-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Huaneng Power Int`l Inc (902.HK) - Attractive valuation

Monday, February 6, 2017  24952

24952

Huaneng Power Int`l Inc(902)

| Recommendation | Accumulate |

| Price on Recommendation Date | $5.020 |

| Target Price | $5.720 |

Weekly Special - 603179.CH Xinquan

Investment Summary

- We estimated a weak 2016 result with decline in net profit, however we believe the valuation is appealing.

- China electric power demand possibly bottomed, perhaps if the electricity consumption continue to grow steadily, would improve the firm's long-term earning power.

- China Coal price surge possibly ended, beneficial to the control of electricity generation costs.

Company Overview

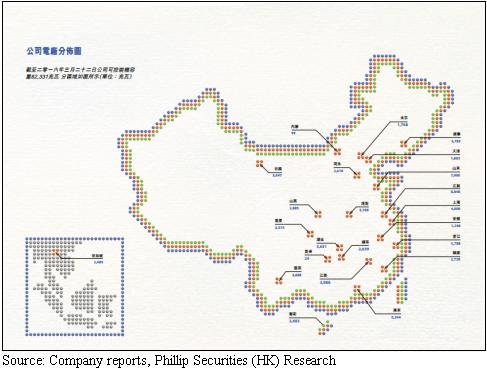

Huaneng Power International Inc. and its subsidiaries mainly engaged in developing, constructing, operating and managing large-scale power plants throughout China. As of 30 June 2016, the Company is one of China's largest listed power producers with controlling generation capacity of 82,571 MW and an equity-based generation capacity of 75,403 MW.

Below is a diagram to show the distribution of power plants of the company:

According to the firm's 1H2016 interim results, the Company and its subsidiaries recorded consolidated operating revenue of RMB52.924 billion, representing a YoY decrease of 18.96%. The net profit attributable to equity holders of the Company was RMB6.177 billion, representing a YoY decrease of 30.99%.

Along with overall unfavorable business environment of the power generation industry, the firm experienced tough times in last year. The most obvious problem is that, the price surge of the thermal coal resulted a significant impact on the cost of power generation. Moreover, the Excess Capacity of the power generation industry is another crucial problem. China's industrial power use growth has slowed in resulting the decrease in the power generation.

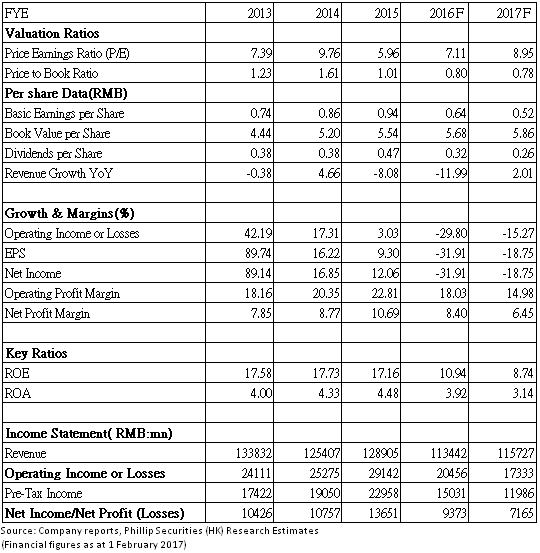

The group announced that the company's total power generation by the power plants within China on consolidated basis amounted to 313.690 billion kWh, down 2.13% YoY in 2016, and the total electricity sold by the company amounted to 295.800 billion kWh, down 2.05% YoY. In 2016, the group's average on-grid electricity settlement price for its power plants within China amounted to RMB396.60 per MWh, down 10.53% YoY. As a result, it is has been estimated that our 2016E EPS is RMB 0.64 per share in 2016, a decline of 32% YoY.

However, the stock is trading at approximate 7x FY2016E PE and 0.78x Price to Book Ratio, we believe most unfavorable information basically priced in on the stock price. In 2016, the stock had underperformed by around 35%, compared with the Hang Seng Index, which the valuation might already become appealing.

In addition, as the firm is the one of the largest power generator in China. It is hard to ignore that the group is a monopoly company, and also since the national standards for energy saving environmental protection is pushed higher and the environmental protection restrictions for energy development is much more tightened, the barriers to entry has become higher and higher for new entrants. Thereby, the group still has favorable long-term prospects.

