-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

SH Pharma (2607.HK) - Rapid growth in core segments, promising in innovation transformations

Tuesday, January 7, 2020  5606

5606

SH Pharma(2607)

| Recommendation | Accumulate |

| Price on Recommendation Date | $15.160 |

| Target Price | $18.060 |

Weekly Special - 3306 JNBY Design Limited

Result Update

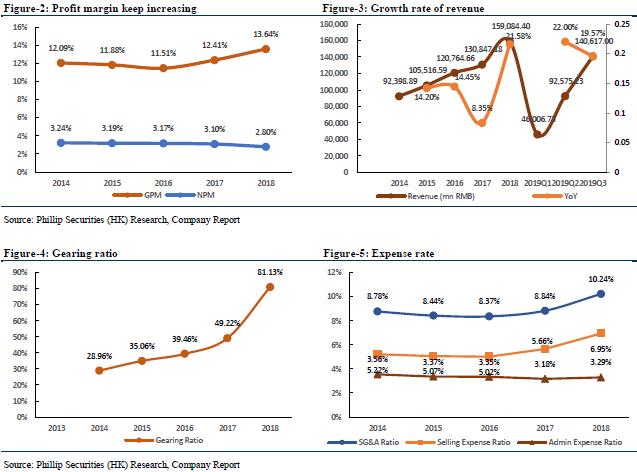

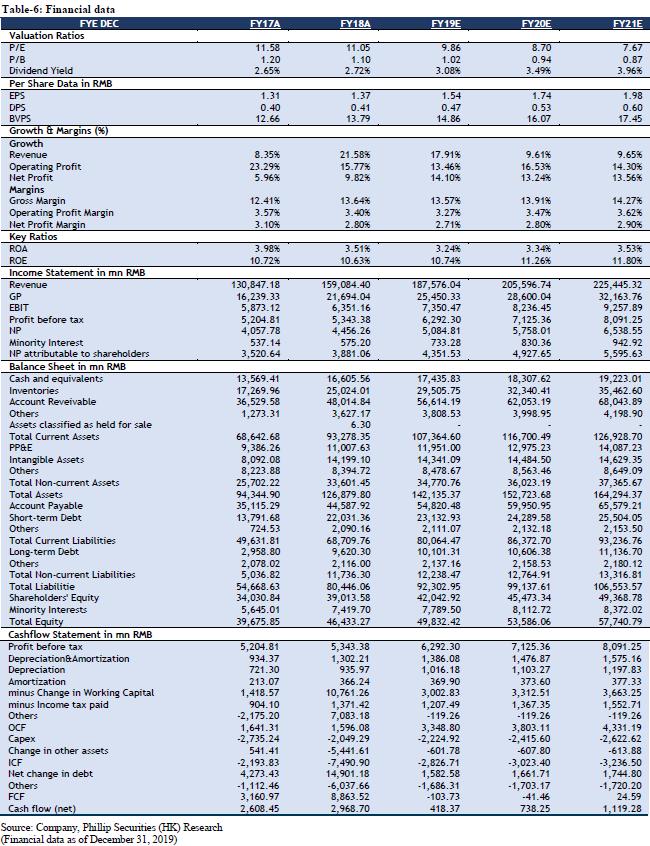

For the nine months ended September 30, 2019, the company recorded operating income of RMB 146.617 billion, an increase of 19.57% YoY, and its main business continued to grow rapidly. Of which, the pharmaceutical manufacturing sector realized revenue of RMB 17.682 billion, a YoY increase of 24.05%. The pharmaceutical business realized revenue of RMB 129.235 billion, an increase of 18.95% YoY (among which, the pharmaceutical distribution business achieved sales revenue of RMB 121.218 billion, an increase of 18.56% YoY; the pharmaceutical retail business achieved sales revenue of RMB 5.908 billion, an increase of 15.94% YoY). The company realized a net profit attributable to shareholders of listed companies of RMB 3.399 billion, a YoY increase of 0.80%; the main business of the pharmaceutical manufacturing sector contributed a profit of RMB 1.540 billion, a YoY increase of 20.56%; the main business of the pharmaceutical business contributed a profit of RMB 1.526 billion, a YoY increase Increased by 15.73%; the participating companies contributed profits of RMB804 million, an increase of 48.13% YoY. The company's comprehensive gross profit margin was 13.70%, a decrease of 0.11 percentage point compared with the same period last year; the gross profit margin of the pharmaceutical manufacturing sector was 57.54%, a decrease of 0.10 percentage point compared with the same period last year, and the average gross profit margin of 60 key varieties was 71.71%; the gross profit margin of pharmaceutical distribution was 6.40%, a YoY decrease of 0.27 percentage points; the gross profit margin of pharmaceutical retail was 14.10%, a YoY decrease of 1.02 percentage points.

