-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Overseas Land & Inv (688.HK) - Land Reserve Quality Continues to Improve

Thursday, June 22, 2017  17445

17445

China Overseas Land & Inv(688)

| Recommendation | Accumulate |

| Price on Recommendation Date | $22.850 |

| Target Price | $25.100 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

- Completed Citic Assets Acquisition, increasing the quality of the land reserve especially that Citic Assets contains substantial amount of land and projects in both Tier 1 and Tier 2 Cities, e.g.: Tier 1 Cities land reserve increased 120%

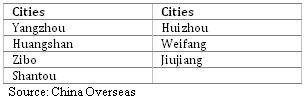

- Reduced exposures in Tier 3 cities by disposing about 9.52Mn square metres of land reserve in these cities, such as Yangzhou and Huizhou, to the associate company China Overseas Grand Oceans

- Significant decrease in total debt and net gearing ratio, which dropped from 37.3% in FY2015 to 7.5% in FY2016

Business Overview

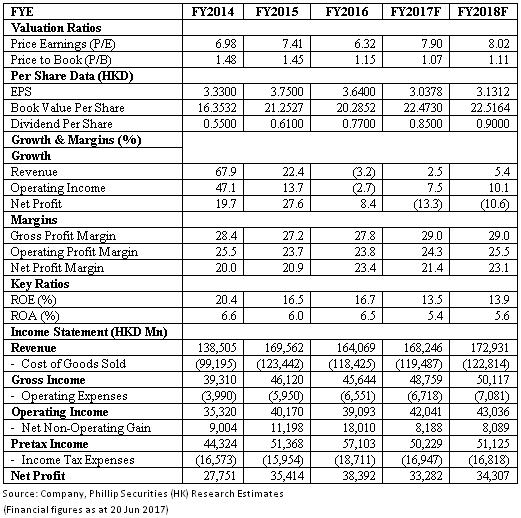

Stable FY2016 result: In FY2016, China Overseas recorded a 3.2% drop in revenue from HK$169,562Mn to HK$164,069Mn. Property sales was strong throughout FY2016, with aggregate property contracted sales exceeding the target contracted sales of HK$200Bn. The aggregate contracted sales amounted to HK$210.6Bn, a rise of 16.6% in comparison with FY2015. Net profit however increased 8.4% from HK$35,414Mn to HK$38,391Mn, mainly caused by the disposal of the company's subsidiaries in May and October 2016, contributing HK$10,175.9Mn of one-off gain to the company. In FY2016, Earning per Share decreased HK$0.13 to HK$3.64. China Overseas declared a final dividend of HK$0.42, an increase of HK$0.01 in comparison with FY2015.

The quality of the land reserve continues to increase: In FY2016, China Overseas increased the size of its land reserve significantly from 41.4Mn square metres in FY2015 to 56.8Mn square metres in FY2016, an increase of 37.0%. In particular, the land reserve in Tier 1 cities more than doubled and increased from 4.6Mn square metres to 10.1Mn square metres, an increase of 120%. The significant growth in the land reserve can be attributed to China Overseas completing the Citic Asset Acquisition. Through this acquisition, China Overseas increased the GFA of its land reserve by 31.55Mn square metres and increased the quality of its land reserve, with a majority of the projects locating in Tier 1 Cities and Tier 2 Cities. In general, the newly acquired assets are mainly residential projects spanning across more than 20 cities in China.

Apart from the Citic Asset acquisition, China Overseas has been actively enhancing the land reserve by reducing the company's exposure in the Tier 3 Cities. The property development projects in these cities generally face weaker demand and lower profit margin than cities of higher tiers. In October 2016, China Overseas sold about 9.52Mn square metres of land reserve to its associate China Overseas Grand Oceans. The disposed land are located in cities such as:

Profitability is expected to be high relative to the industry: With the proportion of land contributed by lower tier cities decreasing, China Overseas's profitability is expected to remain at a high level in comparison with the rest of the industry. The Tier 3 Cities assets are held by its associate company China Overseas Grand Oceans and therefore the sales of the lower tier cities properties would not affect the gross profit margin of China Overseas. Moreover, the recent recovery of the Tier 3 Cities property market enables China Overseas to spin-off its Tier 3 Cities land reserve at a higher price and at the same time generate higher profit via its associate China Overseas Grand Oceans.

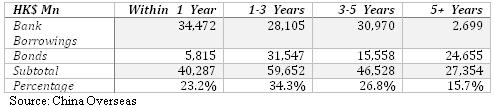

Financial position continues to be strong: The capital structure of the company remains healthy and in FY2016, the net gearing ratio of the company decreased significantly from 37.3% in FY2015 to 7.5% in FY2016. Cash on hand increased to HK$157.2Bn, contributing to about 27.5% of total assets, indicating a strong liquidity position. Both financial figures are at their strongest point across the four-year period, as shown by the following table:

Besides, the company does not have a large short term obligation to meet and the majority of the debt are due more than a year later. In particular, only 23.2% of the total debt, or HK$40,287Mn, are due within a year.

Investment Thesis, Valuation and Risk

Our valuation model suggests a target price of HK$25.10: China Overseas has achieved a stable result in FY2016 but in terms of contracted sales, it has produced a sizable growth. The Citic Asset Acquisition and the disposal of Tier 3 Cities land reserve to China Overseas Grand Oceans enable the company to increase the quality of its land reserve. We also expect an improvement in the profit margins of the business. Therefore, a target price of HK$25.10, corresponding to a P/E and P/B of 7.90x and 1.07x, has been assigned, with an `Accumulate rating assigned. (Closing price as at 20 Jun 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()