-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

NETDRAGON (777.HK) - Look forward to the contribution of new business

Tuesday, April 22, 2014  4029

4029

NETDRAGON(777)

| Recommendation | Neutral |

| Price on Recommendation Date | $13.960 |

| Target Price | $14.640 |

Weekly Special - 3993 CMOC Group Limited

Company Profile

NetDragon Websoft Inc. is the leading online gaming and mobile-internet services company focusing on the PRC market. The company researches, develops and operates MMORPG and mobile games.

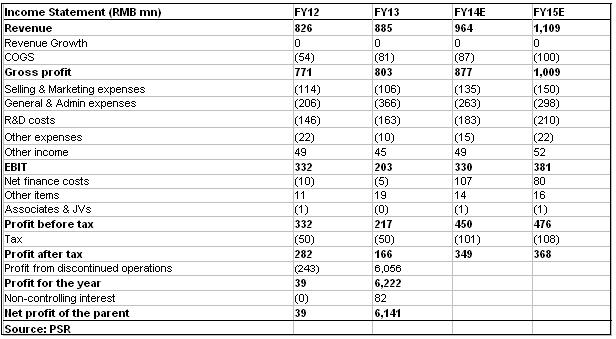

Intensive competition on the online gaming business; a large part of earnings was generated from the disposal of 91 Wireless: According to the company annual report, the adjusted turnover for FY13 grew 7.12% to RMB 885 million, while there was a substantial increase in attributable net income of 157 times to RMB 6.141 billion. This is mainly due to the company disposed its entire 51% of interest in 91 Wireless to Baidu in exchange for a total consideration of approximately RMB 6.7 billion in August 2013. Since then, the company will focus on the game development and operations in its mobile business. However, according to the annual report, the company's online games peak concurrent users (PCU) decreased 8.45% yoy and 6.47% qoq, while the average concurrent users (ACU) also dropped 7.32% and 1.48% respectively. This reflects the company began to lose market share in the extremely competitive online gaming market, and it was necessary to introduce new games in order to restore its market share. In FY14, NetDragon had scheduled to launch 6 new games, including MMORPG, web games and mobile games. It will also launch new patches for its existing games, in order to extend their product life cycles.

A sudden rise admin costs, it is expected to resume normal in the coming year: The administrative expenses in FY13 suddenly increased by more than 70%, reached RMB 366 million, we believe that this was the one-off related expenses for the proposed spin-off listing and the disposal of 91 wireless during the year. We expect that the cost to revenue will restore to normal in FY14

Revenue from online education unforeseen: Selling off the highly competitive wireless platform business in the Red-Ocean with high gross consideration perhaps an appropriate decision. However, the ability of contribution for the Blue-Ocean online education business was still a doubt. NetDragon planned, through enriching the content of its "open educational cloud platform" and connecting to PCs, smart phones, tablet computers and other terminal equipments, thereby to expand its market share and thus revenue. Therefore, the company had entered into an agreement with Foxteq and Vision Knight Capital, and set up two joint venture companies to jointly develop and operate the online education applications market. It was expected the company will gradually increase the revenue mix of the new business, and that would reach over 20% of total revenue in FY16.

Sufficient cash balance for M&A opportunity: After the sales of 91 Wireless, the company distributed a one-time special dividend of HK $ 7.77 per share, a total of RMB 3.13 billion. However, after the cash dividend payment, NetDragon still held more than RMB 44 billion of cash equivalents. This provided sufficient capital for the potential merger and acquisition opportunities.

Valuation: Based on the highly competitive online gaming market faced by the company, while contribution from the online education business is still a doubt, we temporarily give "neutral" rating, with target price HK $ 14.64. This is calculated from the core business valuation of HK $ 5.95 (Forecasted P/E of 7.0x for FY14) plus the discounted 20% of rich cash on hand, valued HK $ 8.69 per share.

Potential risks:

Intensive competition in online and mobile games business, revenue growth slowed down or even reduced

Failure to control costs effectively leaded to increasing ongoing expenses

The new online education business cannot achieve the expected return

Financial Status

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()