-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

GWM (2333.HK) - Sales Structure Is Continuously Optimized

Wednesday, June 29, 2022  1353

1353

GWM(2333)

| Recommendation | BUY |

| Price on Recommendation Date | $16.440 |

| Target Price | $24.700 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

2021H2 Results Are Slightly Lower than Expected Due to Chip shortage and Rising Raw Material Prices

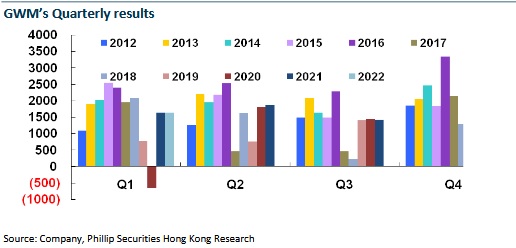

In 2021, Great Wall Motor reported operating revenue of RMB132.17 billion, up 32% yoy. The net profit attributable to the parent company was RMB6.73 billion, up 25.4% yoy. The earnings per share was RMB0.73, and the cash dividend per share was RMB0.07 (tax-inclusive). Including a mid-term dividend of RMB0.3 in 2021, the dividend payout ratio reached 51%. The gross margin in 2021 was 16.16%, down 1.05 ppts yoy. Due to stock option expenses and increased investment in intelligence, electrification and new model R&D, administration expenses and R&D expenses surged to RMB4.04 billion and RMB4.49 billion, respectively, up 58.4% and 46.4% yoy, respectively. Eventually, the net profit margin fell 0.26 ppts to 4.93%.

Last year's results were slightly lower than we expected, mainly due to the serious chip shortage in the automotive industry in H2. The production and delivery pace of vehicle factories was interrupted, while the continuous price rise of raw materials affected the gross margin. In H2, Great Wall Motor saw a 7.5% year-on-year decrease in sales volume, a 10.47% year-on-year increase in revenue, and a 24.2% year-on-year decrease in net profit. Among them, Great Wall Motor reported a year-on-year decrease of 6.9% and 35.8%, respectively in the net profit attributable to the parent company in Q3 and Q4. The gross margin was 17.33% and 15.3%, respectively. Meanwhile, the net profit margin in Q4 fell to 3.9% from 4.9% in Q3 due to factors such as the centralized accrual of year-end employee bonus expenses, the accrual of charging equity of Ora users, and the accrual of equity incentive expenses.

In 2021, Great Wall Motor sold 237 thousand pickups, 907 thousand SUVs and 137 thousand sedans, respectively, a year-on-year increase of 4%, 9% and 135%, respectively. New energy models and high-end models represented by Ora and Wey have made great contributions. In 2021, Great Wall Motor sold 139 thousand new energy vehicles, a year-on-year increase of 137%.

2022Q1 Results Basically Stay Flat, and Sales Structure Is Continuously Optimized

In Q1 2022, Great Wall Motor's operating revenue was RMB33.6 billion, up 8% yoy. The net profit attributable to the parent company was RMB1.63 billion, down 0.3% yoy, basically flat. In Q1, the Company's gross margin was 17.2%, up 2.1 ppts yoy and up 1.9 ppts qoq, mainly due to the product structure optimization and the reduction of one-off factors such as expense accruals, which offset the impact of rising raw material prices and chip shortage.

Since the beginning of 2022, vehicle factories have raised the selling price of products to hedge against the rising cost of raw materials, and Great Wall Motors is no exception. The Company has raised the minimum selling price of Ora Good Cat and Wey by approximately RMB1, 600-12,000. On the other hand, under the premise of short supply, the Company has prioritized the resource allocation for high-value models such as Tank, and discontinued some low-priced models such as Ora Black Cat and White Cat. In terms of the average price of single vehicles, the average price of single vehicles of Great Wall Motor in 2021 was RMB106 thousand, a year-on-year increase of RMB13 thousand. In Q1 2022, the average price of single vehicles was RMB119 thousand, a year-on-year increase of RMB27 thousand, a record high.

