-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Railway Signal & Communication Corporation Ltd. (3969.HK) - A Leader in Global Rail Transportation Control System Market

Monday, December 3, 2018  7964

7964

China Railway Signal & Communication Corporation Ltd.(3969)

| Recommendation | BUY |

| Price on Recommendation Date | $5.530 |

| Target Price | $7.100 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

China Railway Signal & Communication Corporation (CRSC) is a leader in the global rail transportation control system market. During FY2012-17, its revenue reported CAGR of 26.7%. We forecast revenue growth of 15.54%/18.46% and earnings per share of RMB0.42/0.57 in 2018E/19E, giving target price-earnings ratio 11x, and initiate the target price of HK$7.10. (Closing price at 29 Nov 2018)

Company Business

CRSC, focusing on product design and R&D, has three main business, namely design and integration, equipment manufacturing and system implementation of rail transportation control systems. It is the only rail transportation control system solution provider in the world, which is capable of independently providing the entire suite of products and services with competitive advantages across the whole industry value chain It also provides municipal engineering and related construction services and engages in commodities trading. Since its establishment, CRSC Group, a large-scale central enterprise directly supervised by SASAC, has been a major shareholder of the company, with a share-holding ratio of over 75%.

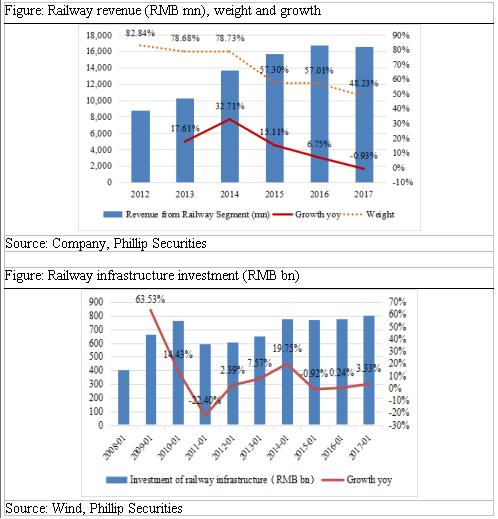

Railway business maintains relatively rapid growth. From 2012 to 2017, the revenue from railway industry grew at a CAGR of 13.7%. In 2017, railway business revenue reached RMB16.6bn, accounting for about 48% in topline. Since 2015, the growth of railway business has slowed down due to the sluggish railway investment after the high-speed rail accident in 2011. Since industry entry barriers is high, the company's market share is ranked at the firs among fierce competition. We predict that in future the company's railway revenue will maintain a relatively rapid growth, mainly benefiting from the growth of railway investment and the renewal of high-speed rail control system.

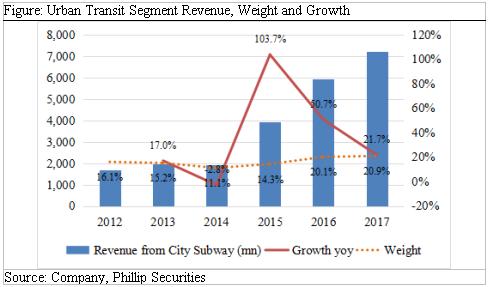

The market potential of urban transit is significant. It is reported that by the end of Jun 2017, there have been 133 rail transit lines opened and put into operation in 31 Chinese cities, with a total operating mileage scale of 4400 km and a mileage scale in construction of 5770 km. It is estimated that by 2020, China's urban transit investment will reach RMB690bn. During FY2012-17, the revenue from urban transit business recorded a CAGR of 33.5%. The amount of external contracts signed from Jan to Sep was RMB79 bn, up 40.0% yoy. This quickly developing segment will continue to serve as an important momentum.

Construction contracting business. The company is engaged in municipal engineering contracting business, involving housing construction, municipal utilities, mechanical and electrical installation, building decoration and other projects. This part of the business is not the main business of the company, but is conducive to strengthening the cooperation between the company and the local government to promote business diversification. Since 2015, the revenue of general contracting business has increased significantly, and the annual compound growth rate of general contracting income in 2015-17 is about 67%.

