-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

GWM (2333.HK) - New Energy Layout Is Accelerating

Thursday, December 8, 2022  1455

1455

GWM(2333)

| Recommendation | BUY |

| Price on Recommendation Date | $11.020 |

| Target Price | $14.100 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

With a Slight Improvement in the Overall Sales Volume in October, the Product Sales Structure Is Continued to Be Upgraded

Great Wall Motors reported a sales volume of 100.2 thousand units in October, down 11% yoy and up 7% mom. The year-on-year decline was mainly due to the disruption of demand of major automobile consuming provinces amid the spread of the pandemic in multiple places. However, Great Wall Motors displayed outstanding performance in the overseas sales in October. A total of 21,052 units were delivered, up 50% yoy and up 12% mom, accounting for 21% of the total sale volume. From January to October, Great Wall Motors` cumulative sales volume reached 903 thousand units, down 9.4% yoy. In particular, 107,870 new energy vehicles were sold accumulatively, up 9.95% yoy, accounting for 11.9% of the total sales volume. The proportion of the Company's high-value models continued to increase. From January to October 2022, Great Wall Motors` sales volume of models above RMB200 thousand accounted for 14.62%, up 4.93 ppts yoy; the sales volume of intelligent models accounted for 85.84%, up 10.54 ppts yoy; and the sales volume of the models of three major technology brands accounted for 70.56%, up 11.67 ppts yoy.

Haval and Tank Accelerate the Launch of New Energy Layout

In terms of sub-brands, Haval sold 63,759 units, up 1.9% yoy and up 18.2% mom, of which the sale volume of the main model Haval H6 was 35,127 units, up 28.5% yoy. In August, Haval announced its new energy strategy, accelerating its transition to the new energy track in a comprehensive manner, and plans to increase the sales proportion of new energy vehicles to 80% by 2025 and stop selling the traditional fuel-powered vehicles by 2030. At the end of September, the 3rd Gen Haval H6 DHT-PHEV was officially launched, which shows the stimulating effect on the total sales volume of Haval models. Haval is expected to launch a total of seven new energy models in two categories by the end of next year, including five plug-in hybrid electric models and two hybrid electric models. In the fourth quarter of this year, two new energy models, namely, the Shenshou PHEV and the Big Dog PHEV, will be launched. Haval is comprehensively accelerating the new energy layout.

Tank reported a sales volume of 12,753 units, up 28.2% yoy and up 1.1% mom. The average price of the Tank 300 and the Tank 500 exceeded RMB200 thousand and RMB300 thousand, respectively, which fully establishes the Company's ability to mine the characteristic segment. In the future, in addition to increasingly enriching the co-creation versions of existing models, new models such as the Tank 400, 700 and 800 will be launched in succession. At the previous Chengdu Motor Show, Tank showed the Tank 300 HEV and the Tank 500 PHEV, which are expected to be launched by the end of the year. Tank is also promoting the new energy layout.

Ora and Wey Are Still in the Transition Period

Ora delivered 5,572 units, down 57.9% yoy and down 26.7% mom. The decline was mainly affected by the discontinuation of low-priced models such as the Good Cat and the White Cat, reflecting that the brand is still in the transition period. On October 31, the new model Lightning Cat, which is positioned as a "super streamlined pure electric coupe", was officially launched. Within 24 hours of its launch, the large orders of the new model reached 15,305 units. The market layout has achieved initial results. It is expected to be a hot-selling model in the future. In terms of product planning, Ora will also launch multiple models such as the Punk Cat and the Cherry Cat in the future.

Wey reported a sales volume of 2,427 units, down 58.5% yoy and up 3.1% mom, reflecting the fierce market competition in the high-end models of self-own brands. In the future, Wey will make breakthroughs in the diversity of models. Retro SUV model "Yuan Meng", large six-seat SUV and MPV models, and sedan model are expected to be launched in succession. The product matrix will be encrypted to facilitate the sales rally.

GWM Pickup delivered 15,697 units, down 23.2% yoy and down 8.3% mom, of which the GWM Poer delivered 10,155 units, down 19.8% yoy and down16.1% mom. The sales volume has exceeded 10 thousand units for 27 consecutive months.

Investment Thesis

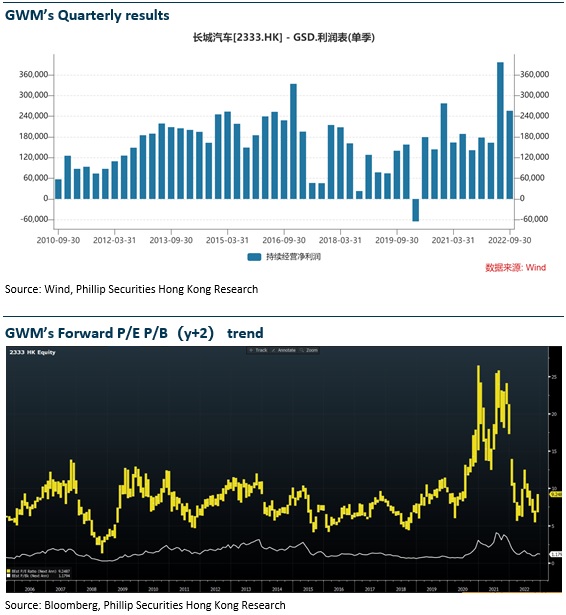

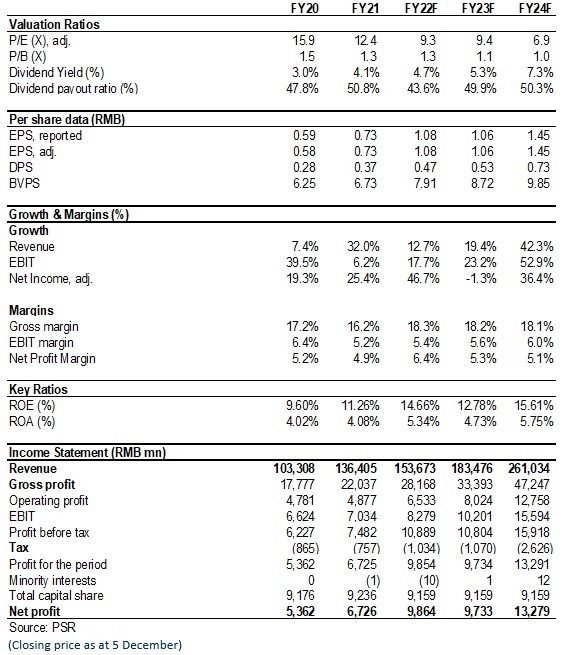

In 2022, due to the disruption resulting from the pandemic, the Company's original strong product cycle has been delayed. However, with the gradual disappearance of the negative factors, the recovery of capacity utilisation and the launch of a series of new models are expected to bring elasticity to the revenue and net profit. We think that Great Wall Motors` long-term layout of new technologies and new product systems will facilitate its share rally and bring stable returns in the future.

Considering revised financial forecast, we raised our target price to HK$14.1, equivalent to 11.8/12/8.8 x P/E in 2022/2023/2024. We gave the rating of “Buy”. (Closing price as at 5 December)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()