-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Sasa (178.HK) - Sales growth slowing down in July and August, looking forward to the coming Golden week and Express Railway Link

Tuesday, September 18, 2018  7941

7941

Sasa(178)

| Recommendation | Buy |

| Price on Recommendation Date | $3.890 |

| Target Price | $4.740 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Sales growth in the first quarter of FY 2019 (Q1, 1st March to 31st June ) accelerated to 24.8%, with sales revenue and same-store growth in Hong Kong and Macau growing by 27.7% and 25.3% respectively. The number of transactions from mainland tourists increased 27.5%, which led to 14.5% growth in the overall transaction volume. The average sales per transaction of local consumers and mainland tourists increased 8.1% and 7.0% respectively.

According to the management team, the slowdown began to be seen in the last week of June. In July, affected by the Sino-US trade war and fluctuations in the RMB exchange rate, the overall sales revenue growth in HK and Macao slowed down to 12 to 13%. In August, the figure was slightly improved to the mid-to-high double digits. Looking into the period from July to August, the consumer sentiment of HK local customers were negatively affected by fluctuations in the financial market more than mainland customers. The total number of transactions recorded low single-digit to negative growth, and the average sales per transaction was only increased by about 4%. For mainland customers, although the average sales per transaction was only with low single digit growth, the number of transactions increased by nearly 20%.

The management is optimistic about the business situation in the coming months. On 23th September, the opening of HK Section of the Express Railway Link will bring more mainland tourists to the retail market in HK. In addition, this year's mid-autumn festival is close to the National Day. It currently has no plan of increasing the discount rate or promotion efforts during the Golden Week to promote sales.In our view, the improvement in August is with low base effect caused by the worse weather in August last year. Its July trend goes with the overall HK retail sales growth, medicines and cosmetics grew 12.7% y.o.y. which showed slow-down trend comparing to 1H, but was already outperformed comparing to other category, and was the 1st runner up after jewelley, watches and clocks, and valuable gifts.

Sino-US trade war has caused volatility on RMB exchange rate and the financial market, coupled with the higher base in 2H of last financial year, it is expected that the slowdown trend in Sasa's revenue growth will continue in the coming months, but with the opening of the Express Railway Link and HK-Zhuhai-Macao Bridge, more tourists are expected to visit HK, which helps to offset some of the negative effects. We expect Sasa can record double-digit growth throughout the financial year. We are also optimistic about benefits that HK can gain through the policy and infrastructure development of Greater Bay Area in medium and long term, which help to drive the flow of people and economic prosperity within the region, while the retail industry will be among the first to benefit.

Despite the growth in top line for Q1, gross profit margin (GMP) has still been under downward pressure due to the proportion of low-margin trendy products in the product mix has increased. From July to August, the gross profit margin was close to 40%, the situation was similar to that of the first quarter. Thanks to the double-digit growth in sales revenue in HK and Macao, the trend of operating leverage continued in the second quarter. The management team plans to launch more trendy products. Sales growth of these products is higher than the traditional high-end products. These products` price ranges from tens to HK$200. Its target is to maintain the GPM at around 40%.

