-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China New Higher Education Group Limited (2001.HK) - The Front runner in private higher education sector

Monday, May 28, 2018  10928

10928

China New Higher Education Group Limited(2001)

| Recommendation | Accumulate |

| Price on Recommendation Date | $7.300 |

| Target Price | $8.190 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

China New Higher Education Group (CNHEG) is one of the leading private higher education operators in China. We expect it will be the front runner in the future, because four schools out of seven of them are located in the provinces that have 1) a moderate increase in the number of candidates for Gaokao, and 2) below average gross higher education enrollment rate. They will surely enjoy universal higher education in China, and escape from the headache of low birth rate. We predict the earnings growth to be 37/14.3% in 2018/19F, assuming PE 28x (Average forward PE 20x with 40% premium). With 12.2% upside, we initiate “Accumulate” recommendation. (Closing price at 23 May 2018)

Business Overview

CNHEG is currently six operating schools in Yunnan, Guizhou, Xinjiang, Heilongjiang, Hubei, Henan, and one under construction in Gansu. It has positioned as an employment-oriented school and focused on applied sciences in order to make their students more equipped to the job market, then enhancing their reputation to attract talented high school graduates and eventually replicating a scalable business model across regions. This strategy has made Yunnan and Guizhou schools a remarkable employment rate, 98.1%, in 2017.

School

Headquartered in Beijing, CHENG has seven schools in Yunnan, Guizhou, Xinjiang, Heilongjiang, Hubei, Henan and Gansu, where the one in Gansu is under construction, and expect to commence in 2019.

1. Yunnan Technology and Business University (Yunnan School)

It located in Kunming, Yunnan, self-established in 2005 and provided 24 undergraduate education majors and 28 junior college education majors, such as Science majors (Civil Engineering, Computer Science, Architectural Design, and Vehicle Inspection and Maintenance), and business majors (Accounting, Auditing, Financial Management, and Logistics Management).

For 2017, the student enrollment is 23,642, presenting 12.8% CAGR over past four years. The moderate CAGR in enrollment showed a satisfactory organic growth in this Yunnan region. Besides, according to the statistics from Yunnan Education Department, the market share of private higher education in Yunnan was 10.5% as of 2016.

2. Guizhou Technology and Business Institute (Guizhou School)

It located in Guiyang, Guizhou, commenced in 2012 and offered 30 majors through six colleges (Accounting, Architecture, Business administration, Design & Engineering, Nursing and Physical Education). It provides practical trainings for selected final year students, general education (teaching skills such as English and Computing), and continuing education to help students prepare their undergraduate exams or other requirements for bachelor's degree.

15,584 students have enrolled in the institute for 2017, implying a 40.7% CAGR over past four years. Despite a high CAGR, the growth in student enrollment has been slowed down in recent years, as the school has already entered a mature stage. In 2016, it had 3.3% market share in the private higher education in Guizhou.

3. Harbin Huade University (Northeast School)

Located in Harbin, Heilongjiang and owned 73.91% by CNHEG, it has eight colleges for example, Electronics and Information Engineering, Mechanical Electronic and Automobile Engineering, Architecture and Civil Engineering, Arts and Media, Economics, Language, Clothing, and Robotics Engineering, offering thirty-six majors in total.

The student enrollment for 2017 is 9,355, slightly dropped 1.7%. Management explained they are going to upgrade to undergraduate level this year, so they are now focusing on the quality of the students. In addition, the market share of the school in Heilongjiang's private higher education was 8.4% as of 2017.

4. Science and Technology College of Hubei Minzu University (Central China School)

Fully owned by CNHEG, the school is in Enshi, Hubei, offering more than forty undergraduate, junior college, and pre-undergraduates programs, including Medicine, Music, Physical Education, Mechanical Electronics and Information Engineering, Architecture, Economics, and Culture & Media. The student enrollment in 2017 is 5,709, lifting 64% YoY, along with 1.3% market share in private higher education for Hubei province.

