-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

HC Group (2280.HK) - Transition into vertical B2B, a new growth driver

Wednesday, November 14, 2018  10480

10480

HC Group(2280)

| Recommendation | Buy |

| Price on Recommendation Date | $4.880 |

| Target Price | $6.580 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

HC Group is an information and B2B e-commerce service company in China. Its main businesses include: transaction, data and information services. Assuming 2018E P/E ratio to be 22x (the average of the past five years is 24x, we think 22x is within the reasonable range), we derive the target price to be HK$6.58, and initiate a “Buy” rating with 34.8% potential upside. (Closing price at 6 Nov 2018)

Catering to the B2B platform revolution with a variety of ancillary services

As it was proved in the past that the platform solely relying on information services to match up buyers and sellers has not been so successful, it is necessary to inject the logistics and capital flows in order to further penetrate business transactions, leading to greater customer stickiness. The Group caters to the trend and focuses on three major vertical B2B platforms, including: Ibuychem, Union Cotton and China Formwork. These platforms provide Logistics, Payment, Warehousing, Finance and Data services to deeply penetrate the entire business transaction process, and resolve the current difficulties in the B2B field, enhancing the platform value.

The ascendancy in transaction segment will spread to information and data segment

he Group's current profit mainly comes from information services, but it will focus on transaction services segment in the future, in order to spread the ascendancy to the information and data services segment by bringing traffic and data through transactions. As the transaction volume gradually hiked, the B2B platform of the Group can capture enormous user and market data to develop advertising and data analysis services on the platform.

Interim revenue and profit increased significantly, while gross profit margin fell sharply

The interim revenue reached RMB 3.79 billion, up 182.3% YoY; the profit attributable to equity holders of the company was RMB 190 million, up 77.6% YoY. However, due to the low gross profit margin of the transaction segment, the GPM of the Group dropped significantly from 49.2% to 17.7%. On this May, the group announced to hold an aggregate of 51% of equity interests and will officially be consolidated. In the second half of the year, China Formwork will also be consolidated in the consolidated financial statements.

Business Overview

Founded in 1992, HC Group is an information and B2B e-commerce service company in China. In 1994, the Group signed an exclusive agreement with Fuguo Company to represent the "Personal Computer" and "Electronics and Computers" advertising, entering the trade catalogues and yellow page directories business. In December 2013, the group was listed on the Growth Enterprise Market of the Hong Kong Stock Exchange. With the rise of the Internet, the Group officially renamed to “HC360” in March 2004 and opened more than 40 industry channels and 76 industry search engines. In September of the same year, HC360 cooperated with Tencent Technology to launch the instant messaging software “Mai Mai Tong TM”, preparing for the transition to an online information platform for the Group. In 2014, the Group successfully listed in the Main Board of the Hong Kong Stock Exchange. In March 2015, the Group acquired ZOL Online for RMB 1.5 billion, becoming the Group's second major online information platform. However, in 2015, the Internet business started reaching the top and both revenue and profits declined. In 2017, Liu Jun became the CEO of the Group and proposed two principles of “專注” and “聚焦”, focusing on three business segments of information services, transaction services and data services, and positioning the company as the leader in industry Internet in China which empowers traditional industries by the internet and data. In August 2018, the group also appointed Zhang Yonghong, former executive vice president of the Tsinghua Unigroup, as co-president.

Industry Analysis

Why is the B2B platform not as successful as B2C in the past?

