-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CR PHARMA(3320.HK) - Distribution Business of 1H2019 Keeps Stable

Wednesday, October 2, 2019  7914

7914

CR PHARMA(3320)

Weekly Special - 3306 JNBY Design Limited

Company Update

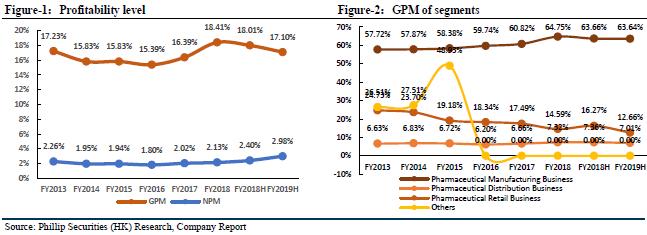

For the six months ended June 30, 2019, the company recorded revenue of HKD 101.923 billion (1H2018: HKD 93.741 billion), representing an increase of 8.78% YoY (up 15.7% YoY in terms of RMB), the revenue of pharmaceutical manufacturing, distribution and retail segments accounted for 15.5%, 81.5% and 2.9%, respectively, which was slightly lower than our expectations, it is mainly due to the slower growth of the pharmaceutical manufacturing business by Dong-E-E-Jiao. The company achieved gross profit of HKD 17.434 billion (1H2018: HKD 16.881 billion), showing an increase of 3.3% YoY (up 9.9% YoY in terms of RMB). The gross profit margin was 17.1% (1H2018: 18%), decreasing 0.9 ppts YoY, mainly because the distribution business grew faster than the pharmaceutical manufacturing business. The net profit attributable to shareholders was HKD 3.035 billion (1H2018: HKD 2.25 billion), a YoY increase of 34.9% (up 43.6% YoY in terms of RMB), mainly due to the investment income of Shenzhen Sanjiu.

Optimize Business Structure and Promote Terminal Coverage

The company`s pharmaceutical distribution business achieved revenue of HKD 84.949 billion, a YoY increase of 9.5% (up 16.5% YoY in terms of RMB). The gross profit margin was 7.0%, a slight decrease of 0.4 ppts compared with 1H2018. The coverage of terminals has increased year by year. The total number of downstream customers of 1H2019 has exceeded 100,000, of which 6,862 are high-end hospitals, increasing 17.2% YoY. The proportion of emerging businesses continued to increase. The growth rates of equipment, importing and Chinese medicine decoction pieces businesses were more than 50%, 30% and 30% in 1H2019, respectively, and third-party logistics revenue increased by more than 80% (in terms of RMB). The company`s direct sales to medical institutions increased by 23% YoY, and the proportion has increased to 77.5%, the business structure has been further optimized. In addition, in July 2019, CR Pharmaceutical Commercial completed the subscription and increased its holding of Zhejiang Int`l, accounting for 20% of the total share of Zhejiang Int`l, which will help enhance the company`s comprehensive competitiveness in the Eastern China.

Leader of OTC Industry, DTP Business Grows Rapidly

Affected by the revenue decline of Dong-E-E-Jiao and consolidation of Jiangzhong Pharmaceutical, the company`s pharmaceutical manufacturing business achieved revenue of HKD 17.367 billion, a YoY increase of 2.9% (up 9.5% in terms of RMB). The gross profit margin was 63.6%, a slight decrease of 0.1 ppts compared with 1H2018. After the acquisition of Jiangzhong Pharmaceutical, the leading position of the company in the CHC area has been further strengthened. In 2018, four products made by the company was included in the top ten OTC market sales products in China. In addition, as of 1H2019, the company focused on more than 40 consistent evaluation projects, and five products passed the consistency evaluation. In 1H2019, R&D expenditure was HKD 660 million, an increase of 7.9% YoY (in terms of RMB). The revenue of retail business was HKD 2.946 billion, an increase of 19.2% YoY (increased 26.9% in terms of RMB). Gross profit margin was 12.7%, down 3.6 ppts from 1H2018, mainly due to the rapid growth of DTP with relatively low gross profit margin. In addition, the company acquired a 25% shares in the Tycoon Group in 1Q 2019, which will further enrich and optimize the existing retail product portfolio and strengthen the competitive advantage of the distribution and retail business in Hong Kong market.

Maintain "BUY" Rating

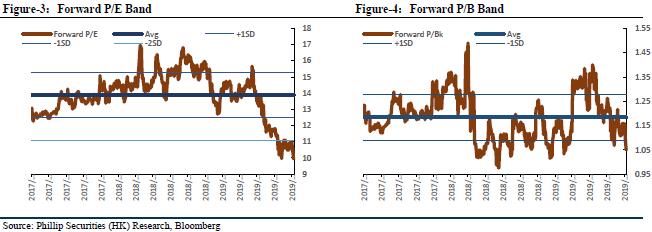

We adjusted our forecast for FY19/FY20/FY21 incomes to HKD 206.6/225.6/246.5 billion, showing increases of 8.92%/9.21%/9.23% YoY; net profit attributable to shareholders were HKD 4.7/5.2/6.2 billion, with increase of 16.84%/10.69%/18.70% YoY; the corresponding EPS was HKD 0.75/0.83/0.90. The target price was adjusted to HKD 11.22, corresponding to FY19/FY20/FY21 14.95x/13.51x/12.48x PE, which was +52.27% higher than the current price (HKD 7.37 as of September 27, 2019), maintaining a “BUY” rating.

Risk

1. Industry policy risk;

2. M&A fails expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()