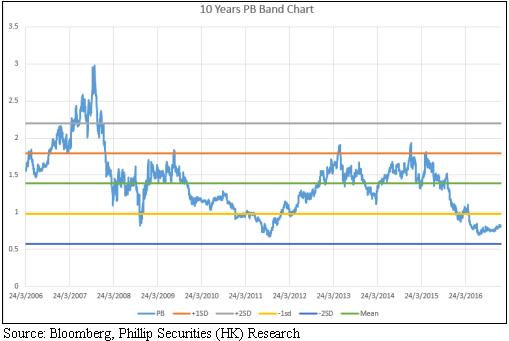

The Valuation is attractive

By simply look at the PB ratio, aims to examine the attractiveness of the valuation, at least in the book value point of view.

The Chart in below shows 10 years of PB ratio of Huaneng Power, the statistic started on 27/3/2016, with 2 standard deviation banh.

From the chart above, we can see that the valuation is actually appealing. Approximately, the average 10 years PB ratio is 1.385, one standard deviation below is 0.978, and the stock trades well below 0.978x PB.

These were two periods that the firm's Price to Book Ratio similar to now, the first period is during the 2008 financial crisis and the 2011 European debt crisis.

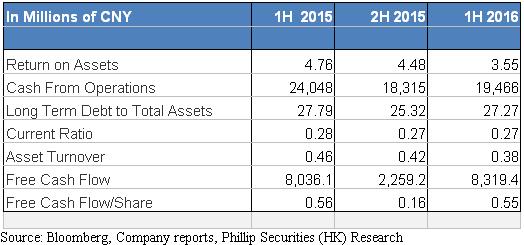

Although the valuation looks appealing by just looking at the PB ratio, the recent profitability, liquidity and operation efficiency are also the important factors. We have collected some key figures in the table below:

According to the 2016 interim result, the group still has an abundant operating cash inflow of RMB 19,466 million, which surprisingly increased by 6.28% compared with the previous 6 months. Although the long term debt to total assets ratios rose to 27.27, the current ratio stayed the same. As the first half of 2016, the group still has free cash flow per share of 0.55 RMB, almost identical to the same period in 2015, indicated the free cash flow is possibly still abundant.

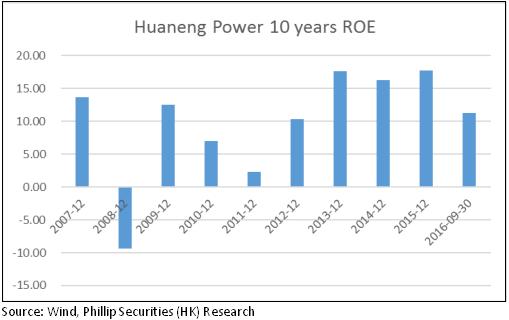

The Return on Equity ratio is also crucial, which can provide more information regarding the profitability of the group.

According to the data collected from Wind, the ROE for last 3 seasons is 11.25% indicating that the profitability is acceptable for the period, and the stock trades at around 0.78x PB ratio currently. The firm's profitability was unfavorable in two periods. The first period was 2008 during the Financial Crisis, the firm's ROE was -9.4%, and the stock traded at lowest PB of 0.82. The second period was 2011 during the European debt crisis, the firm's ROE was only 2.26%, and the stock traded at the lowest PB of 0.67. This could indicated that most of the unfavorable information are already reflected in the stock price, and the group possibly undervalued in recent times due to market overreaction.

Moreover, to see whether Huaneng Power is undervalued, we used a simple Discounted Dividend Model for evaluating the intrinsic value. The annual market return of HSI that we use for the calculation is 7.16%, which is the data collected from 31th Dec 1995 to 31th DEC 2016. We used the 10 years China government bond yield of 3.27% as the risk free rate, and the historical Beta of the stock is 0.729. From that, we calculated that the required return of the stock is 6.11%. Our forecasted dividend per share for next year is 0.26 RMB per share. Basic on the 10 years average ROE figure and we assumed the dividend payout ratio will stays the same as 50%, we speculated the dividend growth rate is 2.47% under normal situation and 1% for the worst situation. As a result, we calculated the intrinsic value of RMB 7.14 per share for the normal situation, and it is surprisingly close to the A share price of the group in the China A market. Under the worst situation, the intrinsic value is still RMB of 5.09 per Share. Therefore, the H share of the Group is trading at below intrinsic value. Basic on our estimated intrinsic value of the firm and the current PB ratio, it is reasonable to believe that the stock is undervalued.