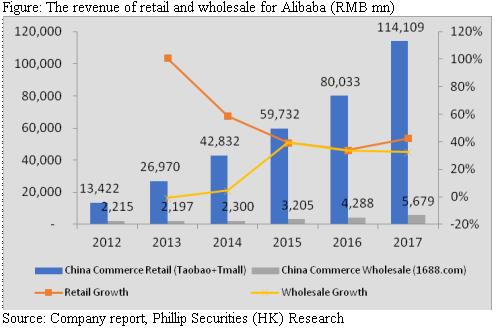

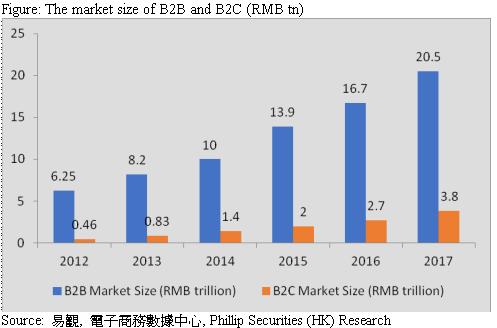

There are two leading players, Tmall and JD.com tin the B2C industry in China, while there are also leaders such as Alibaba 1688 in the B2B industry. But why are the leaders in this industry not as successful as in B2C? Take Alibaba as an example. In 2017, the revenue of B2C platform “Tmall” was estimated to be about RMB 40 billion (because Alibaba announced the revenue of Taobao and Tmall was combined, we assume that the revenue of Tmall accounts for about 35% of the total revenue based on the proportion of its past GMV); whereas the revenue of B2B platform “1688” only recorded about RMB 5.6 billion. The revenue of the B2C platform was almost seven times higher than that of B2B. However, in 2017, the market size of the B2B in China was five times greater than that of B2C. What factors cause the absence of B2B platform with a similar size of Tmall and JD.com, when B2B market size is much greater?

We believe that it is caused by the difference between B2B and B2C in terms of business model. For the profit model of E-commerce in the past, these two kinds of platforms generally bridge the gap between buyers and sellers via an online platform, where the platforms receive membership or advertisement fees. But, as for the business model itself, it is much more suitable to B2C than B2B industry. The characteristic of a B2B platform is first the buyers are more rational and concern about the quality of products and their integrity because the delay in product delivery could affect adversely their operation, which makes the online advertisement and sales promotion ineffective to facilitate transactions. Second, the relationship between businesses is more stable, so once the businesses reached its customers in the B2B platform, the transactions could be done without the platform next time, implying that they do not need the platform anymore. Third, the number of customers in B2B is less, but with more repetitive purchase. As a result, once the businesses have accumulated enough customers for repetitive purchase, the demand of the platform to the businesses for matching up function reduces. However, the buyers in B2C are more emotional, and their purchasing behaviors are mainly driven by desire and preference, which makes the online advertisement and sales promotion more effective. Besides, the relationship between business and the individual customer is less stable and with less repetitive purchase, so the businesses have to stay in the B2C platform in order to attract new customers. In other words, B2C platforms have stronger customer stickiness than B2B under the information era (simply matching up buyers and sellers by advertisement), explaining the fact that why B2C outperformed B2B in the past.

B2B 1.0 to B2B 2.0

It has shown in past that B2B platform was not so successful by simply providing information services to matching buyers and sellers, so what kinds of B2B platform could be successful?

We believe 1) a variety of ancillary services and 2) picking a suitable industry and product are essential for a B2B platform to succeed.

1. A variety of ancillary services

In order to enhance the customer stickiness of the platform, the platforms have to penetrate the logistics and capital flows of a transaction, upgrading from B2B 1.0 (Information) to 2.0 (Information + Logistic + Data). Because of the characteristic of B2B customers, the information services are not enough, and it creates values only when it resolves the difficulties faced by businesses. As for Finance, SMEs have less collateral and fixed financial assets and lack of qualified financial statement, leading to refusal of bank financing. Therefore, if the platform is able to help the business finance, it could enhance the customer stickiness. As for Data, the upstream enterprises are usually not accessible to the date of downstream, making them difficult for estimating production volume. Meanwhile, the price data are also valuable to enterprises in the commodity sector. So, if the platform is able to provide those data, it could enhance the value of the platform. Only by penetrating the transactions in terms of Logistics, Payment, Warehousing, Finance, Data and so on as well as resolving the difficulties faced in the B2B industry, the B2B platform can succeed.

2. Picking a suitable industry and product

Based on the characteristic of B2B buyers we have mentioned, it is quite difficult for the current B2B platform to satisfy the large-sized enterprises. Generally, before entering into a procurement agreement, large-sized enterprises require testing on the products, then a small batch of trial with countless communications and adjustments. Due to the complexity of the procurement process, large-sized enterprises seldom procure via the online B2B platform. As a result, we think it will be more likely for a B2B platform to be successful if they are facing the industry where major buyers are SMEs, because the purchasing process of SMEs is closer to that of an individual, where their procurement process is relatively simple, compared to large-sized enterprises, resulting in a higher willingness to purchase via online B2B platform. For example, the procurement decisions are made by several departments in a large-sized enterprise; while that may be made by the boss solely in SMEs.

