-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

NetEase (9999.HK) - Top game developer in the world, High growth potential in Youdao K-12 sector

Monday, November 16, 2020  9682

9682

NetEase(9999)

| Recommendation | Buy |

| Price on Recommendation Date | $139.400 |

| Target Price | $172.800 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

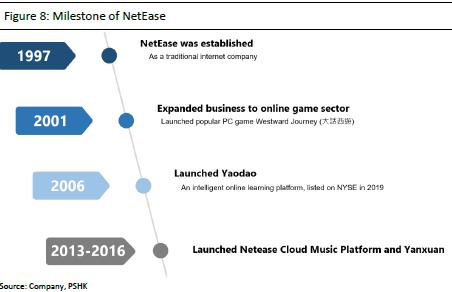

NetEase is a leading Internet company in China

NetEase is a leading internet company in China. It was established in 1997 and started as a typical Chinese internet company providing traditional internet services, such as media and email services. Since 2001, the company has expanded its business to the online game sector. According to App Annie data, the company is now the world's second largest mobile game company based on the user expenditures of iOS and Google Play in 2019. In 2006, the company launched an intelligent learning platform Youdao, which was spun-off and listed on the New York Stock Exchange in 2019. In 2013, the company launched a music streaming platform NetEase Cloud Music Platform. In 2016, the company launched its e-commerce platform Yanxuan. The company's business can be divided into three major sectors, online games, Youdao, and other innovative businesses such as NetEase Cloud Music and Yanxuan. The company was listed on the Nasdaq Stock Exchange in 2000, and on the Hong Kong Stock Exchange in 2020.

The differences in targeting game genres between NetEase and Tencent

The company's focus of game genre is significantly different to Tencent. Tencent's main games Honor of Kings (王者榮耀) and Game for Peace (和平精英) are both moderate games with social characteristics in them. These games are user friendly to new joiners and suitable for both men and women in nature. Therefore, these games have a very high MAU. In addition, these games are backed by the 2 largest social media platform in China, Wechat and QQ. Hence, these 2 games basically monopolize the light-moderate mobile game markets in China, with very few similar games on the market. On the contrary, NetEase has been deeply focused in R&D of core game genres such as MMORPG genres since its inception. However, due to the high average game time and high spending nature of core games, which in game performance and rankings are hugely affected by the game time and money spent by users, the MAU of core games are significantly lower. But at the same time, core games have characteristics of higher ARPU and longer life cycles. Taking into account Tencent's absolute innate advantages in light and moderate games, the company avoids direct competition with Tencent and focuses on core games is a wise choice.

The K-12 online courses of Youdao is experiencing huge growth

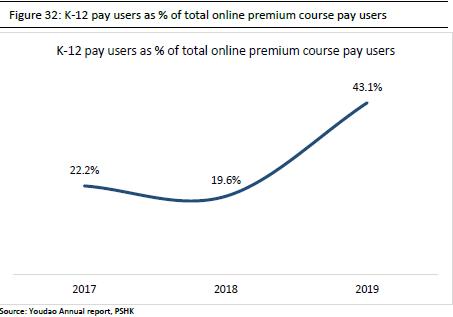

In 2018, the company began to focus on K-12 business and launched several products for K-12 students, including Youdao Mathematics and other learning tool products that use AI technology. The company also provides a series of K-12 online premium courses (including K-12 online after-school tuition classes and K-12 online programming classes). In terms of the K-12 business model, Youdao still insists on learning products (including APP and other tools) as the main channel for traffics, while online courses are the company's main channel for monetization. Youdao's number of K-12 pay users in 2019 was 359 thousand, accounting for 43% of the total number of pay users for its premium courses. This proportion increased by about 24% yoy comparing to 2018. It can be seen that the company's K- 12 business layout has a significant effect, prompting it to fully capture the high demand and growth potential of China K-12 online education.

Valuation

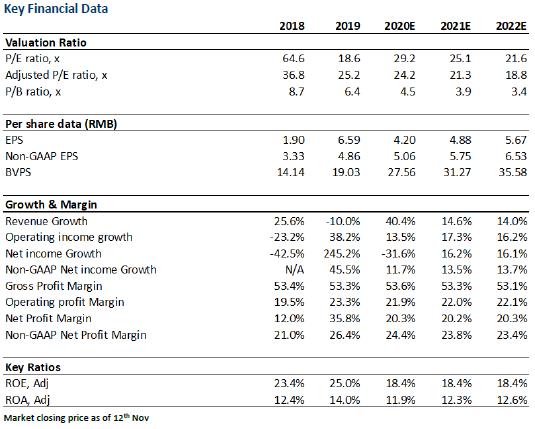

We forecast the company's 2020/2021/2022 Non-GAAP EPS to be RMB 5.06/5.75/6.53. We have adopted SOTP to value the company. we value NetEase at HKD 596.9 billion, with target price at HKD 172.8, with respective 2020/2021/2022 Non-GAAP PE at 29.85x/26.31x/23.14x. We initiate with a BUY rating.