Continue to deepen one product one policy, accelerate innovation transformations

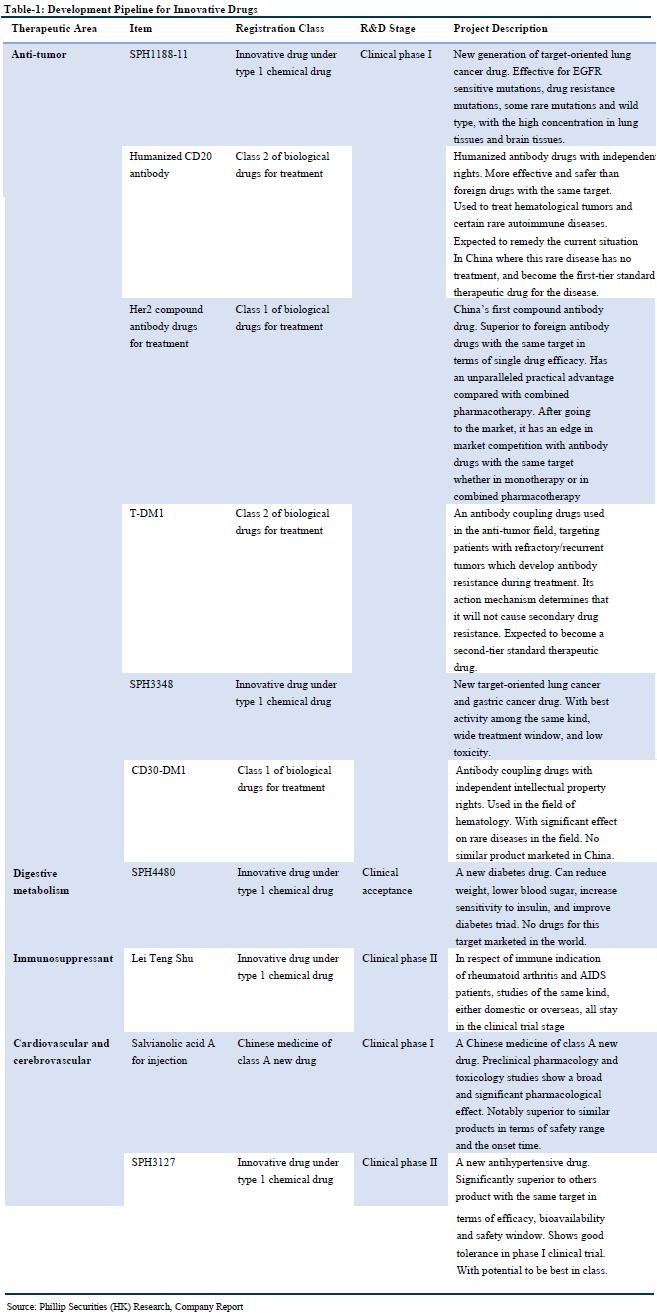

In the pharmaceutical manufacturing sector, the company focuses on key products and continuously increases its market share, such as tanshinone IIA sodium sulfonate injection. From January to September 2019, it realized sales revenue of RMB 1.14 billion, a YoY increase of 76.39%. According to the life cycle of different products, the company has formulated a differentiated terminal strategy, and the promotion effect is significant. In January-September 2019, Ulinastatin for injection achieved sales income of RMB 673 million, a YoY increase of 32.91%; hydroxychloroquine sulfate tablets achieved sales income of RMB 587 million, a YoY increase of 20.56%; Hongyuanda achieved sales income was 366 million yuan, a YoY increase of 31.75%. Eureklin for injection achieved sales of 275 million yuan, a YoY increase of 20.85%.

