industrial solid waste comprehensive treatment project (hazardous waste processing capacity of 7,000 tons/year), was the first project the company obtained in Zhejiang province. It marked the company's breakthrough of business development in new areas. As at 2017, the aggregate biomass material processing designed capacity was 8.45 million tons/year, aggregate household waste processing designed capacity was 6,250 tons/day, and hazardous waste treatment capacity was about 674,000 tons/year. All the business processing scales are at a record high.

Steady progress has been made in the construction of the project. As at the end of the period, the company had 36 completed projects, and the amount of investment was about HKD7,291 million. In addition, 11 construction projects of investment about HKD3,513 million are expected to be completed and put into operation in 2018 and the first half of 2019. The company has 35 projects under preparation with about HKD8,954 million investment, and rich project reserves to boost future growth.

Clear Business Layout and Outstanding Competitive Advantage

The company develops the unique business model of biomass material + rural household garbage integration, which is the only company that operates the integrated mode of biomass and garbage generation in China. Through planning on agricultural and forestry waste and the rural living garbage as a whole, the company satisfies the environmental protection requirements of the government at all levels, and can effectively reduce the overall development and operation costs, highlighting the competitive advantage in business expansion.

Biomass power generation low nitrogen combustion technology of the company has made significant breakthrough. The technology can make the biomass power generation project nitrogen oxide (NOx) emission concentration below 100mg/m3, and has run stably for a long time in Nanqiao and Dingyuan biomass direct combustion project implementation. The successful application of this technology will make the company's biomass power generation project operation level reach the domestic leading level. We believe that the company will increase technological innovation and build technical barriers, which will help consolidate and expand its competitive advantage and enhance its core competitiveness.

Risk Warnings

Risks of macroeconomic and environmental policy changes;

Intensified risks in industry competitions;

Project construction progress is lower than expected;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()