Industry Review and Forecast

The market for PRC Mobile Games Overseas

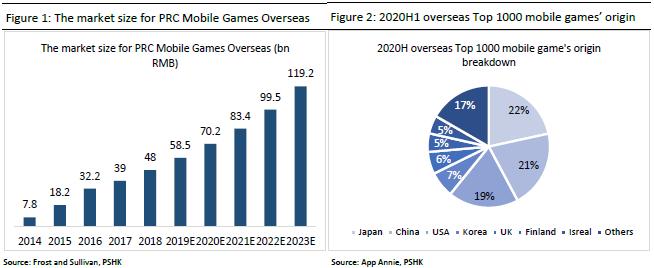

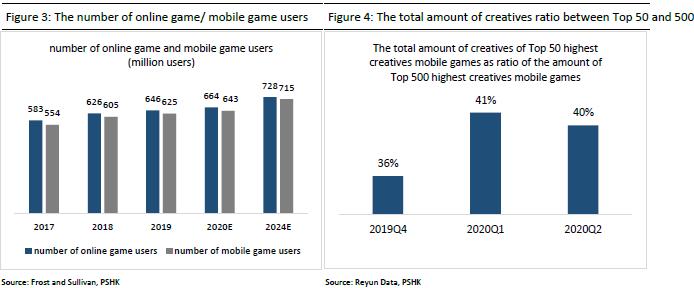

In recent years, many mobile game companies have been focusing on their overseas market business, mainly because the mobile game markets in many overseas regions (especially Southeast Asia) are still in the early stage of development and has great growth potential. In contrast, the Chinese mobile game market is already in the mature stage and its growth has significantly slowed down. Secondly, the Chinese game market is indeed hugely affected by policies. Relevant national departments issued a number of game supervision measures (including tightening supervision on underage gamers and restricted their game time) in 2018-2019, and suspended the pre-approval for games in 2018. Although the current pre-approval procedure has resumed, nonetheless there are still significant policy risks in China's mobile game market. On the contrary, games in majority of overseas markets are only supervised through the "game classification system", where games are classified by the age of suitable players. It can be seen that the regulatory intensity of the overseas game market is obviously lower than that of the Chinese market. As a result, expanding overseas markets will help Chinese mobile game industry participants to reduce this policy risk. According to Frost & Sullivan, the China's overseas mobile game market recorded a significant growth at a CAGR of 57.5% from 2014 to 2018, and is expected to grow at a CAGR of 20.0% from 2018 to 2023. The Chinese mobile games have already achieved good results in overseas market. According to the statistics of the Overseas Research Institute (海外研究院), in the US Google Play Store Top 100 free list and Top 100 best-selling list, apps from China have occupied 15 and 20 places respectively. Further, there are 30 Chinese mobile games in the Top 100 best-selling Korean mobile games in 2019. Further, according App Annie data, the market share of Chinese mobile games in overseas markets was up by 2.9ppt yoy in 1H20, and reached 21.2%, which is only slightly behind Japan with 21.5%.

The Chinese game advertisement market

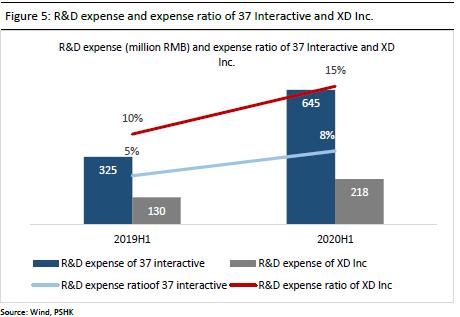

In recent years, the growth of users in the Chinese game market has gradually been slow. According to Frost & Sullivan, the CAGR of Chinese gamers/mobile game players from 2019 to 2024 is expected to be 2.4%/2.7%. In 1H20, even under the impact of COVID and quarantine, the growth of users remained slow. According to the “China Game Industry Report for January-June 2020” 《2020年度1-6月中國遊戲產業報告》, the number of gamers in China in 1H20 was 557 million, a yoy increase of only 1.97%. As the growth of number of Chinese gamers begins to slow down, the difficulty of acquiring customers for game companies has increased. On the other hand, according to Reyun data, the total amount of creatives of the Chinese TOP 50 highest creatives mobile games have accounted for roughly 41%/40% of the total amount of creatives of the Chinese TOP 500 highest creatives mobile game in 20Q1/20Q2, up by 5ppt/4ppt comparing to the 36% in 19Q4. The increase in this proportion means that the Chinese game advertisement market is gradually dominated by the market leaders. According to DataEye-ADX, the Game 《亂世王者》by Tencent ranked 13th on the ranking of highest creatives Chinese game. This is relatively surprising, since the games developed by Tencent don`t usually appear in the Chinese game advertisement markets, as they are usually promoted and advertised through the diversified advertisement channels of Tencent. This served as a clear evidence that the market leaders have begun to enter the Chinese game advertisement market. The combination of the increasing customer acquisition difficulties as well as the fact that the market leaders begin to enter the Chinese game advertisement market have driven the cost of game advertisement upward significantly.

Developing exquisite games by enhancing R&D capabilities is the general trend in the sector

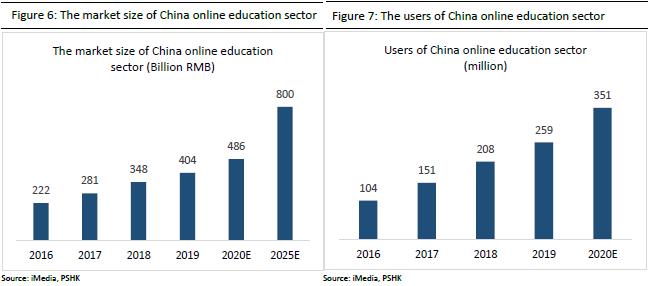

Game development capabilities and game quality have become particularly important especially in the background of high game advertisement cost. The increase in game advertisement cost will squeeze the living space of non-exquisite games on the one hand, and on the other hand, it has shifted the attention of mobile game developers onto the quality of games in order to acquire customers and retain them, rather than spending significant amount on advertisement. In addition, as players consume more and more rationally, whether mobile game companies can tap the value of its existing users by providing high-quality games will become the key. Further, pre-approval of games by Chinese Government are more stringent than ever. This has further pushed game companies to refine their games in order to increase the games` life cycle to cope with the increasingly stringent pre-approvals. The above reasons have promoted high quality and refinement of the mobile game industry and we believe that that increasing their R&D capabilities will be the only way for mobile game companies to survive. Take 37 Interactive Entertainment (A-shares) and XD Inc (HK-listed) as example, the R&D expense of 37 interactive and XD in 1H20 were RMB 645/218 million, up by 99%/68%. The corresponding R&D expense ratio were also up by 2.7ppt/5.5ppt.

