-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Galaxy Entertainment (27.HK) - Q3 results slightly better than expected

Thursday, October 29, 2015  17067

17067

Galaxy Entertainment(27)

| Recommendation | Buy |

| Price on Recommendation Date | $26.800 |

| Target Price | $35.000 |

Weekly Special - 3306 JNBY Design Limited

Q3 results slightly better than expected

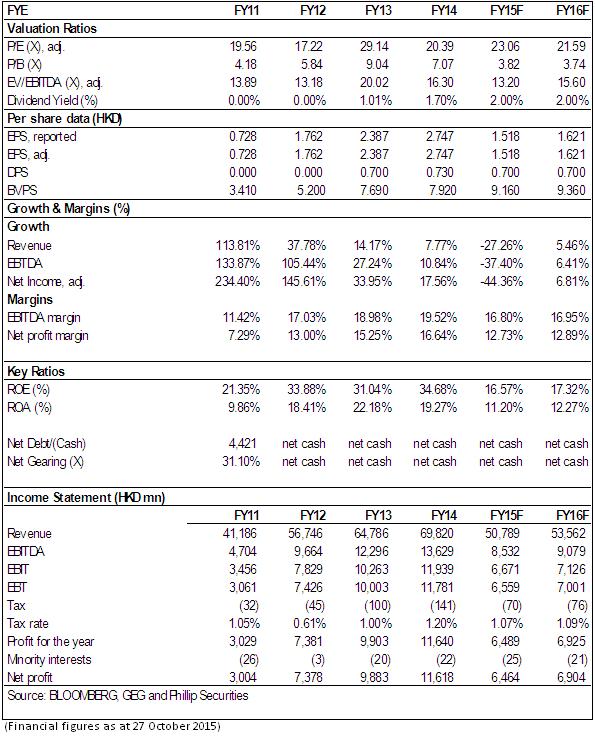

Galaxy Entertainment recorded revenue of HKD12.3 billion, down 29% yoy, but up 5% QoQ. The Company's adjusted EBITDA amounted to HKD2.1 billion, down 36% yoy, but up 13% QoQ, including played unlucky which reduced EBITDA by approximately HKD130 million.

In Q3, the occupancy rate of the Company's hotels maintained as high as 99%. Two main brands of the Company had diversified performance. Galaxy Macau performed better in the period under review: recorded revenue of HKD8.7 billion, down 22% yoy, but up 9% QoQ; adjusted EBITDA amounted to HKD1.7 billion, down 30% yoy, but up 19% QoQ. It is worth to point out that Galaxy Macau recorded non-gaming revenue of HKD742 million, up 92% yoy and up 60% QoQ.

Star World Hotel recorded revenue of HKD2.9 billion, down 48% yoy and down 7% QoQ; adjusted EBITDA amounted to HKD514 million, down 43% yoy, but up 1% QoQ.

Overall, Galaxy Entertainment had good performance in Q3 and growth was recorded compared to Q2. The rate of decline of income and profit for the whole year narrowed and it reflected that the consistent downturn of VIP venue business was partially compensated by the growth of mass venue business. Moreover, demand for vocations and the launch of new projects also made Galaxy Entertainment more attractive to investors.

New change on operation performance

Fast growth of non-VIP gaming (mass gaming, slots and non-gaming), reduction on cost and launch of new projects were the positive changes on the Company's operation performance. Even though the gaming business of Macau has not yet moved away from depression, the above changes enhanced the Company's sustainable growth and gain on market share.

The market focus of Galaxy Entertainment is turning non-VIP gaming: the contribution of income from mass gaming, slots and non-gaming increased from one-third in 2014Q3 to the current approximately 50%; and such income contributed to the main part of EBITDA. Income from mass gaming, slots and non-gaming is expected to increase in amount as well as in weighting of EBITDA.

The development of Galaxy Macau Phase 2 and Broadway Macau in 2015Q2 provided the Company with new growth momentum. Broadway Macau recorded revenue of HKD189 million in Q3, and adjusted EBITDA of HKD-1 million (loss). A breakeven was basically recorded in the first financial quarter under operation. Moreover, effort made on cost reduction enabled a saving of more than HKD100 million in 2015Q3, and is expected to save HKD800 million in the upcoming 18 months.

Balance sheet kept solid

As at the end of September 2015, Galaxy Entertainment owns cash amounted to HKD6 billion, with net cash of HKD4.8 billion. Significant decrease of total debt was caused by the clearing of debts related to treasury management. Major items of capital expenditure in the coming 1 year include the site investigation works of Cotai Phases 3 & 4; and also the strategic investment of overseas markets. However, the amount of expenditure is expected to be limited.

Risk

The regulatory policies on the gaming business of Macau by the Central Chinese Government;

Weaken demand for VIP gaming;

Stronger competitors in Macau and nearby areas;

Labour cost and inflation in Macau.

Valuation

Q3 business data of Galaxy Entertainment is slightly better than expected, reflecting the positive changes of the fundamentals of the Company and also the steady recovery of demand. The Macau government has released some positive signals regarding gradual relaxation of regulations on gaming business in Macau and stimulation to tourism of Macau. We think these signals would generate positive boosting effects on the gaming business of Macau and particularly on Galaxy Entertainment. We give a rating of “Buy”, with the 12-month target price of HKD35, which is equivalent to 15.6x of 2016e EV/EBITDA and 22x of 2016e P/E. (Closing price as at 27 Oct 2015)

Financial Sheet

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()