China electric power demand possibly bottomed

According to the China National Energy Administration, the total power consumption grew 5% YoY to 5.9 trillion kilowatt hours in 2016. Electricity consumed by the service sector surged 11.2% last year, in line with 5.3% growth and 2.9% increase in the agricultural and industrial sectors in the period. From the whole year data, the main cause of the Excess Capacity of the power generation industry is slowed growth in the industrial electricity use. As its economy also slows, China possibly switch to less energy-intensive industries in order to be more resource-efficient.

However, according to the China Electricity Council, in November 2016, the total industrial electricity Consumption grew 5.9% to 370.5 billion kilowatt hours, accounting for 73.1% of the total power consumption.

The light industrial electricity consumption grew 7.2% to 62.1 billion kilowatt hours, accounting for 12.2% of the total power consumption. The heavy industrial electricity consumption grew 5.7% to 308.4 billion kilowatt hours, accounting for 60.8% of the total power consumption. Moreover, the group recently announced a better quarterly operation figure. For the fourth quarter of 2016, the company's total power generation by the power plants within China on consolidated basis amounted to 81.097 billion kWh, up 2.02% yearly, and the total electricity sold by the company amounted to 76.064 billion kWh, up 1.57% yearly. All these figures indicated that China electric power demand possibly bottomed, perhaps if the electricity consumption continue to grow steadily, would also improve the firm's long-term power of earning.

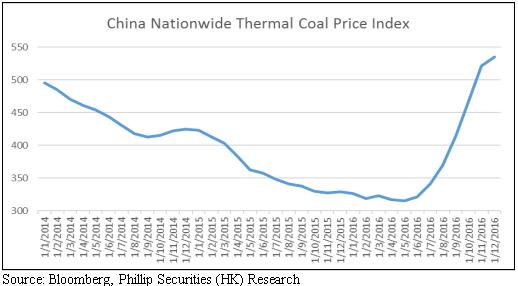

China Coal Price surged significantly, correction expected

Since the China government has been implemented a successful coal supply-side structural reform, including the strictly production limitation and reduction policy in major coal producing areas, as well as intensified the inspection on illegal coal mines and closure and suspension of mines. The China Nationwide Thermal Coal Price Index, the coal price rose to 534.92 per tonne in the last month of 2016, roughly more than 60% increase since the start of the year, according to the data from Bloomberg. The surged coal price had a significant impact on the power of earning of the coal-fired power generation companies, no exception for Huaneng power international.

However, the significant price increases disrupted the coal industry's capacity reduction and hurt the business of downstream industries, could cause the serious excess capacity problem reappeared in the coal industry. On the demand side, the end of the winter heating season will also reduce the demand for Coal. As a result, the coal price surge would possibly ended in recent time, and at least a price correction is expected, it is beneficial to the firm's fuel cost reduction. Moreover, according to the company, they have fully analysed the market, reinforced and deepened its cooperation with large-sale coal companies, highlighted the bids and price comparison for open-market coal, and at the same time improved coal importation. As a result, along with the correction of the coal price, we believe the group has the ability to effectively controlling the electricity generation cost.

Valuation

Taking all the points mentioned above into consideration, Huaneng Power International Inc's target price is therefore $5.72, with Accumulate rating assigned, represents 0.89x FY16 P/B and 0.86x FY17 P/B. (Closing price as at 1 FEB 2017)

Risks

Risks relating to the power demand in China, the overall power demand could keep declining if the economic growth slows down.

Risks relating to coal market, the fluctuation on the coal price will bring certain degree of risks to the fuel cost control

Risks relating to electricity tariff, it could cause uncertainty on the electricity pricing.

Risks relating to environmental protection policies, the national standards for energy saving environmental protection could pushed higher and the environmental protection restrictions for energy development is possibly more tightened.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()