The epidemic has popularized online education in China

China's online education market has maintained steady growth in the past. According to iMedia, the size of China's online education market has increased from RMB 221.8 billion in 2016 to RMB 404.1 billion in 2019, with a CAGR of 22.1% during the period. Affected by the epidemic, the growth of China's online education market will accelerate, and it is expected that the market size will reach RMB 485.8 billion in 2020, with a yoy increase of 20.2%. Further, the industry is expected to benefit from the upgrading of technologies such as artificial intelligence and big data in the future, and its market size is expected to grow steadily. It is expected to reach approximately RMB 800 billion in 2025. In addition, affected by the epidemic and the policy of “suspending school without suspending learning”, traditional colleges and universities have also adopted online education for teaching in China. This has greatly increased the scale of online education users and the penetration rate of online education, especially for K-12 teaching. According to iMedia, the number of online education users in China is expected to reach 351 million in 2020, with an increase of 36% yoy.

The K-12 online education market has the highest growth potential

At present, the online education market can be divided into 5 major segments, namely early childhood education, K-12 education, higher education, quality education and vocational training. According to iMedia, compared with other segments, the Chinese K-12 online education market is in greater demand with high online penetration rate. The main reasons are 1) The society now pays more attention to children's education 2) the increase in disposable income of Chinese families is noticeable 3) the increase in K-12 students` familiarity with the internet and 4) the pressure to enter primary and secondary schools in China has gradually increased. On the other hand, according to data from the Chinese Academy of Sciences (中國科學院), affected by the epidemic and the policy of “suspending school without suspending learning”, the penetration rate of K-12 online education in China reached its peak level in March 2020, about 85%. With the pandemic gradually being controlled and the resumption of Chinese K-12 schools, the penetration rate will drop significantly, but most K-12 students have developed their habits of using online education platforms during the epidemic. Hence, the online penetration of K-12 is expected to maintain high level even after the pandemic. According to data from the Chinese Academy of Sciences (中國科學院), the K-12 online penetration rate is expected to reach 35% in 2020, and it is expected to reach 55% in 2022. Further, the market share of Chinese K-12 online education is currently mainly concentrated in Tier 1-2 cities, with total market share of tier 3,4 and 5 cities being 23% (according to the Chinese Academy of Sciences), but as the education consumption power and awareness of online education of tier 3,4 and 5 cities gradually improved, the K-12 online education market in tier 3,4 and 5 cities is expected to realize a huge growth. Based on the above reasons, we believe that the K-12 online education market has great potential for future growth.

Company Overview and its Competitive Advantages

NetEase is a leading internet company in China

NetEase is a leading internet company in China. It was established in 1997 and started as a typical Chinese internet company providing traditional internet services, such as media and email services. Since 2001, the company has expanded its business to the online game sector. According to App Annie data, the company is now the world's second largest mobile game company based on the user expenditures of iOS and Google Play in 2019. In 2006, the company launched an intelligent learning platform Youdao, which was spun-off and listed on the New York Stock Exchange in 2019. In 2013, the company launched a music streaming platform NetEase Cloud Music Platform. In 2016, the company launched its e-commerce platform Yanxuan. The company's business can be divided into three major sectors, online games, Youdao, and other innovative businesses such as NetEase Cloud Music and Yanxuan. The company was listed on the Nasdaq Stock Exchange in 2000, and on the Hong Kong Stock Exchange in 2020.

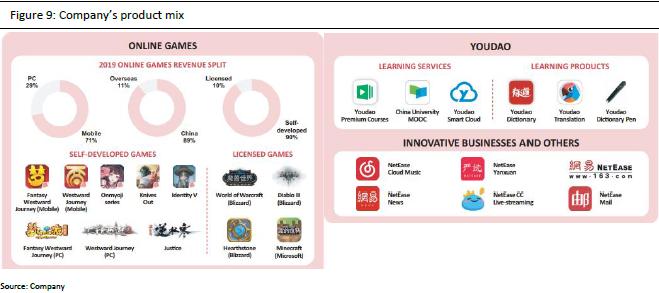

NetEase Online Game business

The company is the world's second largest mobile game company

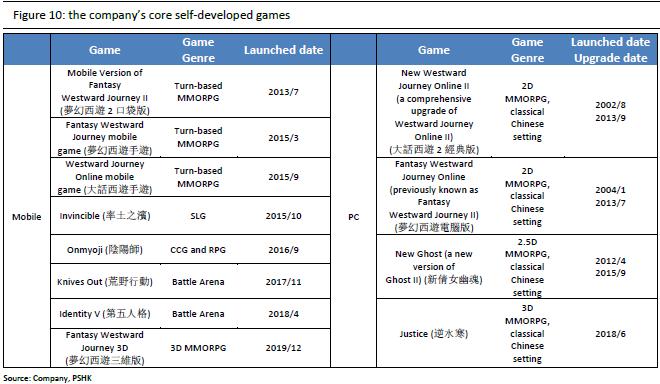

The company started its game business in 2001 and focused on the R&D of PC games. In December 2001, it launched its first MMORPG PC game Westward Journey (大話西遊), and launched Westward Journey 2 (大話西遊2) in August 2002. In January 2004, it launched its second original MMORPG PC game Fantasy Westward Journey (夢幻西遊). Westward Journey and Fantasy Westward Journey were upgraded to New Westward Journey Online II (大話西遊2經典版) and (夢幻西遊電腦版) in 2013. Up to now, these two games are still loved by players and still contribute significant revenue for the company. In 2013, in order to capture the high growth of the mobile game market, the company began to expand its game business to mobile game sector, and launched its first mobile game Mobile Version of Fantasy Westward Journey II (夢幻西遊2口袋版). The current business model of the company's game business is “mobile games as the mainstay, with PC games as a supplement”. In 2019, the company's revenue of mobile games accounted for 71% of total game revenue. As of the end of 2019, the company has released more than 100 mobile games (self-developed + licensed games), with a variety of game genres, including MMORPG, CCG (collectible card game), first-person shooter games, Battle Arena, SLG games, etc. Among all games, the self-developed and “PC to mobile” games Fantasy Westward Journey mobile game (夢幻西遊手遊) and Westward Journey Online mobile game (大話西遊手遊) are most populated. Lastly, the revenue from licensed games only accounted a small portion of the company's total game revenue, 10.8%/9.5%/9.6% respectively in 2017/2018/2019.