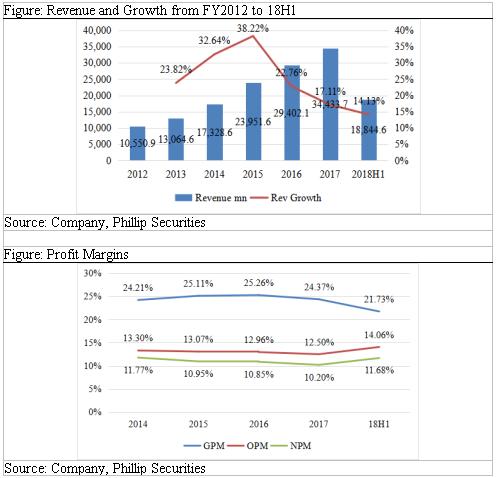

Financial performance. The growth rate of topline has slowed down. given FY12-17 revenue CAGR is 26.7%, while revenue yoy gorwth in 2017/18H1 just report to be 17.11%/14.13%. Gross profit margin has declined in recent years and will rise with the improvement of business structure in the future. Due to effective cost control measures, SG&A expenses decrease year by year. Since its listing, the dividend pay-out ratio has gradually increased and is expected to remain around 40% looking forward.

A leader in global rail transportation control system market

Rail transportation mainly includes railway, urban transit and modern tram. The rail transportation control system enables automatic control of both intervals and speed of trains operating at a high speed and ensures transportation safety while improving efficiency. The rail transportation control system consists of signal system, which comprises ground and on-board signal system, and communication system. The essential part of the signal system is train control system. CRSC has ranked the first in the global rail transportation control system market since 2009.

“Three-in-one” business model. CSRC is the only rail transportation control system solution provider in the world that is capable of independently providing the entire suite of products and services with competitive advantages across the whole industry chain. It provides three main services: (1) Design and integration, provides engineering design and system integration services for rail transportation control system projects, and offers integrated solutions designed to achieve functionality and performance of control system; (2) Equipment manufacturing: manufactures and sells signal system products, communication information system products and other products; and (3) System implementation: provides construction, installation, testing and maintenance services for rail transportation control system projects. Besides, it also provides municipal engineering and related construction services and engages in commodities trading.

Milestones. The company was formerly established by the Ministry of Railways as an electrical design firm. In 1981, the Ministry of Railways approved the establishment of CRSC Group, the controlling shareholder of the company. In 2010, the main body of the listed company was established and in 2015 listed on HKSE main board. CRSC Group has been the major shareholder, with the current share-holding ratio reaching 75.14%. The Group is a large-scale central enterprise directly supervised by SASAC. It has a complete industrial chain which involves the integration , R&D and design, equipment manufacturing, and construction of railway and urban transit communication signal system. The company is growing with China's railway industry. We roughly summarize its development as three main stages. (1) 1953-2007 Normal-speed Railway Stage. Subordinated to the Ministry of Railways, the company is responsible for the design and construction of communication control systems for many railways throughout China. From 1990 to 2007, CRSC's technology was further upgraded with five major speedups of Chinese railway. (2) 2007-2013 High-speed Railway Stage: The company undertook the design and integration of railway signal and communication system of Beijing-Tianjin High-speed Railway, China's first high-speed railway (350 km per hour). The high-speed railway business developed rapidly. (3) Business Diversification After 2013. The company explores urban rail, municipal engineering and other businesses to enhance business diversification.

Railway control system business

This business has slowed down in recent years. In railway market, most customers are affiliated entities of China Railway Corporation. From 2012 to 2017, the segment revenue grew at CAGR of 13.7%, mainly from the high-speed railway business. In 2017, the revenue from the railway business reached RMB16.6bn, accounting for about 48% of topline. Since 2015, the growth of railway business has slowed down. This is because that the start-up of several high-speed rail projects were delayed after the high-speed rail accident in 2011, which reduced the number of new projects started during 2011 to 2013 and dragged down railway investment. Therefore, the mileage of newly opened railway has declined during 2015 to 2017 (given the construction period of high-speed rail projects last generally 4 to 6 years). CRSC's revenue recognition is concentrated around 1.5 years earlier before the opening of new railway, so less launch in 2012-13 led to revenue slowdown in 2016-17.