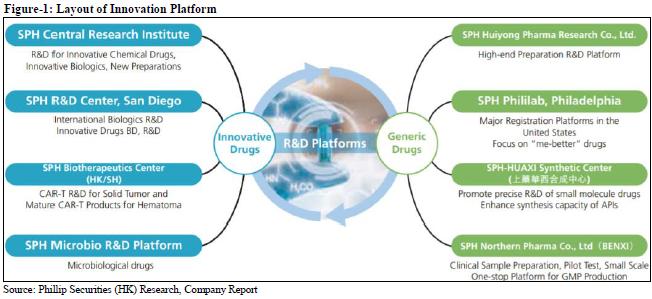

In addition, the company continued to accelerate innovation transformation. From January to September 2019, R & D expenditure was RMB 860 million, an increase of 13.74% YoY; 73 invention patent applications were completed, 24 invention patent authorizations, and 20 utility model authorizations, totaling 117 patents. On September 17, the company signed a joint venture agreement with BIOCAD, the largest biopharmaceutical company in Russia, to introduce adalimumab biosimilars, trastuzumab biosimilars, bevacizumab biosimilars, and PD-1 products. Permanent and exclusive R & D, production, sales and other commercialization rights of the six blockbuster biopharmaceuticals in Greater China, including the joint venture company, will be the sole platform for BIOCAD in Greater China.

The company continued to advance the consistency evaluation of the quality and efficacy of generic drugs, further improved the production process and the quality of medicines. As of the end of September, the company has completed more than 40 product specifications for BE testing and application, of which 6 varieties have passed the consistency evaluation. Two varieties of ceftriaxone sodium for injection and lansoprazole for injection have completed a BE test and declared to CDE. Beclometasone propionate inhalation aerosol has been approved for supplementary application, 3 specifications of rosuvastatin calcium tablets have been declared for production, and lenalidomide capsules and rivaroxaban tablets have been completed for BE filing. Capsaicin, a commonly used drug for clinical chemotherapy, has been completed. Tabin has also officially started the BE trial.

Pharmaceuticals services continue promoting, expand the terminal market

In November 2019, the company continued to promote the implementation of new distribution and new retail development strategies, promote the rapid development of advantageous and innovative services, clarify the regional development strategies of key provinces, and continue to promote key provinces such as Guangdong, Shandong, Heilongjiang, Jilin, and Liaoning. The platform construction utilizes the policy opportunities brought by the two-vote system and volume purchase, integrates market resources, and strictly controls the accounts receivable, while quickly seizing the pure-sale terminal market. Among the large varieties, Pfizer's Peer vaccine market has been rapidly expanding, which has led to rapid increase in distribution revenue. During the reporting period, the company achieved 2.122 billion in distribution revenue from vaccine business, a YoY increase of 92.33%. The company has launched a new business, providing efficient and compliant sales channels for imported drugs and new special drugs that are not covered by medical insurance, and after the corresponding products enter the medical insurance, the company's distribution network will be used to provide hospital services. The one-stop service chain of innovative pharmaceutical companies has joined forces to win the general distribution rights for new varieties of large pharmaceuticals.