The company's major self-developed games all have high gross billings after being launched. According to App Annie, the company has 4 games that ranked top 10 in China in terms of IOS revenue generated in September 2020. These 4 games are Fantasy Westward Journey mobile game (夢幻西遊手遊), Westward Journey Online mobile game (大話西遊手遊), Invincible (率土之濱) and Onmyoji (陰陽師).

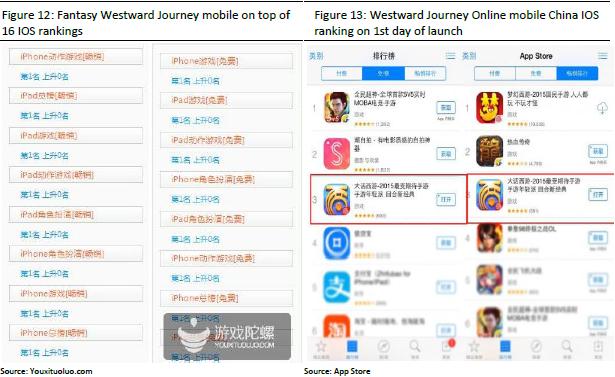

Fantasy Westward Journey mobile (夢幻西遊) is the company's first "phenomenon-level" mobile game. It was launched on March 15, 2015. It reached the top of the IOS free ranking within 2 hours of its launch, and reached the top of the IOS best-selling ranking after 11 hours of launch. Since March 28, it has ranked 1st on 16 IOS ranking, including iPhone action game bestselling ranking, iPad total bestselling ranking, iPad game bestselling ranking and etc. Since then, it has dominated the IOS bestselling ranking for a long time. Up to now, the game has remained stable in the China Top 10 IOS game bestselling ranking.

Westward Journey Online mobile (大話西遊手遊) is the company's second "phenomenal" mobile game. It is a turn-based MMORPG mobile game based on the PC game New Westward Journey Online II (大話西遊PC). It was launched on September 10, 2015. Less than a day after it was launched, it ranked third on the China IOS bestselling ranking and free ranking. Up to now, the game has maintained on the Top 20 best-selling IOS game ranking in China.

Invincible (率土之濱) is a SLG game with the theme of the Three Kingdoms. It was launched in October 2015. At that time, the China SLG market was not as popular as now. The company can be regarded as one of the first game company to open up the China SLG market. The initial ranking of the game was not as high as other hit games. The game only made it onto the Top 40 best-selling IOS games ranking two months after it was launched. However, the game has fully demonstrated the characteristics of long life cycle and stable gross billing of SLG games, with a very stable and eye catching performance even 5 years after it was launched. Its China IOS bestselling ranking went from Top 50 in the 1st year to Top 35 in the 2nd year, and to Top 25 in the 3rd year. Up to now, it is stable at Top 20 and sometimes even break into the Top 10s.

Onmyoji (陰陽師) is an RPG+CCG mobile game. It was launched on the IOS platform on September 2, 2016. On September 9 of the same year, it was launched on all platforms. It topped the IOS best-selling ranking shortly after its launched, and in October it even dominated the list for two weeks.

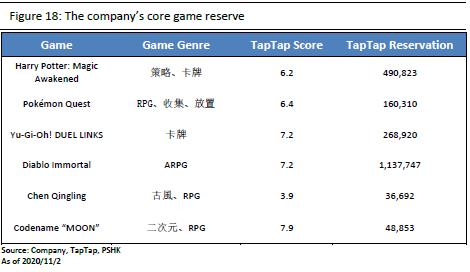

The company's game reserve

According to the company's official website, the company currently has dozens of games in reserve, with a diverse game genres and playstyles. The game reserve includes mobile games derived from famous IPs such as "Harry Potter", "POKEMON", “Yu-Gi-Oh”.

The company is an obvious leader in developing MMORPG games

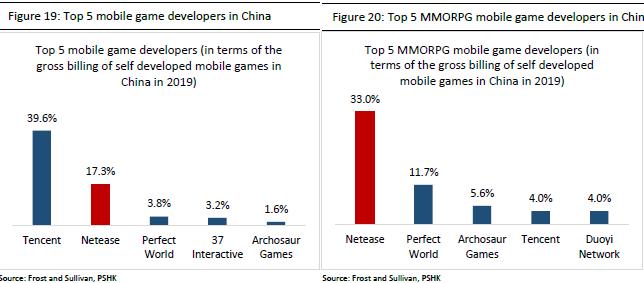

Majority of the company's core games are MMORPG games, such as Westward Journey Online mobile (大話西遊手遊) and Fantasy Westward Journey mobile (夢幻西遊). According to Frost and Sullivan, the company is the 2nd largest Chinese mobile game developer in China in terms of total gross billings from self-developed games in mainland China in 2019, with market share of 17.3%. However, in terms of the total gross billings from self-developed MMORPGs in mainland China in 2019, the company actually ranks 1st in the country, with market share of 33.0%. According to Frost and Sullivan, MMORPG games has the highest market share in China among all other game genres and also has the highest growth potential in the future. The expected CAGR from 2019-2024 is 19.7%, way higher than the 11.7% CAGR of the average in the mobile game industry in the same period. Further, MMORPG games also has higher-than-average life cycles, highest ARPU and highest Pay user conversion rate comparing to other mobile game genres. The company is expected to become the main beneficiaries of the high future growth in MMORPG mobile game sector because of the company's forward looking and deep cultivation in the field of MMORPG games.