Due to the pandemic, Sales Plummet in April but rebound in May

Due to the outbreak of the pandemic in Shanghai, Jiangsu Province and Jilin Province, the supply chain and logistics were blocked in many aspects. Great Wall Motor's sales volume in April plummeted to 53,777 units, down 41.4% yoy and down 46.7% mom, respectively. In May, as the supply chain resumed work and production successively, the company's sales rebounded to 80,062 units as scheduled, a significant increase of 49% month-on-month, and the year-on-year decline narrowed to -7.94%. The cumulative sales volume in the first five months of this year was 417,300 units, a year-on-year decrease of -19.4%, a narrow of 2.3 ppts from the previous four months.

Among the sub-brands, the sales volume of Haval/GWM Pickup/ORA/Wey/Tank in April were 29.1/13.2/3.1/2.3/6 thousand units, respectively, down 47.1%/34.6%/ 58.7%/36.1%, and up 10.3% yoy, respectively. With the gradual improvement of the pandemic situation, the automotive industry, which is the key concern for the resumption of work and production, will gradually fix the supply chain and facilitate the stability and recovery of sales volume. The sales volume of Haval/GWM Pickup/Ora/Wey/Tank in May were 41.7/17/10.8/2.5/8 thousand units, yoy -22.5%/-16.7%/+199.4%/-16.3%/+31.7%, respectively. Haval and ORA have improved significantly mom.

The share of high-value models of the Company continued to rise. In April/May, the Company's sales share of models of over RMB150 thousand yuan reached 18.7%/14.9%. The sales share of models based on the three major technology brands, namely, Lemon, Tank and Coffee Intelligence, have reached 66.2%/64.1%. The share of intelligent models has been up to 89%/82.9%.

Clear GIFT Strategy + Enhanced New Product Cycle + Expectation for Policy Facilitation Promote a Virtuous Cycle of Valuation and Results

Great Wall Motor previously announced the 2025 Strategy - "Green Intelligent Future Technology": The Company plans to achieve the global annual sales target of 4,000 thousand vehicles by 2025, 80% of which are new energy vehicles, with operating revenue exceeding RMB600 billion. In the future, the accumulated R&D investment will reach RMB100 billion. We believe that the core technologies including cobalt-free batteries, hybrid DHT technology, 3.0T+9AT/9HATP2 powertrain, wire-control chassis and smart cockpit, and the Coffee Intelligence platform, is expected to continuously strengthen the Company's strength in new energy vehicles and intelligence in the future, and open up the future valuation space.

In 2022, Great Wall Motor will still usher in an enhanced new product cycle. Wey, Tank and Ora brands will launch multiple new models. Meanwhile, an abundant order in hand is also a strong guarantee for the rapid growth of sales volume and operating revenue after the pandemic.

In addition, in order to stimulate the economy and maintain the continuity of the support policies for the NEV industry, a package of policies to encourage automobile consumption, including the halving of the purchase tax of fuel vehicles and the sending of new energy vehicles to the countryside, has been implemented intensively from the central to local governments. More than 90% of the car purchase demand was met, which exceeded expectations. With the help of policies, this round of auto industry recovery will accelerate. Great Wall Motor's 2.0L and below fuel vehicle sales accounted for 87%, and the ORA cat and its GT version have also been selected for the list of going to the countryside and will benefit first.

Investment Thesis

We expect that negative factors such as production suspension and delay caused by the pandemic are expected to improve or eliminate in H2 2022. In view of the repeated occurrence of the pandemic, the Company's net profit in 2022 may be lower than the forecast. It will take some time to digest the adjusted net profit under the impact of the pandemic and the rising raw material prices. We think that the recovery in capacity utilisation rate is expected to bring resilience to the revenue and net profit from 2023. In the longer term, benefiting from the new technology platform and the enhanced model cycle, Great Wall Motor's long-term layout of the new product system will strengthen barriers, accelerate the share increase, and bring positive returns for a long time in the future.

Considering revised financial forecast, we raised our target price to HK$24.7, equivalent to 24/17/10.4 x P/E in 2022/2023/2024. We gave the rating of “Buy”. (Closing price as at 15 June)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()