-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China New Higher Education Group (2001.HK) - Greater value form Gansu College but policy risks are emerging

Wednesday, August 15, 2018  9834

9834

China New Higher Education Group(2001)

| Recommendation | Accumulate |

| Price on Recommendation Date | $4.700 |

| Target Price | $5.050 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

CNHEG announced to acquire Gansu College, and gave up its original plan on Northwest school. And, the land for developing Northwest school will serve as the new campus of Gansu College. We believe the acquisition can reduce the time required for cultivating the school and it can leverage on the brand name and teaching resources of Lanzhou University of Technology. However, the Revised Draft of Law for Promotion of Private Education from Ministry of Justice of the PRC proposed a prohibition on the acquisition of non-profit private schools. Based on the DCF model, we give a target price of HKD5.05, and maintain our “Accumulate” rating, with 7.45% potential upside. (Closing price as at 13 August)

Company Update

1. On 9 July, CNHEG announced to enter into the cooperation agreement with Lanzhou University of Technology, becoming a joint school sponsor of the Gansu College. The company will contribute RMB200 million (including the paid land use right valued at RMB 165,670,000) for the new campus, and be responsible for the construction of the new campus and operation of the Gansu College thereafter.

2. On 10 Aug, Ministry of Justice of the PRC announced “中華人民共和國民辦教育促進法實施條例(修訂草案)(送審稿)”. The enterprise of education institute may not control non-profit private schools through mergers and acquisitions, franchise chain, agreement control, etc. And, the government intends to strengthen the supervision of the VIE structure.

Acquisition of Gansu College

CNHEG gave up its original plan of self-establishing a school in Gansu, and made use of the land for the construction of the new campus for the Gansu College instead. We believe two advantages can be brought from its aforementioned decision, 1) less time required for cultivating the school and 2) leveraging on the brand name and teaching resources of Lanzhou University of Technology.

Less time required for cultivating the school

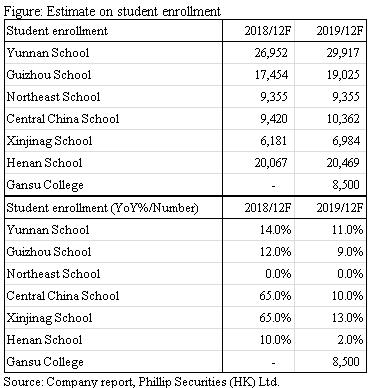

In order to provide undergraduate education, it takes at least twelve years for self-established schools, and requires several approvals from government. Moreover, the self-established schools have to build up their student base from scratch. Therefore, it takes a long period of time to cultivate a mature school. Now, it can reduce the time for cultivating a school by acquiring Gansu College directly. First, Gansu College is now providing undergraduate education, so it does not need to spend plenty of time on undergraduate program. Besides, it had existing students, with 8,372 and 8,218 in the school year of 2016/17 and 2017/18. Thus, it can generate profit much earlier than a self-established school. The management expected the net profit in 2020 can reach RMB 13 million.

Leveraging on the brand name and teaching resources of Lanzhou University of Technology

Gansu College was one of the independent institutes under Lanzhou University of Technology. According to cooperation agreement, Lanzhou University of Technology will contribute intangible assets comprising its school name and teaching resources, enabling CNHEG to leverage the brand name and teaching resources of Lanzhou University of Technology. Currently, Gansu College owned around 300 teachers, and some are part-time teachers from Lanzhou University of Technology. Apart from undergraduate education, CNHEG only targeted to provide junior college program in order to expand its scale.

Future development

Students

Since the school condition of Gansu College was relatively poor, where its area of campus and classrooms are relatively small, the college stopped expanding its student base. Therefore, the student enrollments in 2018 are lower than in 2017. As the new campus is built, the school condition will be improving, and the student enrollment will increase.

Tuition fees

The tuition fees are currently RMB 11,000, a relatively low level. As the school condition is improving, the management expected there will be a 5-10% rise in the future.

Management fees

Based on the business model of independent institute, Gansu College needs to pay management fees to its parent university (Lanzhou University of Technology). The management fees have been confirmed with the parent university, where the amount will be lower than the average in the market.

Profitability

The net profit margin for Gansu College is around 15-20%. Currently, the college needs to pay a management fees to its parent university, and the operating cost is also relatively high. It is believed the operating efficiency and profitability can be enhanced after the acquisition by CNHEG.