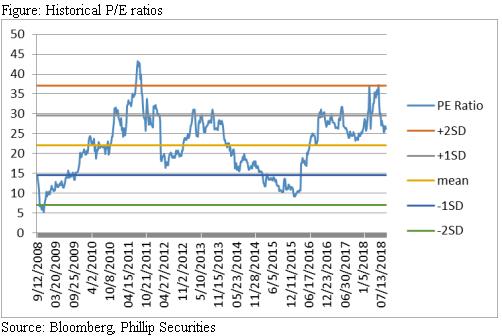

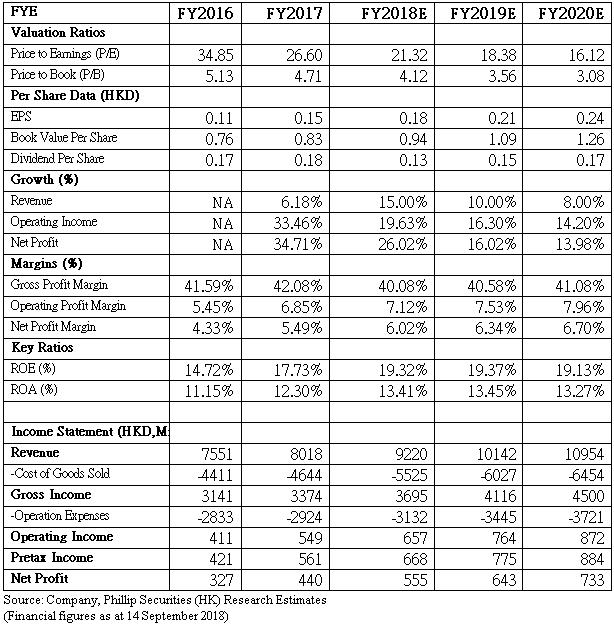

We expected that the whole-year GPM will still be under pressure. However, sales growth is expected to bring operating leverage with the rental and wage costs remain stable. We give Salsa Buy Rating, forecast price-earnings ratio 26 times, the corresponding target price HK$4.74. (Closing price at 14 September 2018)

Business Overview

Established in 1978, Sa Sa has grown from a 40 sq. ft. retail space to become today's regional "beauty" enterprise and is now the leading cosmetics retail chain in Asia, according to the "Retail Asia-Pacific Top 500" ranking of Retail Asia magazine and Euromonitor in 2017. As one of the largest sole agents in cosmetics in Hong Kong, Sa Sa represents over 200 international beauty brands in Asia.

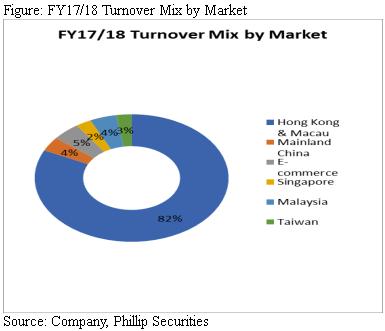

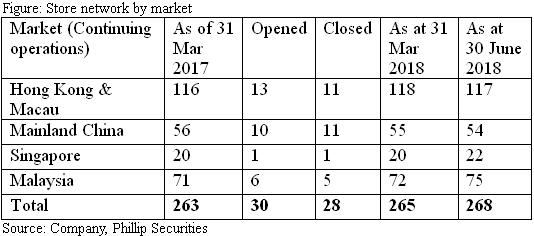

Listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange) in 1997 (Stock Code: 178). It has over 260 retail stores and counters in Asia selling over 700 brands of skincare, fragrance, make-up and hair care, body care products, health and beauty supplements including own-brands and exclusive products. The Group employs close to 4,800 staff in markets across the region, covering Hong Kong & Macau, Mainland China, Singapore and Malaysia.

Performance review

Since the second half of last year, Sasa's top-line growth has accelerated, which drove the whole year's revenue to grow 6.2% to HK$8.017 billion. Turnover (retail and wholesale) in HK and Macau recorded a growth rate of 7.9%, while same store growth(SSG) was 3.9%.

The growth rate in the fourth quarter was the fastest in the year, with a 14.4% increase in turnover, and turnover and SSG in HK and Macau increased by 17.8% and 15.1% respectively. The HK and Macau market accounted for 82.1% of total revenue last year.

Several factors contributed to the strong performance in HK and Macau, including the increasing demand from both local and mainland tourists. In mainland, the demand for middle and high-end cosmetic products is soaring on the back of strong retail growth driven by the improved purchasing power of Mainland residents living in the third and fourth-tier cities.

During the year, the growth rate of the total number of transactions was 3.8%, while the number of transactions by local consumers and mainland tourists by 3.3% and 4.6% respectively. The number of transactions decreased 1.1% in 1H y.o.y. but increased 8.5% in 2H, that means the sales increase in 2H was mainly resulted from the increased total number of transactions. The growth of average sales per transaction was 4.1%, 3.4% and 4.2% respectively for 1H and 2H.