The company's focus of game genre is significantly different to Tencent. Tencent's main games Honor of Kings (王者榮耀) and Game for Peace (和平精英) are both moderate games with social characteristics in them. These games are user friendly to new joiners and suitable for both men and women in nature. Therefore, these games have a very high MAU. In addition, these games are backed by the 2 largest social media platform in China, Wechat and QQ. Hence, these 2 games basically monopolize the light-moderate mobile game markets in China, with very few similar games on the market. On the contrary, NetEase has been deeply focused in R&D of core game genres such as MMORPG genres since its inception. However, due to the high average game time and high spending nature of core games, which in game performance and rankings are hugely affected by the game time and money spent by users, the MAU of core games are significantly lower. But at the same time, core games have characteristics of higher ARPU and longer life cycles. Taking into account Tencent's absolute innate advantages in light and moderate games, the company avoids direct competition with Tencent and focuses on core games is a wise choice.

The strong game R&D and operation capabilities

As of December 31, 2019, the company had more than 10,000 in-house programmers, network engineers and graphic designers dedicated to its R&D activities, accounting for approximately half of its total employee headcount. Further, the company has two proprietary game engines, NeoX and Messiah. The company's proprietary game engines bring greater flexibility and autonomy to its R&D team, allowing the company to successfully complete the "PC to mobile" transformation. The company's self-developed game revenue accounted for the vast majority of its total game revenue. In 2019, the self-developed game revenue accounted for approximately 90% of total game revenue. The company's strong R&D capabilities have prompted the company to continuously develop hit-games. From Fantasy Westward Journey (夢幻西遊手遊) and Westward Journey Online (大話西遊手遊) in 2015 to Onmyoji (陰陽師) and Knives out (荒野行動) launched in 2016/2017. Furthermore, the company is currently co-developing Diablo ImmortalTM (暗黑破壞神:不朽) with Blizzard, an MMO action-RPG and a milestone in Blizzard's foray into mobile games with its iconic Diablo franchise. The company has also further enhanced its global R&D capabilities by launching a video game studio in Canada in 2019.

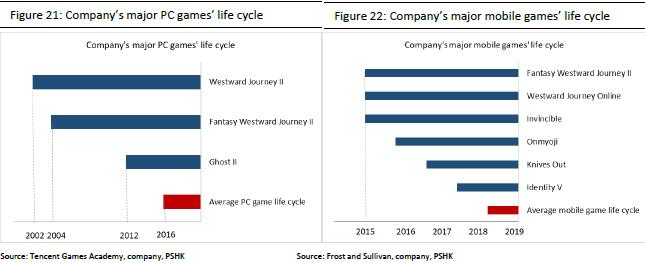

On the other hand, the company has always paid great attention to the product life cycle and scalability. According to Tencent Game Academy, the average life cycle of a PC game is 3-5 years, but the company's PC games Westward Journey (大話西遊) and Fantasy Westward Journey (夢幻西遊) were launched in 2002/2004 respectively. So far, these two games have been operating stably for 18/16 years, which is far higher than the average of a PC game. The long life cycles were mainly due to the company's constant operation and maintenance of the game. Both of these games had launched major upgrades in 2013, prompting gamers to maintain freshness to the game, hence reducing the decline in ARPU. As for mobile games, according to Frost & Sullivan, the average life cycle of Chinese mobile games is 3-12 months, but the company's core mobile games have all operated for 4-5 years, while still maintain stably on the China Top 10 mobile games ranking in terms of revenue generated.

The global influence of the company's games

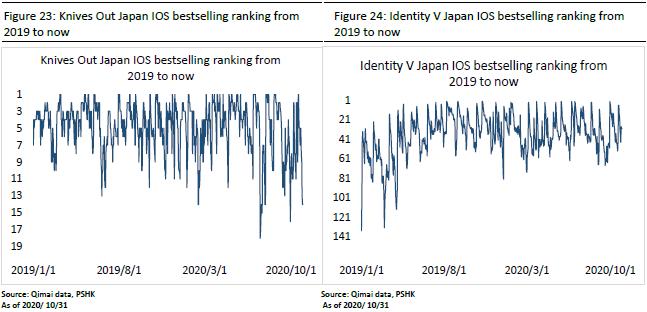

The company has been actively expanding globally in recent years. Since 2015, the company has launched more than 50 mobile games in overseas markets. With the huge influence of the company's IP and localized operations/purchases/marketing strategies, many games have achieved outstanding performance in overseas markets (including the Japanese market, which can be regarded as the most difficult market to enter). 1) Knives Out (荒野行動) was launched in the Japanese market in 2017, and it has been loved by Japanese players, and has repeatedly topped the IOS bestselling ranking in Japan. In 2020 (3 years after the game was launched), the game remained stable in the Top 20 of Japan's IOS best-selling ranking. 2) Identity V (第五人格) was launched in the Japanese market in 2018, and in September 2019 it topped the Japanese IOS bestselling ranking. 3) Marvel Super War (漫威超級戰爭), which was launched in various Southeast Asian markets at the end of 2019, also topped the iOS download ranking in various regions. At the end of 2019, the company's overseas game revenue accounted for 11% of total game revenue. We expect the company to launch more games in overseas regions in the future, including blockbuster games such as Diablo: Immortal (暗黑破壞神:不朽) developed in cooperation with Activision Blizzard and self-developed mobile game Harry Potter: Magic Awakens (哈利波特:魔幻覺醒) and etc. At present, the company's overseas game revenue accounts for a relatively low proportion, and there is a lot of room for growth in the future.

The company's diverse IP monetization channel

The company has a number of original IPs, including Western Journey (大話西遊), Fantasy Westward Journey (夢幻西遊), Onmyoji (陰陽師) and so on. The company has combined its original IP with games, animation, film and television, etc. to create a complete IP ecological chain, which helps the company to monetize its IPs in a very diverse channels. Taking Onmyoji as an example, the company has created 3 games based on the IP of Onmyoji (a Moba game, a CCG game and a SLG game), a movie, two musicals, multiple animes and even launched a café with the theme of Onmyoji. Different entertainment content based on the same IP can not only effectively realize multi-channel monetization for the IP, but also greatly increase the influence of the IP, thereby increasing the popularity of the company's IP games, which is the company's main business.