5. Xinjiang Institute of Finance and Economics (Xinjiang School)

Owned 56% by CNHEG, the school is located in Korla, Xiajiang, and mainly provides undergraduate business courses, such as Accounting, Financial Management, Marketing, Human Resource, Tourism, Law, and etc. Currently, the student enrollment is 3,746 in 2017, and the latest data for the total enrollment of private higher education in Xiajiang is 34,500. Hence, we estimate the market share of the Xiajiang is around 8-9%.

6. Luoyang Science and Technology Vocational College (Henan School)

CNHEG invested in the Henan School (located in Luoyang) on Jan 2018, owning 55%. It provides secondary school curriculum and junior college courses, such as Electronic Commerce, Information Engineering, Intelligent Manufacturing, Art, Tourism, International Finance and etc. The current number of enrollment is 18,243, accounting for 4% market share in the private higher education of Henan.

7. Northwest Technology and Business Institute ( Northwest School)

On July 2017, CNHEG commenced the construction in Lanzhou, and expect to complete on September 2019.

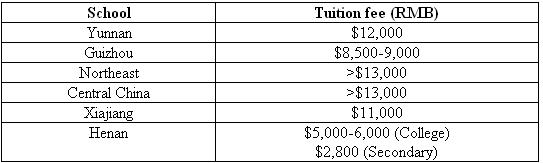

Tuition Fee

In 2017/18, the average tuition fee for Yunnan, Guizhou, Central China and Northeast school is RMB $11,548, still lower than that of other private higher education institutions (RMB $13,068).

Industry Overview

The private higher education industry in China has boomed in the past decade, as the higher education gross enrollment rate has been rising, thanks to the economic development. Yet, there is a reduction in the higher education age population for some provinces due to low birth rate, mitigating the growth brought from increasing gross enrollment rate.

Higher education is becoming more popular in China

The higher education gross enrollment rate has kept soaring, from 23.3% in 2008 to 42.7% in 2016. Because the economic development will goes on in China across different provinces and the enrollment rate is lagging behind compared to the western countries, we believe the gross enrollment rate will maintain its momentum in the future,

Flourishing economy in China

Since the economic reform, China has become the second largest economy in the world. The GDP per Capita has reached USD 6,894, at 7.7% CAGR. As the citizens have become wealthier, we expect it will enhance the gross enrollment rate in higher education

Lagging behind western countries

Compared to those developed western countries, the gross enrollment rate of higher education in China is significantly low, only 37.5% in 2014, with United States (86.7%), United Kingdom (56.5%), Germany (65.5%) and the average (71.8%). As the education development in China goes on, we expect the gross enrollment rate in China will increase steadily, shrinking the gap between China and those western countries.

Admission rate increasing, whereas decreasing number in candidates for Gaokao

The admission rate was rising from 57% in 2008 to 82% in 2016, because the higher education has become more and more popular, whereas the number of candidates for Gaokao peaked in 2008, and stabilized at ~900 million in recent years, mitigating the rising admission rate. It implies the admitted candidates actually grew slowly at 3.2% CAGR from 2008 to 2016. However, some provinces still have an increasing number in candidates for Gaokao, for example Yunnan, Guizhou, Jiangxi, Xinjiang, Henan and etc. Hence, we believe the winner in higher education will be the one locating their schools in those provinces.

Why CNHEG?

In light of the current situation of private higher education in China, we believe those schools located in provinces that have 1) a moderate increase in the number of candidates for Gaokao and 2) below average gross enrollment rate will have greater potential to be successful in the future.

First, Ministry of Education has claimed the admission rate for Gaokao will not decrease in order to enhance the gross enrollment rate, meaning the increase in candidates for Gaokao will eventually lead to a rise in students admitted. Second, the source of the students for the private higher education institutes usually comes from their own provinces, for example, 90% of the students for Yunnan and Guizhou schools are local, meaning that private schools will definitely enjoy, if the number of students admitted for their own province is getting larger.

Among all the company in the higher education sector, CNHEG is the current company that matches our criteria the most.

Four out of seven schools for CNHEG matched our above criteria, which are Yunnan, Guizhou, Henan and Xinjiang.