High entry barriers, mild competition, and largest market share. Due to the technical barriers and specific policies in railway communication industry, the industry has a strict access standards and a high threshold for administrative licensing, which leads to a obvious concentration. There is not many market players in railway wireless communication industry, and the overall market competition is relatively mild. The market scale is accordingly developing with the growth of China's railway construction investment. According to Sullivan's report, by the end of 2014, in terms of the accumulated mileage of the completed high-speed railway control system project, CRSC takes up 65.2% market share, ranking the first.

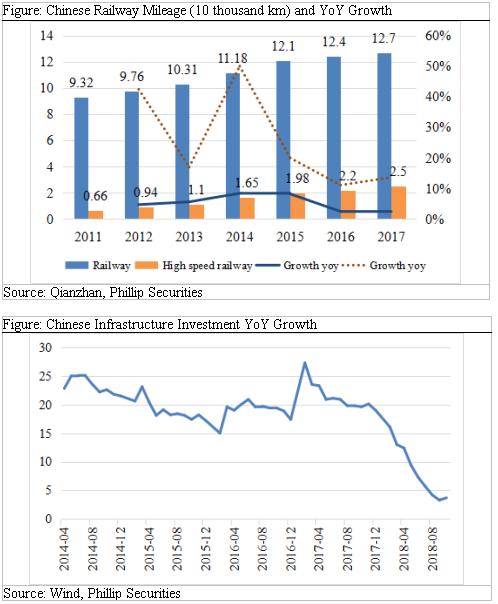

National railway investment is to grow relatively rapidly. In recent years, the operating mileage of China's high-speed railway has been increasing. In 2011, Chinese railways reached 93.2 thousand km, 7% of which is high-speed railways (6.6 thousand km). By the end of 2017, the operating mileage of railways had reached 127 thousand km, 20% of which is high-speed railways (25 thousand km). According to a government plan (《中長期鐵路網規劃(2016-2030)》), by 2020 China will build up 30 thousand km of new railway lines, thus the total railway mileage and high-speed railway mileage will reach 150 thousand km and 30 thousand km. So we estimate that during 2016 to 2020 (十三五) the mileage of newly built railways will maintain a CAGR of at least 5.7%, and 6.3% for newly built high-speed railways. We see that infrastructure investment growth has slowed down since 2017, and bottomed in Sep 2018 around 3.3%, while that rebounded to 3.7% in Oct. In addition, market news confirmed in this August that the investment in railway fixed assets will be increased from RMB732bn to over RMB800bn in 2018E. Therefore, it is expected that China's railway construction will at least maintain a relatively rapid growth in next few years.

Coming upgradation of railway communication facilities. China Railway Corporation is expected to upgrade and replace "wireless train dispatching" system for about 80 thousand km normal-speed railway. In addition, the high-speed railway control & communication system is to be renewed. It has been ten years since the first high-speed railway Beijing-Tianjin line was put into operation in 2008. Due to around 10-year life limit, the control system of high-speed railway has entered the replacement cycle. Based on 20 high-speed railways under construction and operation, assuming that the service life is 10 years and the replacement project cycle is 2 years, the renewal is estimated to involve 242/1236/1631 km of railways in 2019E/20E/21E. If the cost of renewal per km is RMB2mn, the market scale will reach RMB4.8/24.7/1.75bn in 2019E/20E/21E. And the company's revenue will be enlarged by RMB96.9/495/653mn, if 40% market share is grasped.