In addition, it will be more likely to be successful if the product traded in the platform is a standardized commodity, which means the upstream suppliers will not have a strong bargaining power, so the companies in downstream could lower their cost by consortium purchasing through the online B2B platform. Asides the type of products, chances are the online B2B platform will succeed if there is a lengthy supply chain.

Business analysis

The group focuses on three segments, including transaction services, data services and information services and creates industrial internet by empowering traditional industries with “Internet” and “Data”.

Transaction Services

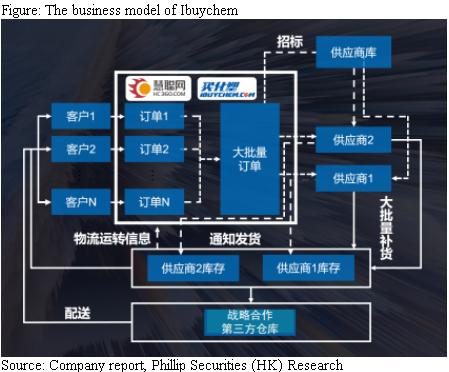

Ibuychem

Ibuychem was launched in March 2015, and targets chemicals and plastics, sub-commodities and fine chemicals. The platform matches the buyers and suppliers for spot transactions and provides the financing and logistics services to resolve after-sales issues. Since it is large-sized suppliers versus small-sized buyers in the chemical industry, the platform adopts consortium procurement as their operation model, where the platform first gathers the discrete orders from the downstream and consolidates them, then purchases from the upstream to lower the procurement cost. The take rate is about 0.5%-1.5%. Ibuychem was built by the Group itself, and the founder, Guo Xihong, have been working in the B2B chemical industry for many years. Now, it serves nearly 1 million enterprises, 8 million members, and 80,000 suppliers, with more than 1 million SKUs. In addition, Ibuychem has established branches in South China, East China and North China to provide matching services in local for Guangzhou, Shunde, Dongguan, Shenzhen, Shanghai, Ningbo, Hangzhou, Wuxi, Beijing and Tianjin. The similar platforms are “化塑匯”, “買塑網”, and etc.

Union Cotton

Union Cotton was established in August 2015 and launched in April 2016, positioning itself as the platform for cotton spot trading. It provides services such as online transactions, payment settlement, logistics, warehousing and online finance. As cotton is generally produced in the northwest, while most of the textile companies are located in the south. For those small textile companies with no purchasing team, they have to buy raw materials from merchandisers which that have been marked up and resold. It implies that the supply chain is lengthy and costly to the buyers. Besides, the landscape of cotton industry is small-sized suppliers versus small-sized buyers, so the platform adopts agency procurement as their operation model. Union Cotton helps the buyers match with suppliers directly, avoiding the multiple mark-up from merchandisers and lowering the purchasing cost. The buyers can lower their transportation cost by gathering deliveries from other companies. The group increased its equity interests to 51% in this April for a total consideration of RMB 50 million. In the full year of 2016, the transaction volume of Union Cotton has reached 25,800 tons, with a total GMV of RMB 378 million, and the growth rate of the average monthly transaction volume was as high as 34%. In 2017, the GMV of Union Cotton has exceeded RMB 1 billion and the number of active members in the upstream and downstream has reached 1,000, with a daily average of 100,000 tons. Besides, the founder and CEO of Cotton Union, Gong Wenlong, is very experienced in the cotton industry and is the founder of China Cotton Network and the National Cotton Monitoring System.

China Formwork

China Formwork is positioned to as a materials bank in the construction formwork industry, covering smart attached lifting scaffolding, aluminum alloy formwork system, glass fiber formwork system, building smart device, etc. Through the SaaS platform “雲租寶”, the users can rent or lease out materials, like aluminum formwork and elevator frame. Due to the expensive transportation cost of the construction formwork materials, if the location between the previous and next construction projects is too far away, the building subcontractors will tend to lease out the materials at the current project location, and then rent it at the next project site to reduce transportation costs. In addition, China Formwork also provides services such as design, installation, repair and refurbishment and supply chain finance. As the requirement on the safety of construction sites became strict, subcontractors need a high-quality proposal of the formwork and elevator frame design in order to compete projects from general contractor. As a result, China Formwork provides solutions, such as the production of building information models, to help subcontractors to fight for the projects. Apart from it, the equipment needs to be refurbished frequently. Thanks to the economies of scales, China Formwork can be repaired and refurbished with cheaper expenses. Part of its business is self-operated leases, that is, they purchase materials and then rent out for profits, but it only accounts for a small proportion. At present, the group holds 57% of the equity interests and will be consolidated in the second half of 2018. Moreover, there are no competitors in the market, so the profit is higher than other platforms of the group.

