-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

PAX Global Technology Limited (327.HK) - Better-than-expected growing results in 2015H1

Friday, September 18, 2015  15514

15514

PAX Global Technology Limited(327)

| Recommendation | BUY |

| Price on Recommendation Date | $8.000 |

| Target Price | $11.000 |

Weekly Special - 3306 JNBY Design Limited

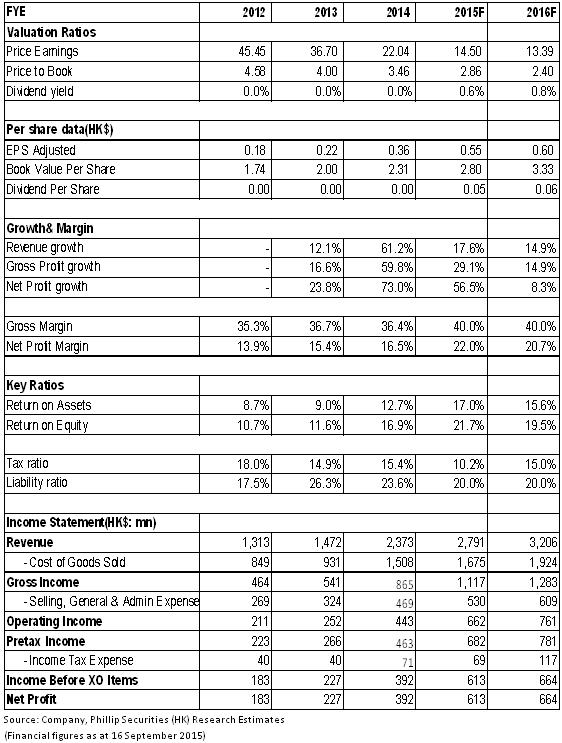

Pax Global is a EFT-POS terminal solution provider. The Company ranked the third worldwide in terms of supply of EFT-POS terminals in 2014. According to the 2015 Interim Report, its revenue increased 10.1% yoy to HKD1.11 billion in 2015H1; profit attributable to shareholders surged 55.9% to HKD0.31 billion, representing HKD0.279 per share. The Company also announced an interim dividend of HKD0.02 for each ordinary share and this is the first dividend payout since the Company was listed.

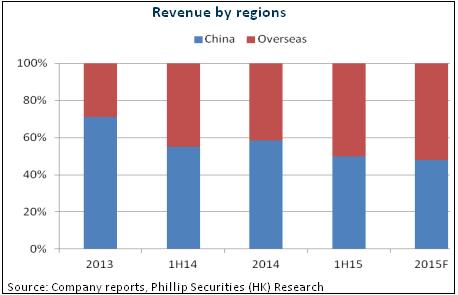

Nearly 95% of the Company's revenue was contributed by the business of EFT-POS terminal, which was up 11.6% yoy in 2015H1, to HKD1.05 billion. It is mainly due to sales in overseas markets recorded a yoy growth of 22.7%, to HKD0.56 billion. Sales in overseas markets surpassed sales in Chinese market for the first time. In perspective of profitability, with the increase of portion of revenue from overseas markets, the Company's overall gross profit margin raised 3.7 ppts yoy, to 41.5%.

From the perspective of global development in finance industry, EFT mode would gradually replace the traditional mode of cash payment. For example, Denmark would become the first country in the world which no longer uses cash as a medium of transaction. It is worth to note that, in the era of mobile internet, EFT would be more convenient. Pax Global is expected to be benefitted from the trend. Thereinto, the American market carries the growth highlights, where revenue recorded in 2015H1 surged 78.2% yoy. High-speed growth is still expected.

Despite of unsatisfactory sale performance in 2015H1, the Company is expected to regain growth in Chinese market in 2015H2 and we are optimistic about this. First of all, the delayed confirmation of income in first half of the year will be booked in. Moreover, the new product of wireless POS terminal was launched in June. In addition, according to the most recent policy, the administrative fee of using bank cards would be lowered generally, and this would be particularly beneficial to dining and entertainment industries. We believe the launch of such policies would lower the expenses of shops and encourage more shops to use POS terminals.

High-speed growth is still expectable

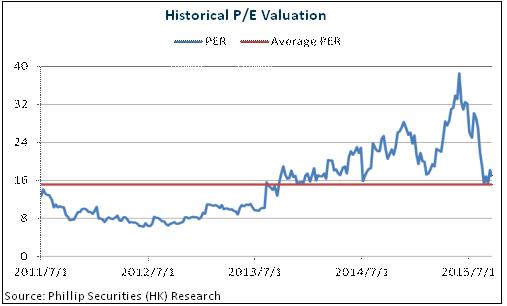

E-payment has become a global trend. Pax Global's business in overseas markets demonstrated high-speed growth, and has acquired a leading position in the industry. In addition, Pax Global's sufficient cash position supported its external expansion, and thus consistent growth is expectable. We grant a rating of “Buy” to Pax Global with a target price of HK$11, equivalent to 20x of 2015 forecasted EPS. (Closing price as at 16 Sep 2015)

Better-than-expected growing results in 2015H1

Pax Global is a EFT-POS terminal solution provider. The Company ranked the third worldwide in terms of supply of EFT-POS terminals in 2014. According to the 2015 Interim Report, its revenue increased 10.1% yoy to HKD1.11 billion in 2015H1; profit attributable to shareholders surged 55.9% to HKD0.31 billion, representing HKD0.279 per share. The Company also announced an interim dividend of HKD0.02 for each ordinary share and this is the first dividend payout since the Company was listed.