Railway revenue will maintain a relatively rapid growth in next few years. (1) We see that railway infrastructure investment returned to over RMB700bn level during 2015-17. Thus more railway construction will be finished in 2019E-20E, considering that the construction period is about 4 years. Besides, we also noticed that in the first nine months of 2018, the total amount of external contracts signed for Railways amounts to RMB17.1bn, up by 66.3% yoy, which further proves our viewpoint that the company is expected to recognize more revenue in 2019E-20E. (2) In terms of high-speed rail renewal business, assuming that the service life of control system is 10 years, there will be more than 1000 km per year during 2020E-24E of which the control systems are needed to be replaced. Assuming that the cost of renewal equipment per km is RMB2-3mn, the annual market size should reach more than RMB2-3bn. (3) Since 18Q4, the growth of infrastructure investment has been accelerating. It is expected that railway investment will grow relatively rapidly looking forward, which will benefit CRSC's medium and long-term development.

Urban Rail Transit Business

Huge potential of urban rail transit market. According to Qianzhan's report, by the end of Jun 2017, there have been 133 rail transit lines opened and put into operation in 31 Chinese cities, with a total operating mileage scale of 4400 km and a mileage scale under construction of 5770 km. Urban transit investment capital grew from RMB216.5bn in 2013 to RMB384.7bn in 2016, with a CAGR of over 21%. Assuming 21% CAGR looking forward, it is estimated that by 2020, China's urban rail transit investment will reach RMB690bn.

Good industry prospects lead to fierce competition. At present, the competition is fierce given there are many manufacturers in the wireless communication industry of urban transit. The market concentration is lower than that of the railway market. (1) Due to the clear development prospects of the wireless communication market of urban rail transit in terms of government policies and planning, the sustained investment attracts more equipment manufacturers to approach the industry and intensifies the competition. (2) Competition reveals regionalized. Market players in Beijing, Shanghai, Guangzhou, Shenzhen and other first-tier cities have formed relatively strong competitiveness. While rail transit projects in lower tier cities usually invite tenders from local experienced manufacturers. In recent years, the scale of rail transit construction, mainly in second-tier cities, is experiencing explosive growth. (3) Relatively high entry barriers give current leading firms time to expand market share. Due to high requirement for product safety and the long qualification certification cycle, the market concentration is further improved, and project resources are more often gathered by strengthened companies with outstanding technology, rich project experience and strong overall contracting strength.

CRSC is the largest supplier of urban transit control system. In this market, most of CRSC's customers are metro operators controlled by the local government. The company is the largest supplier of solutions for urban transit control systems in China, accounting for 40.1% market share, based on the total contract awarded between 2011 and 2014. As of end of 2014, CRSC's core rail transit control system products and services cover 39.9% of urban rail transit lines in terms of operating and completed mileages in China. Since the first fully localized urban transit control system (大連市快速軌道交通三號線信號系統工程) contracted by the company in 2004 was put into use, CRSC has continuously innovated the technology of urban transit control system. Given it accelerates the industrializa-tion of the technological research achievements, facilitating the application of the proprietary CBTC system and the commercial use of the achievements of C2+ATO train control system for intercity railway.

Urban transit business growing rapidly. During FY2012-17, the revenue from urban transit business remained CAGR above 33.5%. In 2017, the company's revenue reached RMB7.2bn, up 21.74% yoy, accounting for 21% in total revenue. Overall, urban transit segment has shown a escalated momentum. In 2017, there was more than 860 km of new lines, up 60% yoy. The amount of external contracts signed from Jan to Sep was RMB79 bn, up by 40.0% yoy. We anticipate that the urban transit business will benefit from the rapid expansion of the overall market size and keep an important driver for CRSC.

Construction Contracting Business

Municipal project contracting business involves various types of engineering services, including project design and construction services in relation to building construction, municipal public utilities, mechanical and electrical installation, building decoration, fire fighting facilities, airport runways, smart buildings, environmental protection and pipeline construction. Although this part is not the main business of CRSC, it is conducive to strengthening the collaborative relationship between CRSC and municipal governments. Actively participating in the construction of municipal projects such as smart cities led by local governments and road network projects related to rail transit, will promote more business cooperation between companies and municipal governments.

