-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Baguio Green (1397.HK) - Delivered strong financial results in 1H2024

Monday, January 13, 2025  2588

2588

Baguio Green(1397)

| Recommendation | Buy |

| Price on Recommendation Date | $0.630 |

| Target Price | $0.980 |

Weekly Special - 2333 Great Wall Motor

Baguio Green Group (“Baguio”) a leading integrated environmental services provider in Hong Kong, demonstrated robust financial performance in the first half of 2024, driven by its core business resilience and successful government contracts. Operating in essential service sectors including cleaning, waste management and recycling, landscaping, and pest control, the Company maintained growth momentum despite a challenging macroeconomic environment.

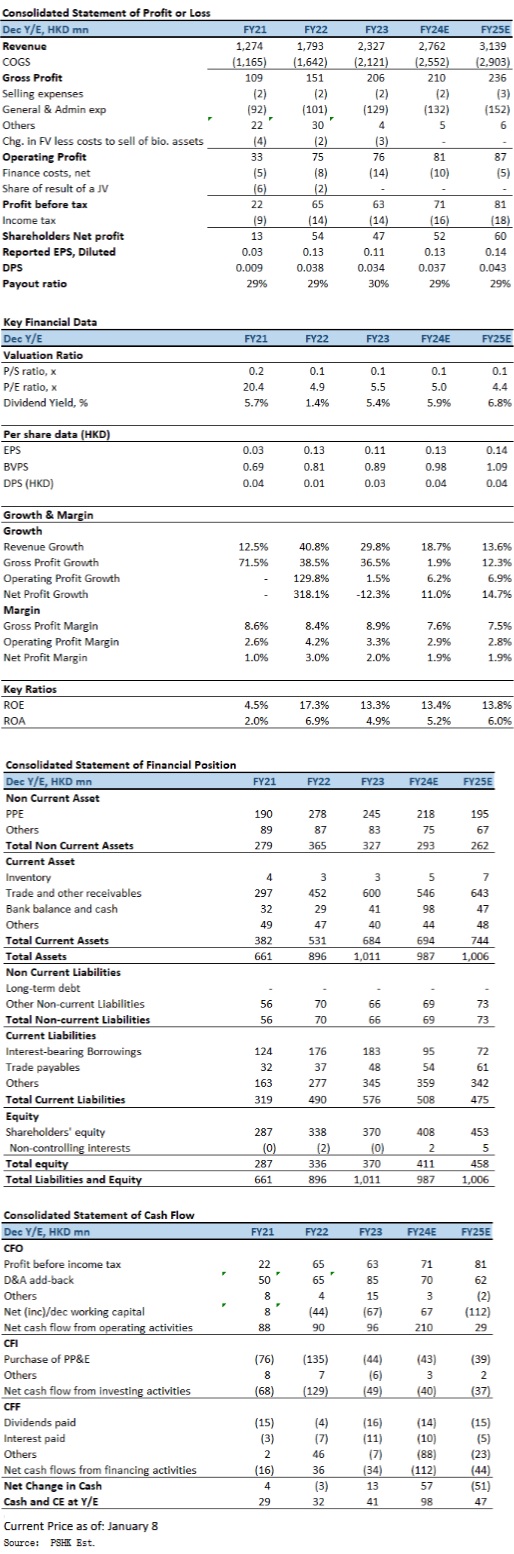

For the six months ended June 30, 2024, Baguio reported revenue of HK$1.291 billion, a year-on-year increase of 16.6%, with profit for the period rising 18.5% to HK$25.8 million. While the gross profit margin declined slightly to 7.5% due to rising labor costs, the strong performance of its cleaning and waste management segments offset this pressure. Baguio remains well-positioned as a provider of essential services with limited exposure to economic cycles, benefiting from growing government initiatives in sustainability and recycling. With a solid financial foundation, diverse revenue streams, and a clear growth trajectory supported by environmental policies, we expect FY2025E-FY2026E EPS to be HK$12.6 cents and HK$14.5 cents respectively, with PT of HK$0.98, implies a FY2025E P/E of 7.8x (~3-yrs historical average). Our investment rating is “Buy”, with an optimistic outlook for its future performance.