Youdao Business

The two segments of Youdao are learning services and product businesses and online marketing services

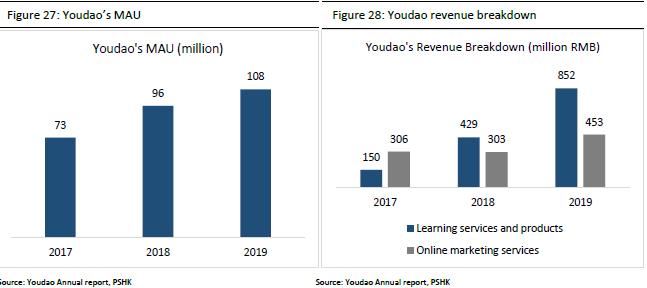

Youdao was established in 2006 and launched its flagship product Youdao Dictionary in 2007. Up to now, Youdao Dictionary is still one of the language apps with the most active users in China. Youdao Dictionary has attracted a huge user base for the company. With its strong brand, the company has subsequently launched other learning services, including online courses and interactive learning programs, to meet the lifelong learning needs of preschool, primary and secondary school, college students and adult users. In addition to providing learning services and products, Youdao also provides different forms of advertising services (online marketing services). Therefore, the company's two major sources of income are learning services and product businesses and online marketing services. The 2017/2018/2019 learning service and product business revenue accounted for 32%/59%/65% of the total revenue of Youdao, respectively. Youdao was listed on the Nasdaq Stock Exchange in October 2019. Youdao's global average MAU in 2019 was approximately 108 million people, and it has achieved success in China and many overseas markets.

Learning services and product businesses

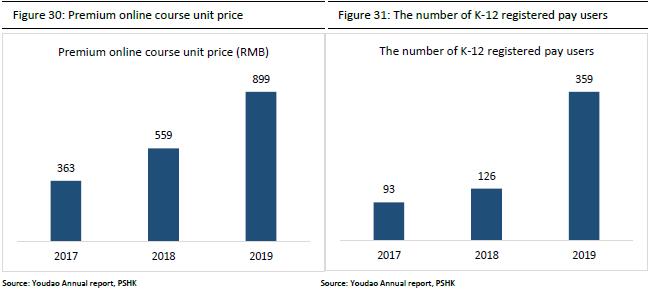

Youdao's learning services and product business mainly include online courses (such as Youdao premium courses, China University MOOC, etc.), sales of smart products (youdao dictionary pen) and APP paid value-added services (such as Youdao translation). Youdao learning service and product business revenue has grown rapidly in recent years, from RMB 150 million in 2017 to RMB 850 million in 2019, with a CAGR of 138% during the period. Among different products in this segment, the revenue of online courses accounted for the vast majority of the total income of learning services and products. The 2017/2018/2019 income of online courses were RMB 1.15/3.29/6.08 million, accounted for 77%/77%/71% of the total learning services and products` revenue. The revenue of Youdao Online Courses nearly doubled yoy in 2019, mainly due to 1) the strong yoy increase in K-12 pay users. In 2019, the number of pay users of K-12 online courses was approximately 359 thousand, representing a yoy increase of 185.2%. 2) The unit price of Youdao's online premium courses in 2019 rose by 61% yoy to 899 RMB.

In 2018, the company began to focus on K-12 business and launched several products for K-12 students, including Youdao Mathematics and other learning tool products that use AI technology. The company also provides a series of K-12 online premium courses (including K-12 online after-school tuition classes and K-12 online programming classes). In terms of the K-12 business model, Youdao still insists on learning products (including APP and other tools) as the main channel for traffics, while online courses are the company's main channel for monetization. Youdao's number of K-12 pay users in 2019 was 359 thousand, accounting for 43% of the total number of pay users for its premium courses. This proportion increased by about 24% yoy comparing to 2018. It can be seen that the company's K- 12 business layout has a significant effect, prompting it to fully capture the high demand and growth potential of China K-12 online education. In addition, Youdao has effectively increased its online presence and exposure in China's K-12 online education sector through cooperation with CCTV Video, Bilibili and other platforms during the epidemic period, which is expected to further accelerate the company's growth in K-12 online education market and enable it to occupy a certain market share.

The innovative education model of Youdao premium courses

Youdao Premium Courses is the education brand of Youdao's large class teaching. Courses include K-12 courses, foreign language courses, interest classes, etc. Up to now, Youdao's premium courses have covered all ages from children to university students. Youdao's premium courses have evolved from the previous live broadcast large-class teaching to the current “Dual-Teaching” model (雙師模式) (lectures by famous teachers and supervisor supervises students), which makes online teaching more efficient. At present, Youdao's premium course has a unique technology platform, including live/recorded broadcasting system, question bank, mock examination and other systems. Youdao even tried to use AI technology by adding AI elements to the current “Dual-teaching” model, and launched an innovative+interactive large class model. The interactive large class mode uses AI technology to add intelligent machine-assisted interaction in the curriculum to improve user experience and teaching effects.

Online marketing services

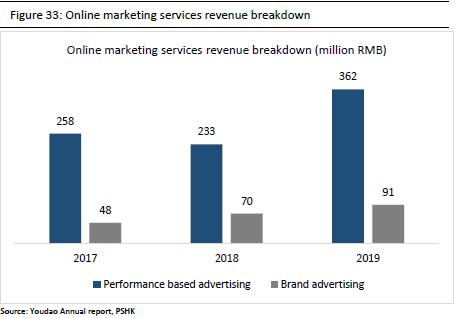

Youdao's online marketing services are mainly advertising services provided by Youdao's product matrix. Youdao's huge user traffic makes its advertising platform valuable for advertisment. The company provides a series of advertising formats, including banner ads, video ads, etc. The company mainly provides CPC (cost per click) performance-based advertising, which advertising costs are based on the number of user that clicks on the advertisement. Performance-based advertising accounts for the vast majority of total online market service revenue, accounting for 84.4%/76.9%/ 80.0% in 2017/2018/2019. The company has approximately 3,000/1,800/2,400 performance advertiser clients in 2017/2018/2019, respectively. In addition, the company also provides brand advertisement services that charge a fixed advertising fee. In order to further retain customers, the company also provides other free value-added services, such as advertising effect analysis and advertising management etc.