Revised Draft of Law for Promotion of Private Education

In the Revised Draft of Law for Promotion of Private Education from Ministry of Justice of the PRC, the article 5, 12 and 45 have the greater impacts on the industry.

Article 5: Foreign enterprises established in China and social organizations with foreign parties as actual controllers shall not hold, participate in or actually control private schools that implement compulsory education.

Article 12: The enterprise of education institute may not control non-profit private schools through mergers and acquisitions, franchise chain, agreement control, etc.

Article 45: Private schools shall disclose related party transactions. The Ministry of Education and Human resources and Social security shall strengthen the supervision of the signing of agreements between non-profit private schools and stakeholders, and the necessity, legitimacy and compliance of agreements involving major interests or long-term and repeated execution shall be conduct an audit review.

Once the aforementioned articles come into effect, CNHEG will need to recognize its schools from non-profit to for-profit, meaning the drop in profitability since they are no longer eligible for the tax exemption. Besides, the M&A targets will remain to those non-profit, and the required time for M&A may also be lengthy due to the stronger supervision from government. However, we believe the impact on higher education sector is relatively small, because the law only forces higher education operators to recognize their school as for-profit, rather than prohibited like compulsory education. Therefore, there are still rooms for higher education sector. But, as the effective tax rate rise and the supervision on M&A, the valuation is believed to be hampered.

The impact on assumptions

Acquisition of Gansu College

We lift our estimate on the student enrollment in the school year of 2019/20 from 2,000 to 8,500, together with an increase in tuition fees from RMB 8,000 to 11,000.

Revised Draft of Law for Promotion of Private Education

We assume CNHEG recognize all its school to be for-profit, making the effective tax rate increasing from 6% to 15%. As the article 53 in the Law for Promotion of Private Education stated there will be tax benefits from the for-profit schools, we assume the effective tax rate will be lower than the income tax rate (25%) in China, even though it recognizes its school to be for-profit.

Valuation

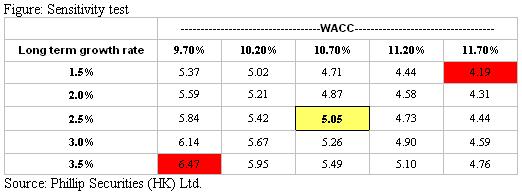

We adopted a three-stage discounted cash flow model, assuming the short and long term growth rate are 10% and 2.5% respectively, with 10 declining years and 10.70% WACC. According to the range for WACC [9.70%,11.70%] and long term growth rate [1.5%,3.5%], the highest and lowest target price are HKD6.47 and 4.19 respectively.

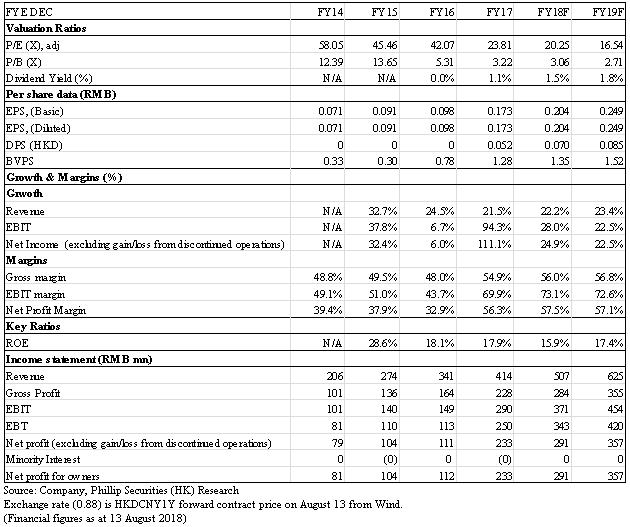

Compared to the self-established school, it takes less time to develop the Gansu College, thereby bringing greater value to CNHEG. However, as the policy risk and the depreciation in RMB, offsetting part of the new value from the Gansu College, we give a target price of HKD5.05, representing a PE ratio of 21.8x and 17.8x in 2018/19. We remain “Accumulate” recommendation, with 7.45% potential upside. We have factored in the worst scenario. Once the policy risk mitigates, we believed it is quite attractive for the current valuation. (CNY/HKD = 1.14)(Closing price as at 13 August)

Risk

1. VIE structure prohibited in China

2. The faster than expected decrease in birth rate

3. New acquired schools were not able to add value

4. The Revised Draft of Law for Promotion of Private Education passed successfully

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()