-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CNOOC (0883.HK ) - Maintain `Accumulate` Rating

Friday, March 8, 2013  11901

11901

CNOOC(883)

| Recommendation | Accumulate |

| Price on Recommendation Date | $14.660 |

| Target Price | $16.700 |

Weekly Special - 3306 JNBY Design Limited

Company profile

CNOOC is China's largest offshore oil and natural gas producer, and also one of the global largest independent oil and gas explorers and producers. Its main business covers exploration, development, production and sales of oil and natural gas.

Investment Summary

CNOOC announced it has completed its acquisition of Nexen Inc. (“Nexen”) on 26 February 2013. The company will gain the benefits from the U.K. North Sea, the Gulf of Mexico, and offshore West Africa, control the oil sands project with rich oil and gas resources in Long Lake, Alberta, and own the production properties in the Middle East and Canada. The Company's output and proved reserves would go up 20% and 30% respectively after this acquisition in expectation, and cause its reserve-production ratio to increase from 9.6 to 10.3 years.

Recently, ConocoPhillips got the approve document for the report of overall development and environmental impacts in Penglai 19-3 oil field. State Oceanic Administration (SOA) approved ConocoPhillips China (COPC) to resume production step by step, which is a very good news for the Company to bring the profitability to return to rising channel.

We still expect the international oil price would go up in the long term. The end of European debt crisis, increasing tense situation in the Middle East, and consistent depreciation of US dollar under quantitative easing (QE) would increase oil price. Different from Sinopec and PetroChina, the Company focuses on the exploration in upstream businesses benefiting from the increase of crude oil price, and does not take the risks from downstream businesses.

Currently China's explored area has less than 10% of total sea area. There is a bright future of offshore oil and gas exploration in the long turn. The Company owns absolute advantages in offshore oil and gas businesses compared to the peers due to the long-term focus on offshore oil and gas exploration and exploitation.

We still hold quite optimistic view on the Company's future performance, and the profitability would be improved step by step after the completed acquisition of Nexen, resumption of production in Penglai oil field and several early projects go in to production one after another. However, the performance of CNOOC is difficult to reach the target last year due to many bad factors, and the price therefore is hard to increase sharply in the short run. Overall, we cut the Company's 6-month target price to HK$16.70, maintain Accumulate rating.

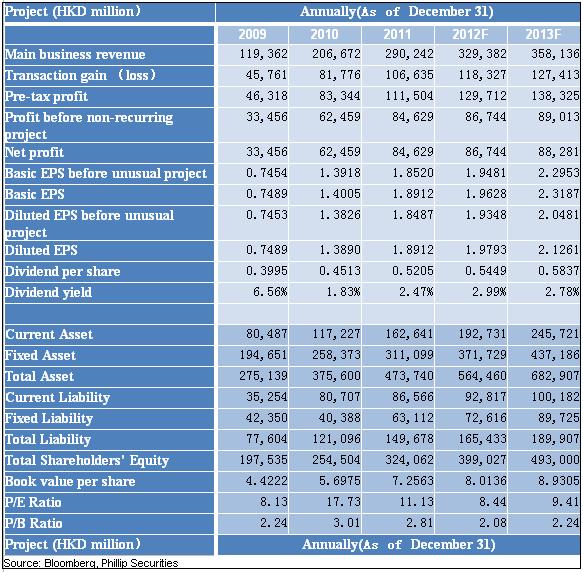

Financial Statement and Predictions

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()