-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Shenzhen Investment (604.HK) - Broadly Completed The Exit From Lower Tier Cities

Tuesday, October 17, 2017  17062

17062

Shenzhen Investment(604)

| Recommendation | Accumulate |

| Price on Recommendation Date | $3.660 |

| Target Price | $4.050 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

- Significant rise in gross profit margin, primarily contributed by the recognition of the sales of properties in Shenzhen, whose gross profit margin can be as high as 66% (Overall GPM of Shenzhen: 50.7%)

- Taking advantage of the recovery of property market in Tier 3 and Tier 4 cities, the company further decreased its exposure in these cities and significantly decreased the proportion of these in cities in the land bank to 34%

Business Overview

The 1H2017 revenue declined but net profit surged: The revenue of Shenzhen Investment in 1H2017 declined 14.6% to HK$5,454Mn. The decline is primarily caused by the tight regulation in Shenzhen and the fact that several projects in Shenzhen will only be recognised in 2H2017 and FY2018, thereby affecting the revenue in 1H2017. Despite the drop in revenue, gross profit rose 1.9% to HK$2,197Mn in 1H2017 due to the rise in gross profit margin from 33.8% in 1H2016 to 40.3% in 1H2017. The large increase in gross profit margin is caused by the increase in the revenue contribution by Shenzhen, whose contribution was 69.4% in 1H2017 and gross profit margin was 50.7%. The profit attributable to the shareholders in 1H2017 rose 119.3%, primarily caused by the disposal gain of the projects in Tier 3 and Tier 4 cities, which amounted to HK$3,325Mn (Before attribution to shareholders and minority interest). Despite the increase in earnings, the dividend per share remained at HK$0.07 per share.

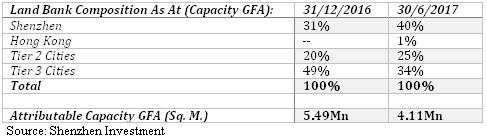

Further optimised the land bank: Shenzhen Investment continued to enhance the quality of its land bank by disposing land in Tier 3 and Tier 4 cities. In 1H2017, the company disposed 5 projects located in Sanshui, Taizhou, and Jiangyan through public listing for sales, allowing the company to achieve an after tax gain of HK$3.33Bn. Coupled with the disposal of land in Heyuan in FY2017, the disposal of these projects signals the broad completion of the company's exit in the Tier 3 and Tier 4 cities, with the contribution to the land bank by these cities dropping from 49% in FY2016 to 34% in 1H2017, significantly enhancing the quality of the land bank. The company also expanded its land bank and obtained a residential land in Tuen Mun, Hong Kong (GFA: 43,938 square metres, 50% Interest) with Road King Infrastructure.

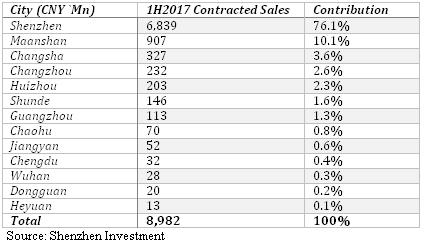

Contracted sales in first 9 months was weak in comparison with peers: Shenzhen Investment's accumulated contracted sales in the first 9 months of FY2017 amounted to CNY10.24Bn, representing a YoY drop of 43%. The accumulated contracted sales area in the same period was 480,079 square metres, representing a YoY drop of 37%. Recognised revenue in 1H2017 dropped 14.6% to HK$5,454Mn. The drop in revenue is primarily contributed by the tightened regulations in China especially those in Shenzhen. According to the 1H2017 report, 76% of the contracted sales in the first half of FY2017 were contributed by Shenzhen. Since Shenzhen projects usually have high profit margins, we expect the reduction in the contracted sales could be partially offset by the improvement in the overall profit margins.

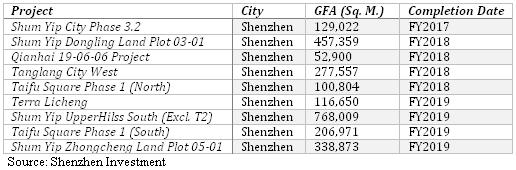

Over the next two years, the company has some large properties to release, mostly in FY2019 and with some projects located in prime locations in Shenzhen. We believe these projects will receive good demand despite the tightened regulations in Shenzhen. Examples of these projects include:

Investment Thesis, Valuation and Risk

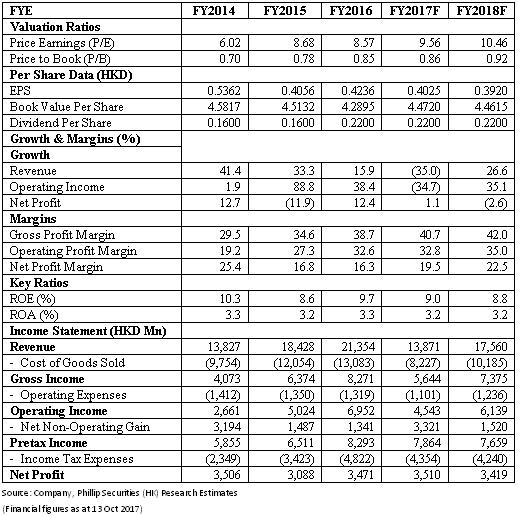

Our valuation model suggests a target price of HK$4.05: Despite the drop in recognised revenue and contracted sales, we maintain our optimistic view to Shenzhen Investment because of its valuable land resources, i.e. those in Shenzhen, and the recent revaluation of China property stocks. We also believe the Shenzhen projects can raise the profit margin, which the improvement in profit margin can offset some of the negative effect on revenue brought by the tightened regulations. Therefore, we have adjusted Shenzhen Investment's target price to HK$4.05, corresponding to a P/E and P/B of 9.56x and 0.86x, with an `Accumulate rating assigned. (Closing price as at 13 Oct 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()