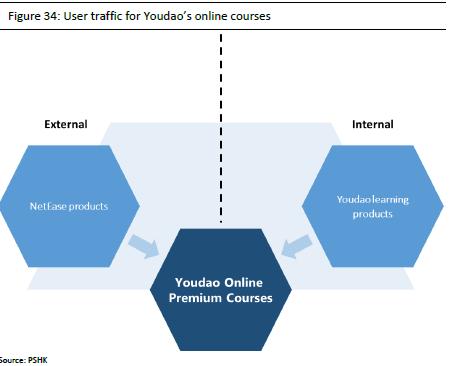

Netease's products are provide user traffic for Youdao, greatly reducing Youdao's customer acquisition costs

We believe that although Youdao has been listed independently in the US, Youdao is still one of the indispensable business segments of NetEase. NetEase's products have always provided Youdao with a large amount of traffic. The company's management has also stated that NetEase's products such as NetEase mailbox and NetEase Cloud Music are the main sources of Youdao's important customers. Coupled with the above-mentioned on learning products (including APP and other tools) provides user traffic for Youdao internally. It greatly reduces Youdao's customer acquisition costs and enhances its competitive advantage in the emerging market of online education.

Financial Analysis and Forecast

Revenue

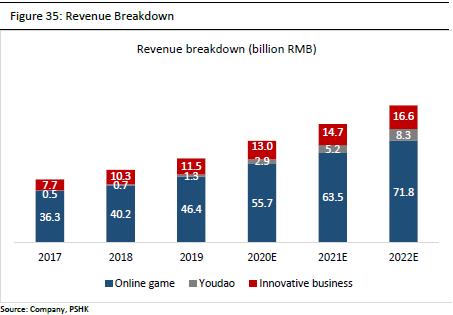

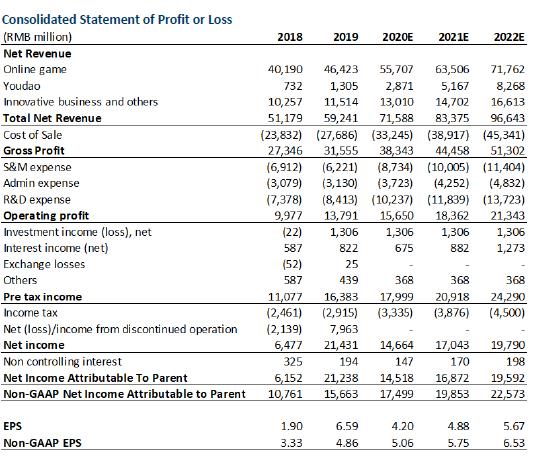

The company's revenue rose from RMB 44.4 billion in 2017 to RMB 59.2 billion in 2019, with a CAGR of 15.4% during the period. Within the total revenue, the online game business, which accounts for the highest revenue share, had a stable revenue growth, rising from RMB 36.3 billion in 2017 to RMB 46.4 billion in 2019, with a CAGR of 13.1% during the period. The main reason for the growth of the online game business was the excellent domestic and overseas performance of the semi-new games such as Identity V (第五人格) and Invincible (率土之濱). In addition, the 2017-2019 CAGR of the company's Youdao business and innovative business revenue was 69.2% and 22.3%, respectively. The high growth of Youdao's business revenue during the period was mainly driven by learning services and products (including online courses).

Looking ahead, we expect the company's online game revenue to maintain steady growth, taking into account the company's strong game R&D capabilities and past performance of new games in both China and domestic regions. Further, we expect he online game business in 2020 will benefit from the “stay-at-home” economy. We forecast its revenue growth to be 20% in 2020 and 13-14% in 2021 and 2022, as “stay-at-home” economy fades. As for Youdao's business, we believe that it is currently in a state of “high marketing costs and high income growth”. In addition, the epidemic has greatly popularized K-12 online education in 20H1. Youdao's K- 12 Performance growth was strong in 20H1, with revenue and the number of pay users both recorded large increases. Further, Youdao has added a number of K-12 subjects in 20H1. We believe these new subjects will become its new growth driver in the future. Based on the above reason, we forecast that Youdao's revenue will experience an explosive growth in 2020, about 120% and expect the revenue growth for 2021 and 2022 to be 80% and 60%. Finally, we believe that the company's innovative business, including NetEase Cloud Music, is currently looking for its optimal monetization model, hence based on a conservative approach, we forecast the revenue growth for innovation business in 2020-2022 to be 13% yoy.

GPM and expense ratios

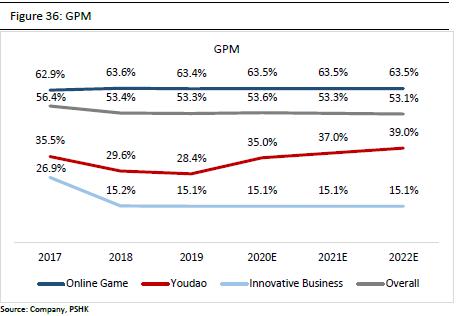

The company's overall GPM in 2018 and 2019 were very stable, at 53.4% and 53.3%, respectively. In terms of online game business, as the business is relatively mature, the GPM of the online game business was basically the same in 2018 and 2019, at 63.6% and 63.4%, respectively. The GPM of innovative business in 2018 and 2019 were also flat at approximately 15.2%. The GPM of innovative business is relatively low, since the company hasn`t workout-ed the optimal monetization models for these business yet. As for Youdao, the GPM in 2019 dropped slightly yoy in 2019, from 29.6% to 28.4%. We expect the future GPM of the company's online game business and innovation business will remain stable, at 63.5% and 15.1%, respectively. We forecast the Youdao GPM will increase yoy for the next 3 years, as the GPM of online courses is likely to rise correspondingly with the scale effect created by the increase in the number of pay users. We expect Youdao's GPM in 2020/2021/2022 to be 35%/37%/39%, respectively.