1) A moderate increase in the number of candidates for Gaokao

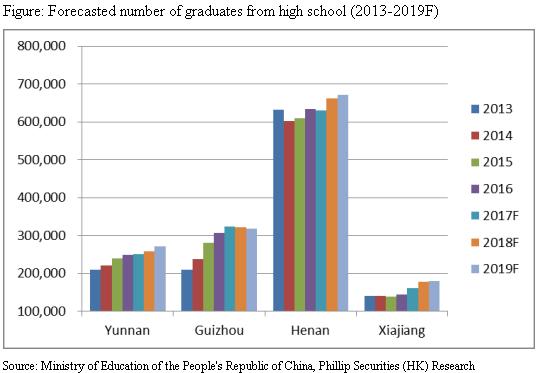

In order to estimate the number of candidates for Gaokao in the next few years, it is important to look into the number of graduates from high schools, the main source for Gaokao.

We forecast the number of graduates from high school for 2017-2019 by referring to the number of the high school senior one, two, and three students in 2016 added adjustments. As we believe the high school students are very likely to continue their study once they have entered schools. Thus, the number of the senior one, second and three students will be a reliable estimator for the number of graduates in the future.

The results have shown that Yunnan, Guizhou, Henan and Xiajiang will have no decline in the number of graduates. There is even positive growth in Yunnan, Henan and Xiajiang. However, the growth in Guizhou started to slow down, with 1% drop in 2019.

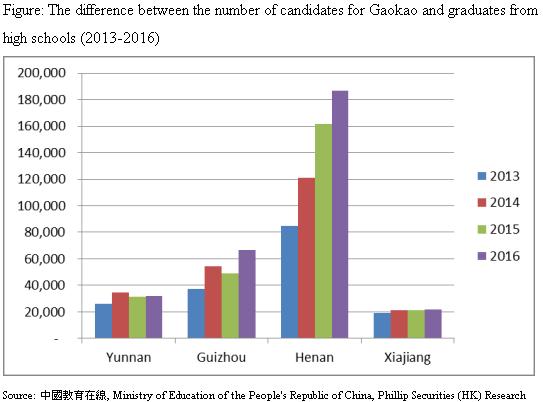

Besides, there is always a difference between the number of candidates for Gaokao and graduates from high schools, because some Gaokao candidates may be self-study, so it will not be counted in the graduate from high schools. Hence, it is also critical for us to investigate the difference.

In general, the difference for Guizhou, Henan and Xiajiang presents an uptrend, except Yunnan, suggesting that there are more and more Gaokao candidates who are from sources other than high school graduation.

As the number of graduates from high school stabilized or even increased, with a rising supply from the sources other than high school graduation. We believe it is safe to assume there will be a moderate increase in the number of candidates for Gaokao in those four provinces.

1) Below average gross enrollment rate

The 13th five-year plan has stated a target for higher education gross enrollment rate to reach 50% in 2020, which was 42.7% in 2016. Guizhou (32%), Yunnan (32.6%), Xiajiang (35.3%), and Henan (38.8%), where CNHEG has established schools over there, has lower gross enrollment rate than average, implying that there is still rooms for growth of the students admitted in those provinces. Besides, it is cautious that the gross enrollment may be inflated because the higher education age population is reducing acorss different provinces. However, we expect there will be still an increase in students admitted due to a robust growth in gross enrollment ratio for those provinces.