Financial Forecast and Valuation

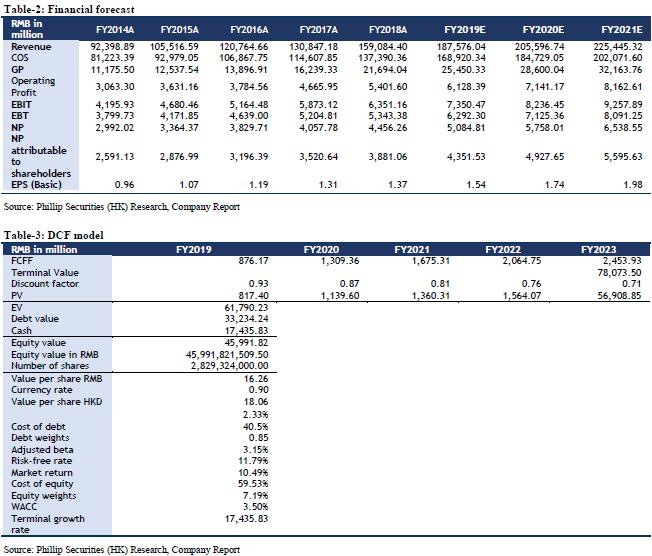

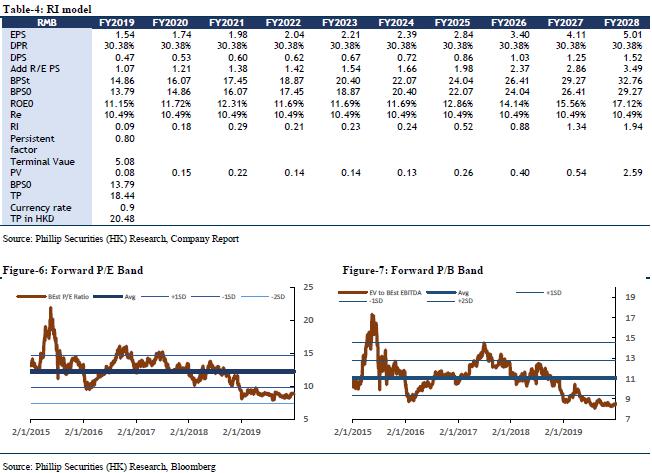

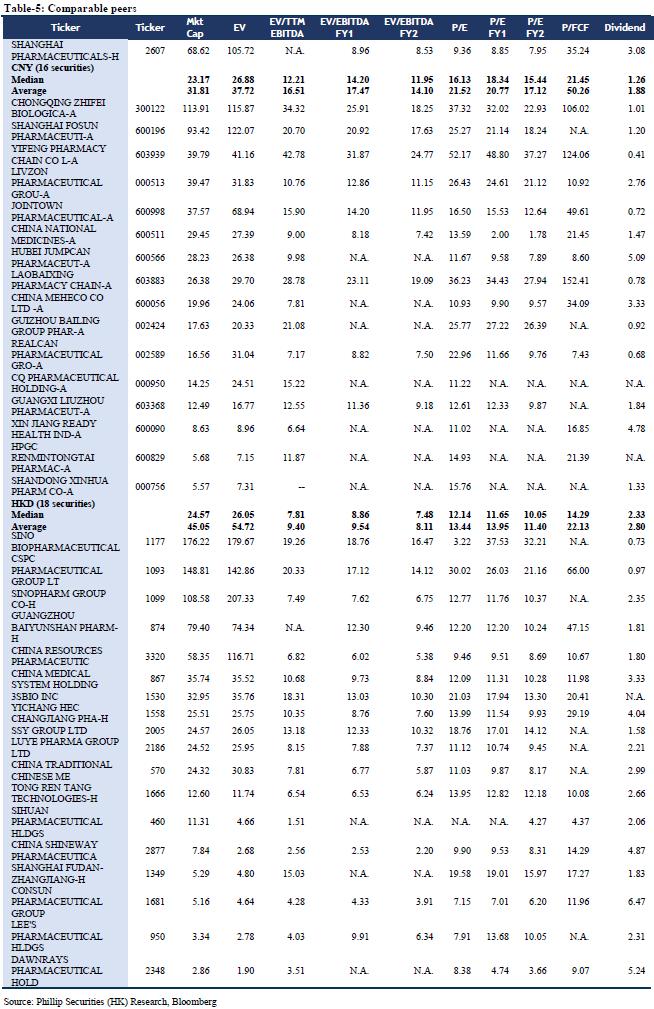

We forecast that the company's FY19/FY20/FY21 income will be RMB 187.58/205.60/225.44 billion, representing an increase of 17.91%/9.61%/9.65% YoY; net profit attributable to shareholders will be RMB 4.35/4.93/5.60 billion, increasing 12.12%/13.24%/13.56% YoY; corresponding EPS will be RMB 1.54/1.74/1.98. We use DCF model and residual income model to value the company. Assuming equity cost is 10.49%, debt cost is 2.33%, and WACC is 7.19%. We get PT of HKD 18.06 and HKD 20.48 respectively. The lower valuation result corresponds to FY19/FY20/FY21 10.57x/9.33x/8.22x PE, which has an increase of +19.14% compared to the current price (HKD 15.16 as of December 31, 2019), giving an “Accumulate” rating.

Risk

The launch of new products fails expectations; Industry policy risk.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()