We believe that the B2B platforms of the group fit well with the elements we have mentioned in order to become a successful B2B platform. For Ibuychem, the chemical products are highly standardized. The market consists of large suppliers and small buyers, which facilitates consortium procurement. And, the platform provides ancillary services such as logistics, finance and data, which is in line with the trend of B2B 2.0. For Union Cotton, cotton products are relatively standardized, and buyers and sellers in the market tend to be small. Due to a lengthy supply chain, the effectiveness of the online B2B platform will be more obvious. Meanwhile, it also provides additional services such as payment and settlement, logistics, warehousing and online finance. For China Formwork, although the platform is mainly for sub-leasing, in addition to information matching services, it also provides a variety of value-added services, such as design, installation, maintenance refurbishment and supply chain finance, in line with the B2B 2.0 trend.

Data services

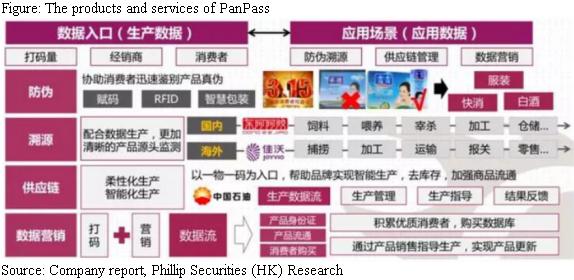

PanPass

Listed on National Equities Exchange and Quotations in China (430073), PanPass provides customers with anti-counterfeiting, traceability, supply chain management and data marketing services through the cloud platform, and using big data, Internet of Things, blockchain and other technologies, supplemented by digital code, QR code, RFID and other labels. PanPass has been working in the anti-counterfeiting industry for more than 20 years, owns 30 anti-counterfeiting know-hows and serves more than 40,000 customers, including: Samsung Electronics, Sony, LG Electronics and Xiaomi. Among them, PanPass has successfully applied blockchain technology into the project of Tong Ren Tang, Hong Ji Tang, Dezhou Chicken and Lulu Group. PanPass was certified by the General Administration of Quality Supervision and Inspection of the People's Republic of China. In the upgrade project of Chinese herbal medicines in Shandong Province, the traceability upgrade systems of customers Dongya Ejiao, Fupai Ejiao and Hongjitang Ejiao were rated as excellent. The financial performance of PanPass in 2018 was satisfactory, with revenue reaching RMB 79 million, a YoY increase of 63%; net profit attributable to the owner was RMB 8.7 million, up 54% YoY. The Group is positive to the development of PanPass and has increased its holdings to 79.51% this year.

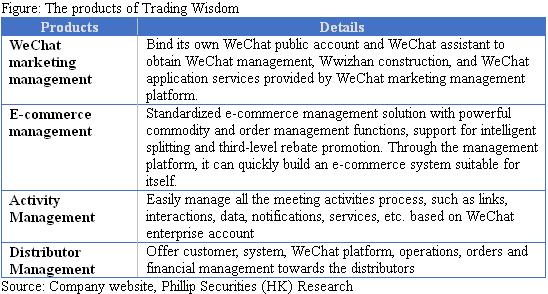

Trading Wisdom

Trading Wisdom is a domestic cross-border integrated marketing platform that provides customized and accurate integrated marketing services through online advertising and market data analysis. It provides WeChat marketing management, e-commerce management, activity management and distributor management. In the third quarter of 2017, it established a tripartite data research institute with China Unicom Big Data Center and Tsinghua University to develop data marketing.

Information services

ZOL.COM

ZOL.COM is the leading 2C technology portal in China, covering more than ten types of products, including: mobile phones, laptops, digital products and home appliances. The portal not only provides visitors with product specifications, product evaluations, product comparisons and product updates, but also offers price quotes of the electronic products for more than 40 cities nationwide. The portal has its own editing team for each product to create content for attracting online traffic. At present, the daily traffic from PC and mobile is about 150 million, with more than 40 million registered users. Moreover, the number of articles read is more than 1 million per day and the video views exceed 20,000. The portal currently has a market share of approximately 62% and is the leader of technology portal in China. The revenue of ZOL.COM mainly comes from advertising revenue. It diverts visitors to Tmall and JD.com or serves as an online portal for third- and fourth-tier city distributors, where products will be delivered by local distributors, in return for advertising revenue.