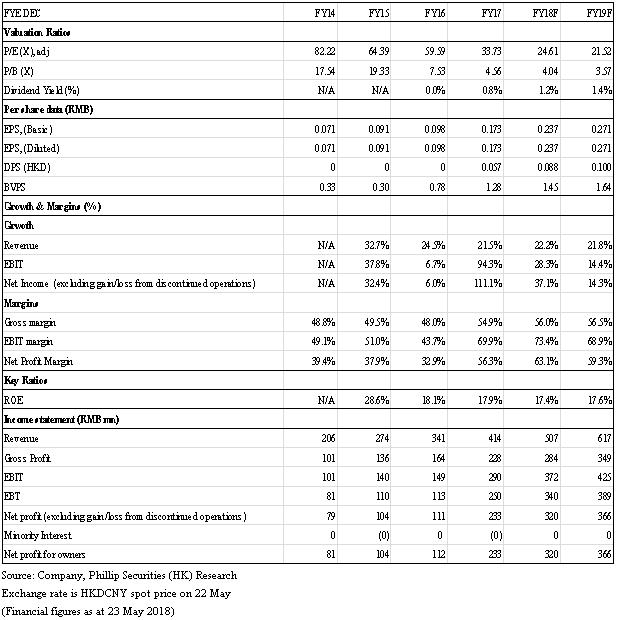

Earnings forecast

Revenue

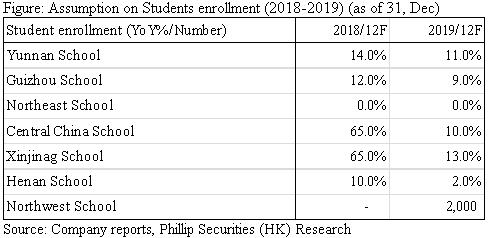

We expect revenue will grow 22.2%/21.8% YoY in 2018/19, as we see there is a moderate growth in student enrollment and the tuition and boarding fee in Yunnan and Guizhou and the completion of Northwest schools in 2019. The growth assumption has only accounted for Yunnan, Guizhou and Northwest schools because we have not yet consolidated the financial reports with Northeast, Central China, Xinjiang and Henan. The management is confident that those four schools will start to consolidate within this year.

Students enrollment

We expect the Yunnan and Guizhou schools will maintain its momentum in the next few years, where Yunnan will outperform a little bit as suggested by our estimate in high school graduates. Besides, the Northeast school will stay flat in 2018/19F, because the schools is upgrading to undergraduate level. The group will now focus on the quality of students. As there will be no student outflow in 2018, we should see Central China and Xinjiang delivering a 65% increase.

Moreover, based on our estimation on the number of candidates taking Gaokao, Xinjinag School will show a better performance than Central China in 2019F. In addition, we forecast there will be 10%/2% growth for Henan school in 2018/19F, because the capacity of the schools is around 20,000 students, and the management expect it to be full in 2019. Hence, we give a lower growth rate in 2019, assuming the enrollment merely reach around its full capacity. Also, we expect Northwest school will be completed in 2019 with around 2,000 students for the first year.

In aggregate, we expect the students enrollments rose 17.2% YoY% to 89,429 in 2018, and 9.7% to 98,111 in 2019.

Tuition and boarding fee

We expect there will be a 7% drop in average fee per students in 2018F due to the inclusion for a much lower fee from Henan school, and a 0.7% rise in 2019F.

Gross profit margin

CNHEG has a sudden rise in GPM in 2017 thanks to the increase in revenue was higher than the increase in costs. We expect the GPM will be 56%/56.5% in 2018/19F, because the improvement in operating efficiency from centralizing the resources for their schools.

Net profit Margin

Since the profit from Northeast and Central China schools have shown as a service fee in 2017, the NPM has been inflated to 56.3%. We forecast the NPM will be 63.1%/59.3% in 2018/19F (assuming the consolidation have not yet done, and the profit from schools other Yunnan, Guizhou and Northwest will be shown as a service fee).

Valuation

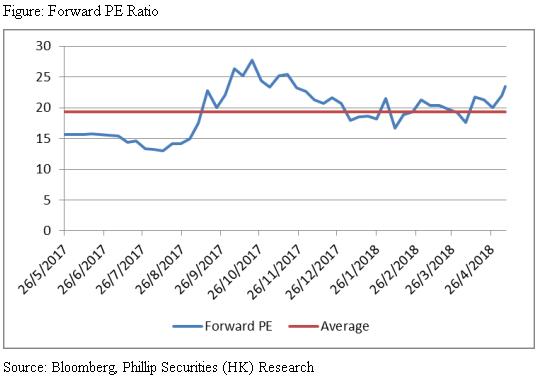

We give a target price of HK $8.19, assuming PE 28x (Average forward PE 20x with 40% premium) due to the competitive advantage in CNHEG. With 12.2% upside, we initiate “Accumulate” recommendation. (CNY/HKD = 1.233) (Closing price at 23 May 2018)

Risk

1. VIE structure prohibited in China

2. The faster than expected decrease in birth rate

3. New acquired schools were not able to add value

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()