-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

GCL-POLY (3800.HK)-Industry Restructure leads Results Decline!

Monday, October 8, 2012  10752

10752

GCL-POLY(3800)

| Recommendation | Reduce |

| Price on Recommendation Date | $1.240 |

| Target Price | $1.050 |

Weekly Special - 3306 JNBY Design Limited

Company Overview

GCL-poly is an upstream solar manufacturer. It's the largest polysilicon producer of China and the world's largest solar ingot and wafer manufacturer. Its business covers many branches of clean energy.

Summary

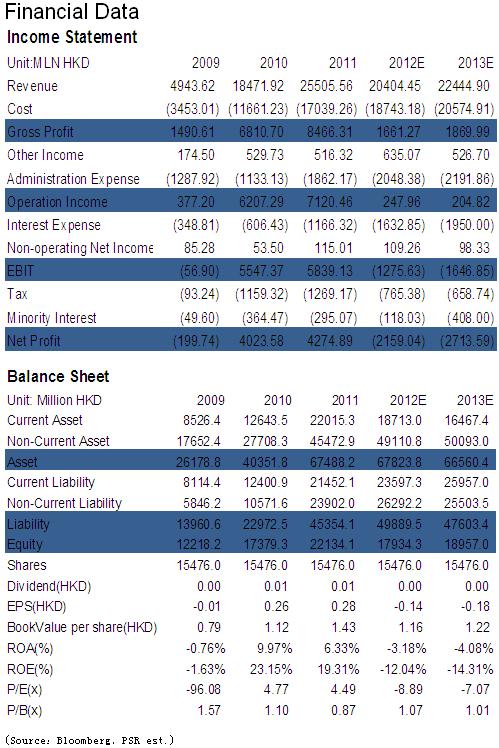

GCL-Poly's operation results suffered sharp decline in the 1HF of 2012. Because of demand decrease in developed market and EU anti-dumping policy, the operating environment of GCL-Poly has been deteriorating since 2011 and put great negative effects on operation results.

According to the semi-annual report of 2012, the capacity of GCL-Poly is still in expansion, but since the product price decrease greatly and the increase of cost is obvious, the operation results are still in down trend.

Although GCL-Poly has state several methods to cope with the negative change of the market, but in fact, the adverse change in the PV industry and market can`t be solve by technology update or expand new market.

The financial stability maybe worse in the future, as MIIT put differential credit policy for PV companies which not include GCL-Poly, the issue will affect the liquidity and finance cost of GCL in the future.

The EPS of 2011 is HKD 0.28, BVPS is HKD 1.43. According to recent information, the results decline is worse than our previous estimation and the decline will last in the 2H of 2012. We estimate that the EPS will decline to HKD -0.14 and the BVPS will decline to HKD 1.16. Considering the bad market environment, the target price in next 6 months is HKD 1.05 under 0.9x P/B, the rating is Reduce.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()