-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

Tencent (00700.HK) - AI-powered growth drives robust performance across all business segments

Friday, September 12, 2025  1835

1835

Tencent(700)

| Recommendation | Accumulate |

| Price on Recommendation Date | $633.500 |

| Target Price | $682.000 |

Weekly Special - 2145 CHICMAX

Financial performance

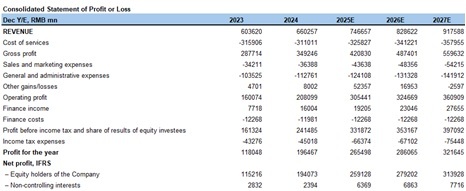

In the second quarter of 2025, the company reported total revenue of CNY 184.5 billion, representing a year-on-year increase of 14.5%. In terms of profitability, operating profit reached CNY 60.1 billion, up 18.5% year-on-year, with the operating profit margin rising from 31.5% in the same period last year to 32.6%. Net profit attributable to equity holders of the company was CNY 55.6 billion, reflecting a year-on-year growth of 16.8%.

By segment, Value-added Services revenue in 2Q25 saw robust growth, increasing by 15.9% year-on-year to CNY 91.4 billion, primarily driven by the sustained stability of top games. Online Marketing Services revenue grew by 19.7% year-on-year to CNY 35.8 billion, benefiting from improved user engagement, continuous AI upgrades to the advertising platform, and optimizations in the WeChat transaction ecosystem. FinTech and Business Services revenue increased by 10.1% year-on-year to CNY 55.5 billion, mainly due to growth in consumer loan services, wealth management services, as well as increased cloud services revenue and merchant service fees.

Performance Summary

Gaming Business

In the second quarter of 2025, the company's game revenue increased by 22.1% year-on-year to CNY 59.2 billion, accounting for 32.0% of total revenue, up from 30.1% in the same period last year. Among this, international market game revenue reached CNY 18.8 billion, a year-on-year increase of 35.3%, primarily driven by revenue growth from PUBG MOBILE and contributions from newly launched games. Domestic market game revenue grew by 16.8% year-on-year to CNY 40.4 billion, benefiting from sustained revenue growth of evergreen titles and the strong performance of the new game Delta Action, which achieved an average DAU of over 20 million in July, ranking among the top five in the industry by daily active users and top three by revenue. With a broader and more platform-diversified game portfolio, management expects reduced volatility in overall game revenue growth.

Social Networks Business

In the second quarter of 2025, the company's Social Networks revenue increased by 6.3% year-on-year to CNY 32.2 billion, primarily driven by growth in game virtual item sales, live streaming services from Channels, and music subscription revenue. WeChat's user traffic continued to grow in 2Q25, with combined MAU reaching 1.411 billion, up 2.9% year-on-year. Meanwhile, monthly active accounts on QQ's smart terminal saw a slight decline compared to the same period last year. The number of registered paid value-added service subscriptions remained stable at 264 million year-on-year. Tencent Music's paid members recorded healthy growth, while Tencent Video's subscription count experienced a decline.

Marketing Services Business

In the second quarter of 2025, the company's online marketing services revenue increased by 19.7% year-on-year to CNY 35.8 billion, primarily driven by AI-powered upgrades in advertising technology and new ad inventory from the Channels transaction ecosystem.

According to management, the company enhanced its AI capabilities across advertising creation, placement, recommendation, and performance analysis, significantly improving ad click-through rates, conversion rates, and return on investment. This was achieved by deploying an upgraded foundational model to revamp the advertising platform architecture, which comprehensively analyzes cross-application/service ad click-through rates, transaction data, and user interactions with text, images, and videos to determine user interests in real time and optimize ad performance.

Management noted that the company's short-form video ad load rate remains in the low single digits, compared to the industry average of 10%-15%. With continued AI-driven microtargeting, growing user traffic, and increasing advertiser demand, management expects advertising revenue to maintain healthy growth.

FinTech and Business Services Business

In the second quarter of 2025, the company's FinTech and Business Services revenue reached CNY 55.5 billion, representing a year-on-year increase of 10.1%. Revenue growth from FinTech services accelerated to mid-to-high single digits, primarily driven by commercial payment services and consumer credit offerings. Business Services revenue achieved double-digit year-on-year growth. Cloud services revenue growth accelerated compared to recent quarters, mainly due to increased demand for GPU leasing to support AI workloads and growth in API token revenue.

Company valuation

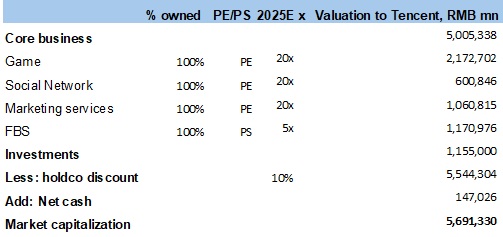

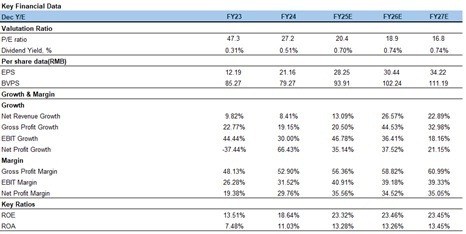

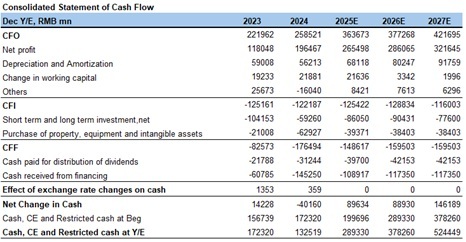

Given the company's better-than-expected growth in gaming and advertising businesses, sustained operating leverage effects, and the empowering role of AI technology across its ecosystem, we have accordingly raised our profit forecasts. Consequently, we upwardly revise our revenue estimates for 2025-2027 to CNY 746.7/828.6/917.6 billion, with adjusted net profit attributable to equity holders projected at CNY 259.1/279.2/313.9 billion. Corresponding EPS estimates are CNY 28/30/34, implying P/E ratios of 20/18/16x at the current share price. Based on SOTP valuation methodology, applying a 10% holding discount to the latest market values or valuations of subsidiaries and invested companies, we derive a total target market capitalization of CNY 5.6 trillion for Tencent in 2025. This corresponds to a target price of HKD 682 per share. We maintain our rating as 'Accumulate'.

Risk factors

1) Strict gaming regulations;

2) Weak macroeconomic environment;

3) Potential competitive threats from existing and emerging social platforms.

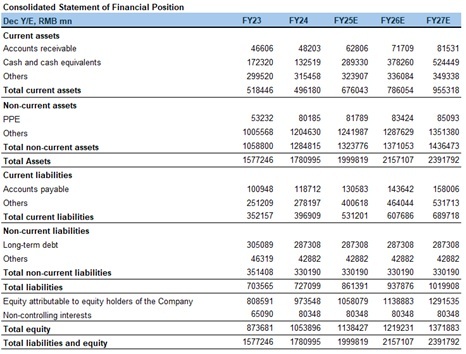

Financials

(Current Price as of: Sep 10 2025)

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()