Delivered strong financial results in 1H2024

During the first half of 2024, Baguio delivered strong financial results, supported by growth across its major business segments. Revenue increased by 16.6% yoy to HK$1.291 billion, underpinned by a 20.1% surge in cleaning services revenue, which contributed 80.2% of total revenue, reaching HK$1.035 billion. This solid growth reflects the Company's success in securing new government contracts and expanding its service coverage. Additionally, the waste management and recycling segment recorded a 7.4% increase in revenue to HK$147.3 million, with its gross margin improving significantly by 4.2 percentage points to 12.9%, driven by the maturity of the "Plastic Recycling Pilot Scheme" and the addition of new recycling points under government contracts.

Gross profit rose by 12.4% to HK$97.07 million, despite a slight decline in the overall gross margin from 7.8% to 7.5%, mainly due to higher labor costs in the cleaning segment. This impact was mitigated by the improved profitability of the waste management and pest control segments, highlighting Baguio's ability to balance risks through its diversified business portfolio.

On cost management, administrative expenses remained well-controlled, with their share of total revenue decreasing to 4.8%. The Company also exhibited a healthy financial position, with its current ratio improving from 1.2x at the end of 2023 to 1.3x as of June 30, 2024. Bank borrowings decreased significantly by 47.5% year-on-year, and cash and bank balances surged by 84.3% to HK$76.3 million, reflecting improved liquidity and reduced financial leverage.

Baguio operates in four core segments: cleaning, waste management and recycling, landscaping, and pest control. These services are closely tied to the daily lives of Hong Kong residents. Cleaning services, the largest revenue contributor, benefited from comprehensive government contracts covering seven districts and serving a population of approximately 2.8 million. This reinforces Baguio's market leadership in Hong Kong's environmental services sector.

The waste management and recycling segment saw strong growth, bolstered by government initiatives to enhance recycling infrastructure. Despite the temporary suspension of the municipal waste charging scheme, the government accelerated its investment in recycling facilities, such as smart food waste recycling machines and mobile collection points. This directly drove growth in Baguio's recycling business. As a key contractor under the government's "Plastic Recycling Pilot Scheme," the Company is well-positioned to benefit from the upcoming Producer Responsibility Scheme for Beverage Containers, which is expected to further drive recycling volumes.

In addition, green technology has emerged as a new growth driver for Baguio. The Company has introduced smart recycling systems that integrate IoT technology and real-time data analytics, improving operational efficiency while reducing carbon emissions, which is highly consistent with the Hong Kong government's smart city and "Zero Landfill" goals. Its biochar plant, which began trial operations during the period, utilizes pyrolysis technology to convert yard waste into high-quality biochar, and further explored a high value-added environmental protection business model.

Investment Thesis

Looking ahead, we expect Baguio to continue benefiting from the government's increased focus on environmental sustainability, including expanding the food waste recycling market and implementing the Producer Responsibility Scheme for Beverage Containers. According to 2022 data, Hong Kong generates approximately 3,330 tonnes of food waste daily, while current processing capacity stands at only 600 tonnes. This indicates enormous growth potential in the food waste recycling market. As a leader in Hong Kong's recycling industry, Baguio is well-positioned to capitalize on this opportunity, particularly with its smart food waste recycling machines already deployed across the city. Furthermore, the development of the Northern Metropolis is expected to create additional opportunities for Baguio's core services. The region is anticipated to provide 500,000 new housing units. These developments are likely to drive demand for cleaning and waste management services, providing sustained revenue growth for the Company. Financially, Baguio's contracts on hand as of June 30, 2024, reached HK$4.6 billion, with HK$1302 million scheduled for recognition by the end of 2024 and HK$3297 million to be recognised over the next two years. This strong pipeline ensures high revenue visibility in the near to medium term. We expect FY2025E-FY2026E EPS to be HK$12.6 cents and HK$14.5 cents respectively, with PT of HK$0.98, implies a FY2025E P/E of 7.8x (~3-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()