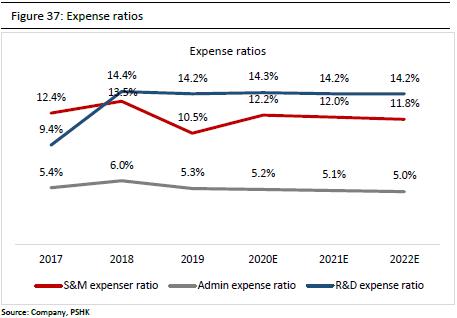

We believe that compared with 2019, the company's future S&M expenses ratio will increase. The main reasons are 1) the increase in the cost of game advertising and 2) Youdao is currently at the state of “high marketing expense, high revenue growth”. Youdao's 2Q20 S&M selling expense ratio was as high as 74.4%, but we think that it will drop yoy with the rapid growth of revenue. Based on the above reasons, we expect that the company's S&M expense ratio to be 12.2%/12.0%/11.8% in 2020-2022. On the other hand, the company's administrative expense ratio in 2017-2019 remained stable at around 5%, and we expect the expense ratio to remain stable in the future. At last. Since 2018, the company has increased its investment in R&D. In 2018, the R&D expense ratio increased by about 5pcts yoy, and then remained stable at about 14%. We believe that the company's strong R&D system is its main moat. Therefore, it is expected that the company will maintain its R&D expense ratio at roughly 14%, and continue to create hit games to maintain its competitive advantage.

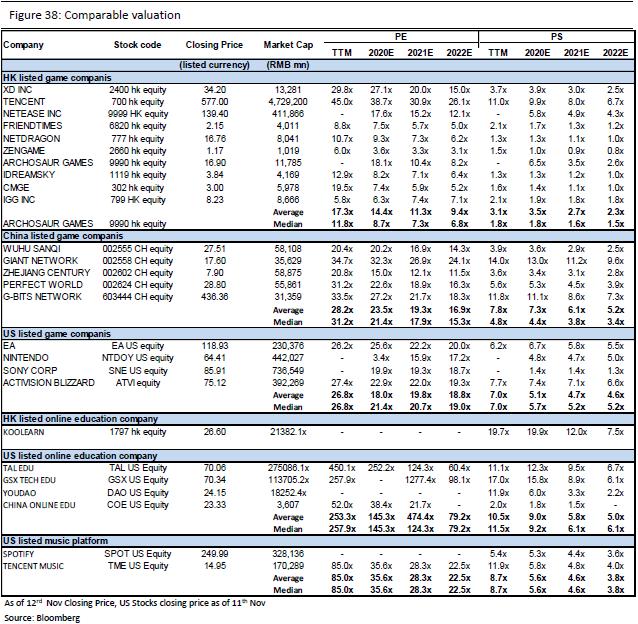

Valuation

We forecast the company's 2020/2021/2022 Non-GAAP EPS to be RMB 5.06/5.75/6.53. We have adopted SOTP to value the company.

1) As of 2020/11/12 market close, the average 2021 PE of HK-listed tier 1-2 game companies is 22.0x. Considered that the company is an obvious leader in this sector, hence it deserves a premium in its valuation. We forecast the Non-GAAP net income for online game business in 2020/2021/2022 to be RMB 16.88/18.76/20.70 billion. We are giving a target 2021 PE of 25x. Hence, we value the company's online game business at HKD 530.06 billion, with respective 2020/2021/2022 PE at 27.8x/25.0x/ 22.7x.

2) As of 2020/11/12 market close, US-listed online education companies have an average 2021 PS of 5.8x. Considered that Youdao is smaller in scale comparing to its peer, hence we are giving a target 2021 PS of 4x to Youdao. We forecast Youdao's 2020/2021/2022 revenue attributable to the company to be RMB 1.68/3.03/4.84 billion. We value the company's share of Youdao at HKD 13.75 billion, with respective 2020/2021/2022 PS at 7.2x/4.0x/2.5x.

3) We forecast the company's revenue share of innovative business in 2020/2021/2022 to be RMB 9.76/11.03/12.46 billion. We are giving a target 2021 PS of 4x, hence we value the company's share of its innovative business at HKD 50.12 billion, with respective 2020/2021/2022 PS at 4.5x/4.0x/3.5x.

In conclusion, we value NetEase at HKD 596.9 billion, with target price at HKD 172.8, with respective 2020/2021/2022 Non-GAAP PE at 29.85x/26.31x/23.14x. We initiate with a BUY rating. (Market closing price as of 12th Nov) (exchange rate: RMB 0.88/HKD)

Risk

1) The tightening on Game regulations 2) The Games underperform comparing to expectation 3) The growth of Youdao is worse than expected 4) Failure in monetization for innovative businesses

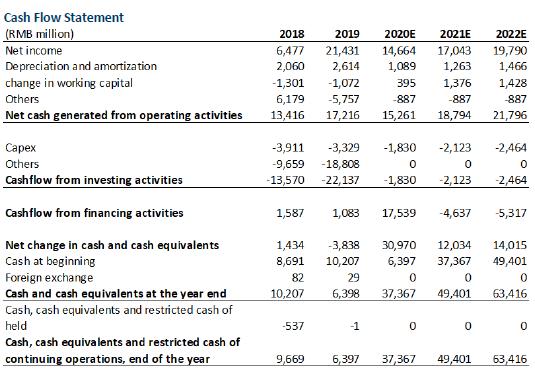

Financial Statements

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()