GPM increased slightly by 0.49 ppt y.o.y. to 42.08%. However, GPM was under pressure in 2H. Thanked to operation leverage, operation costs were under controlled. The operation margin increased 1.4 ppt to 6.85%. In 2H, the margin increased by 2.24 ppt y.o.y. to 9.54%, reflecting accelerated sales growth, the company's effort of the closure of low-productivity stores, and rental reductions. Rental-to-sales ratio dropped at a quicker pace from -0.1% in 1H to -1.6% in 2H, resulting in an overall -1.0% for the full year.

Integration of online and offline platforms

Turnover of e-commerce business dropped 19.3% to HK$383.3milion in last year. The management team explained that this was due to the strategical raise of the minimum spending for free shipping from 1 April 2017 onwards. But the loss was reduced from HK$67.1 million to HK$28.3 million, reflecting the efforts on improving warehouse and logistic operations.

Revenue in Q1 increased by 20% y.o.y.. The management team does believe that online and offline businesses will compete with each other and tend to promote the integration of the two. It is expected that logistics costs will continue to decline.

We expect the e-commerce business performance to further improve this year. With the combination of online and offline networks, the operating efficiency is expected to continue to improve.

The company has announced collaboration with Taobao Global to create new retail model with integration of online and offline platforms. Buyers from Taobao Global promote products of Hong Kong retail stores on online platform, while mainland customers will be able to purchase products through the buyers on the platform.

In late 2017, It launched a brand new mobile app. Through optimising its stability and functions, online ordering was enhanced. These improvements also benefitted internal functions such as operations, and sales and marketing, while enhancing the overall customer shopping experience.

It also cooperated with third-party e-commerce platforms. In the Q2, it opened an online flagship store on Tmall Global to gain more exposure. It also partnered with Jingdong Group to launch a large-scale online shopping festival “JingShaJie” in Q4.

For the future development of e-commerce, Sasa plans to launch a new e-commerce system to provide a strong and flexible foundation to support current and future development. It also plan to further optimize the operation of warehouse in mainland to reduce logistics costs.

Focus on existing markets, change market strategies in China

Sasa has completed its exit from Taiwan market last financial year. The one-off loss of $16.9 million was recorded during the year. This market accounted for about 2.6% of the total revenue last year, so it has limited impact on revenue growth this year. According to the management team, after the exit of Taiwan market, it will focus on the existing markets and does not have plans to open new markets.

Last year, SSG in mainland market was 5.1% y.o.y. Thanks to better cost control and increased store contributions, the loss for this market reduced to HK$10.2million. Sales growth improved significantly in 2H, from 3.9% in 1H to 6% in 2H. This is because of the stablisation of the management team, which enhanced operational effectiveness, the closure of non-performing stores in isolated locations, while opening new stores in key cities. It also improved the product portfolio in mainland and enhanced the marketing strategy.

Last financial, the average logistic time was shortened from 10 days to 7 days, and the target for this year is to further shorten to 5 days. According to the management team, the timing of break-even will depend on the expansion of the scale of business. If the total number of stores reaches 100, which is twice the size of the existing ones, the business can be break-even.

Compared to HK market, the biggest challenge of mainland China market is still the strict inspection of imported cosmetic products, making it difficult to replicate HK's diverse-product business model. However, the management team has accumulated experience of store operation. Its next target is to improve the product mix through seeking cooperation with local suppliers instead of launch products of Sasa's own brands like before which is expected to give consumers more choices of different products.

The Greater Bay Area is one of the company's key development regions. It plans to open 4 new stores in cities within the region. Apart from that, it also plans to add new stores to existing regions. It plans to open 8 to 10 stores in total for this year.

Valuation and Risk

We expect the company's overall revenue this year to reach double-digit growth, and its gross profit margin will be under pressure as Q1. However, sales growth is expected to bring operating leverage with the rental and wage costs remain stable. We give Salsa Buy Rating, forecast price-earnings ratio 26 times, the corresponding target price HK$4.74. Potential risks include huge market or currency rate fluctuations that heavily hit consumer sentiments of Chinese tourists and visitors, huge drop of the number Chinese tourists and visitors, and local consumption not as strong as expected. (Closing price at 14 September 2018)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()