Increasing segment revenue resulting from business diversification. CRSC adheres to the development strategy of "one core business with diversification into related businesses", vigorously expanding new businesses such as smart city, sponge city, urban comprehensive corridor, etc. The segment revenue increased from RMB3.45bn in 2015 to RMB9.63bn in 2017, with a CAGR of about 67%. In 18H1, this segment reported revenue of RMB5.65bn, up by 45% yoy. During the first nine months, the total amount of external contracts signed by the company in construction contracting and other business was RMB18.53bn, down by 29.9% yoy. Considering that this part is not the main business, its percentage in revenue is expected to decline, after the main businesses accelerated.

Financial Highlights

Revenue growth slightly slowed down. From 2012 to 2017, CRSC revenue maintained a CAGR of 26.7%. In 2017/18H1, its topline reached RMB34.4/18.8bn, up 17.11%/14.13% yoy. Attributable profit reached RMB3.51/22bn, up by 10%/12.1% yoy.

Gross profit margin has declined in recent years and in the future will rise with the improvement of business structure. At present, the proportion of design integration, manufacturing, system implementation and construction contracting in topline is 22%/14.8%/33%/30% respectively, and 5-y average GPM is 36%/36.3%/11%/13.3%. It is expected that in 2019E/20E, with the accelerated growth of railway and urban transit businesses, the income contribution of first three business will increase and overall GPM will be improved.

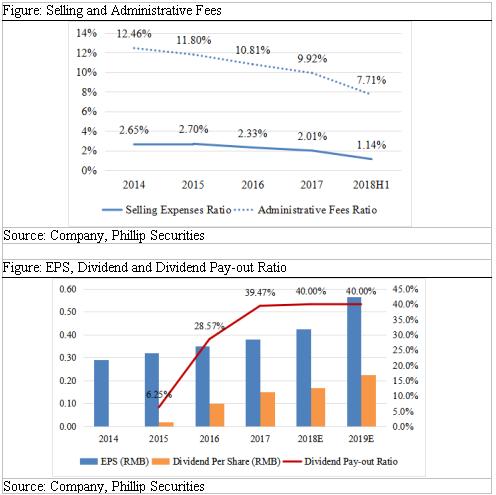

Effective cost control. Though sluggish revenue growth leads to narrowing gross profit margin, operating profit margin rose recently due to the effective cost control measures. Given percentage of selling/administrative expenses in topline decreased from 2.65%/12.46% in 2012 to the current level of 1.14%/7.71%. Excluding the impact of the semi-annual report, we expect that the cost rate of the two items will remain around 1.3%/8% in 2018E/19E.

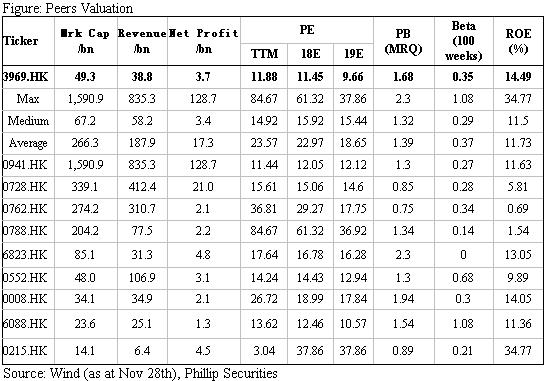

Rising dividend pay-out ratio. Since the company was listed in 2015, the dividend pay-out rate has increased from 6.25% to 39.5% in 2017. Management emphasizes current dividend policy will keep intact in the future if operation results are considerable. We predict that the future dividend rate will remain at 40%.

Valuation and Risks

We initiate target price of HK$7.10. We forecast revenue growth of 15.54%/ 18.46% and EPS of RMB0.42/0.57 in 2018E/19E. Giving a target price-earnings ratio of 11 times, we get the target price of HK$7.10 for 2019E. Risks include: Growth of railway investment fail expectations; Fierce competition in urban rail market leads to bidding failure; Profitability level fail expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()