Nearly 95% of the Company's revenue was contributed by the business of EFT-POS terminal, which was up 11.6% yoy in 2015H1, to HKD1.05 billion. It is mainly due to sales in overseas markets recorded a yoy growth of 22.7%, to HKD0.56 billion. Sales in overseas markets surpassed sales in Chinese market for the first time, reaching 50.1%. On the other hand, revenue in Chinese market slightly dropped 0.1%, to HKD0.55 billion, due to the adjustment of business strategy by the Company and confirmation of partial revenue being delayed.

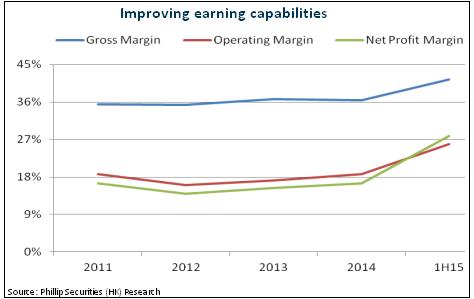

In perspective of profitability, the average selling prices in overseas markets are higher and thus the profit margins are higher than Chinese market. With the increase of portion of revenue from overseas markets, the Company's overall gross profit margin raised 3.7 ppts yoy, to 41.5%. Meanwhile, benefitting from economies of scale, the Company's selling expenses and administrative expenses dropped 0.9 ppts yoy, to 18.6%. Moreover, the Company's subsidiary, Wonder Pax, obtained the approval from the Chinese tax authorities in April 2015 for a preferential tax treatment: the Company is fully exempted from corporate tax for two years, beginning 2014, followed by a 50% tax exemption for the ensuing three years. The over provision of tax accrued by Wonder Pax, of HKD32.98 million, was credited to the profit and loss in 2015H1.

Overseas markets consistently bring growth momentum

From the perspective of global development in finance industry, EFT mode would gradually replace the traditional mode of cash payment. For example, Denmark would become the first country in the world which no longer uses cash as a medium of transaction. It is worth to note that, in the era of mobile internet, EFT would be more convenient. Pax Global is expected to be benefitted from the trend. The Company has already set up establishment in over 80 areas and countries worldwide. The future target is raising the proportion of revenue from oversea to over 70%.

Firstly, the American market carries the growth highlights, where revenue recorded in 2015H1 surged 78.2% yoy. High-speed growth is still expected. Currently, EMV certification in America has entered the fast lane, while Apple Pay is also expected to enhance the development of mobile payment. The Company was joined by the sales and research teams of Equinox, the former second largest EFT solution provider in America. The American market of the Company is expected to enter the stage of gain. The Company's target in American market is raising the market share from 2-3% in 2014, to 7-8% in 2015, followed by a double in 2016.

Secondly, the business of Pax Global has gradually developed in Western Europe and the Company has been certified in markets where there is great demand for traditional POS machines, including UK, Germany and Italy etc. Particularly in Italy, the Company announced on 20 May that it would acquire 70% of the post-expansion equity of Pax Italia, which is the sole distributor of the Company in Italy, at the cost of Euro4.67 million. Such acquisition not only brought considerable additional income to the Company, but also enhanced the market position of the Company in Europe. The Company also targeted at reaching a market share of 20-25% in Italy this year, and 30-35% next year. Italy currently needs 200,000 to 250,000 POS machines per year.

Moreover, in emerging markets, Pax Global has become the first provider obtaining the certification of mobile POS (mPOS) in Brazil. Since 2014, the Company has solidly kept an absolute leading position in the Brazilian mPOS market. Meanwhile, Pax Global has started to launch new products including several multi-media retail payment terminals (“Multilane”) and mPOS in the Middle East market, which also can support the business expansion by the Company in the region.

Mainland market may regain growth in 2015H2

Despite of unsatisfactory sale performance in 2015H1, the Company is expected to regain growth in Chinese market in 2015H2 and we are optimistic about this. First of all, the delayed confirmation of income in first half of the year will be booked in. Moreover, the new product of wireless POS terminal was launched in June, with selling price set as HKD500-600, which is lowered than the traditional ETF-POS terminal. This can satisfy the customers who are price-sensitive and need fewer functions on the POS terminals. Such new product is expected to assist the Company to regain market share.

Moreover, the Company has taken leading position in domestic Chinese market. However, there are only 12 POS terminals for every 1000 people in Chinese market currently; while there are 20 to 25 POS terminals for every 1000 people in developed countries, which is more than double to the number in China. Therefore, the domestic Chinese market still has wide room for development.

In addition, the state policies emphasis on supporting the establishment of electronic transaction network, and this would further stimulate the demand for ETF-POS terminals. According to the most recent policy, the administrative fee of using bank cards would be lowered generally, and this would be particularly beneficial to dining and entertainment industries. We believe the launch of such policies would lower the expenses of shops and encourage more shops to use POS terminals.

Catalyst

Apple Pay promotes faster popularity of NFC worldwide;

Sufficient net cash promotes acquisition worldwide;

Accelerated expansion of overseas markets.

Risk

Worse-than-expected growth of demand in POS industry;

Risk of doing business in overseas markets;

Intensified competition affecting profitability.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()