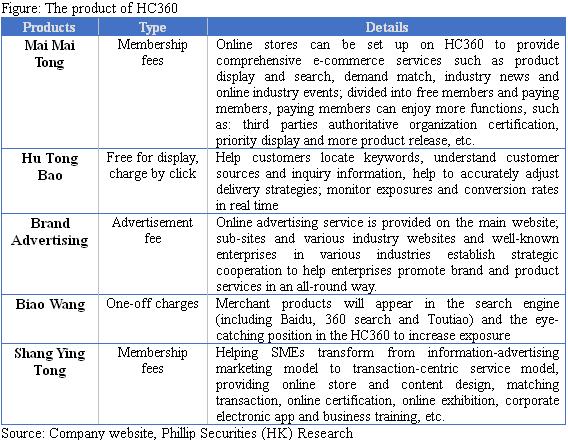

HC360

HC360 is the core online 2B information service platform of the Group, focusing on industrial products, similar to the business model of Alibaba 1688. The platform provides products and services including Mai Mai Tong, Hu Tong Bao, Brand Advertising, Shang Ying Tong and Biao Wang. The main source of revenue comes from membership fees and advertising fees. HC360 will strengthen the product content on website in the future, which will be similar to the business model of ZOL.COM in order to increase user stickiness. In view of this, the Group moved the staff of HC360 and ZOL.COM together, in hope of hoping to create synergies.

ZOL.COM + Rongshang + JDHui.com

In view of the fact that the operation of grocery stores in rural China is still poor, the Group hopes to combine ZOL.COM, JDHui.com (The electrical e-commerce platform of the Group) and Rongshang (a SaaS development company) to form a business that can enhance the operational efficiency of the traditional grocery stores. The group will install the SaaS system for the stores for free. The system will provide services such as procurement, operations, logistics and finance to improve operational efficiency. For example, the group can reduce the cost of the stores by collecting the purchase orders, enhancing the profitability of the stores. Currently, the Group has installed SaaS systems for 1,000 stores. We believe that this business will take a few years more before becoming significant to the Group, but we are excited with its potential.

To conclude, the Group's current profit mainly comes from information services, but it will focus on transaction services segment in the future, in order to spread the ascendancy to the information and data services segment by bringing traffic and data through transactions. Taking Ibuychem as an example, as the transaction volume gradually hiked, the B2B platform of the Group can capture enormous user and market data to develop advertising and data analysis services on the platform. We believe that the rest of the B2B platforms of the Group will develop with similar logic and spread the ascendancy to information and data segments.

Earnings forecast

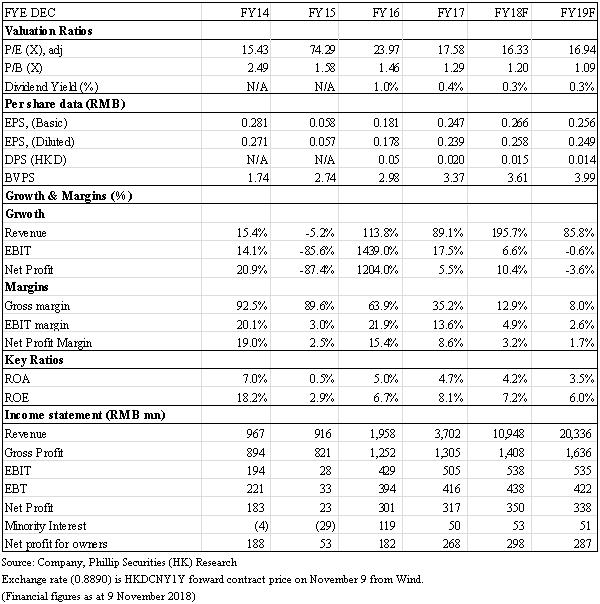

Revenue

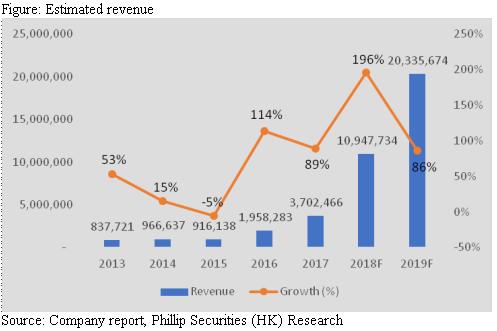

We predict that the revenue of transaction services in 2018/19F will reach RMB 9.27 billion/185.3 billion. Compared with the full year of 2017 and the first half of 2018, the reason for the significant increase in revenue is because we believe that those three major B2B platforms will maintain growth, and that the Union Cotton and China Formwork will be consolidated in May and the second half of this year. Thus, the growth in the second half of 2018 and the full year of 2019 will be very strong.

For data services, we expect revenues to reach RMB 510 million/660 million in 2018/19F. As PanPass is expected to further apply blockchain technology into anti-counterfeiting, and with the increase in traffic volume, more data services will be launched by the Group on the B2B platform.

For information services, we estimate revenue for 2018/19F to be RMB 1.04 billion/1.13 billion. We expect HC360 and ZOL.COM to maintain a slow growth, but as the transaction volume of the transaction services segments rises, the Group will launch more advertising services on the B2B platform, which will boost the growth rate of the segment.

For the O2O business, the management stated that due to the restriction on sales of properties in 2019/20 stated in the contract, it is estimated that the revenue will be hugely reduced. We assume the revenue for 2018/19F to be RMB 140 million/7 million.

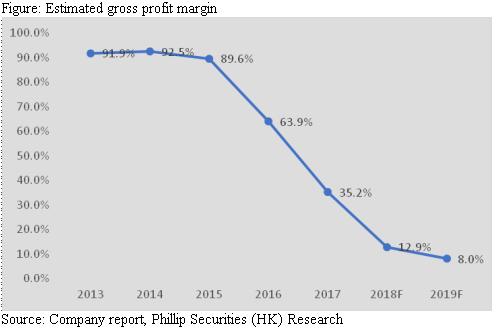

Gross profit margin

Due to the low GPM in transaction services, we expect the GPM to drop as the transaction volume increases, with 12.9%/8.0% in 2018/19F respectively.

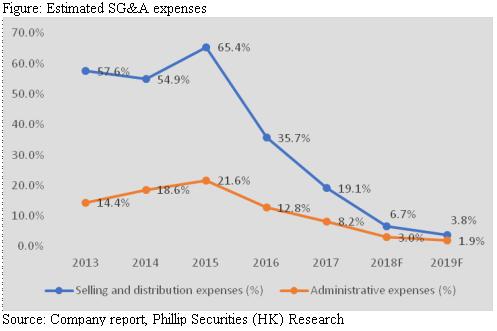

Selling & Administrative expenses

We predict that the selling & administrative expenses as % of revenue will remain stable in 2018/19F respectively. As the revenue significantly rises, we estimate the selling expenses as % of revenue to 6.7%/3.8%; administrative expenses as % of revenue to 3.0%/1.9% in 2018/19F.

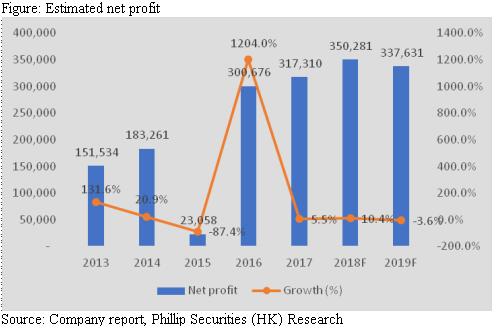

Net profit

Based on the above assumptions, we expect the net profit growth to be 10.4%/-3.6% in 2018/19, reaching RMB 350/340 million. The negative growth in 2019 is because we expect the other income will reduced greatly in 2019 compared to 2018.

Valuation

We believe the transition into vertical B2B platform will create a new growth driver for the Group, where the transaction services are just the beginning. The data that are created by the transaction are of the utmost importance. Although the business model of the Group has changed, we still believe the historical data is still worth to look into. Assuming 2018E P/E ratio to be 22x (the average of the past five years is 24x, we think 22x is within the reasonable range), we derive the target price to be HK$6.58, and initiate a “Buy” rating with 34.8% potential upside. (HKD/CNY=0.889)

Risk

1. The presence of B2B platforms with similar functions

2. Demand for the commodity reduces due to the economic downturn

3. Suppliers refuse to cooperate with the Group

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()