-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Binhai Investment (2886.HK) - Earnings recovery in FY2025, improving dividend payouts enhances shareholder returns

Wednesday, April 2, 2025  3505

3505

Binhai Investment(2886)

| Recommendation | Neutral |

| Price on Recommendation Date | $1.100 |

| Target Price | $1.050 |

Weekly Special - 2333 Great Wall Motor

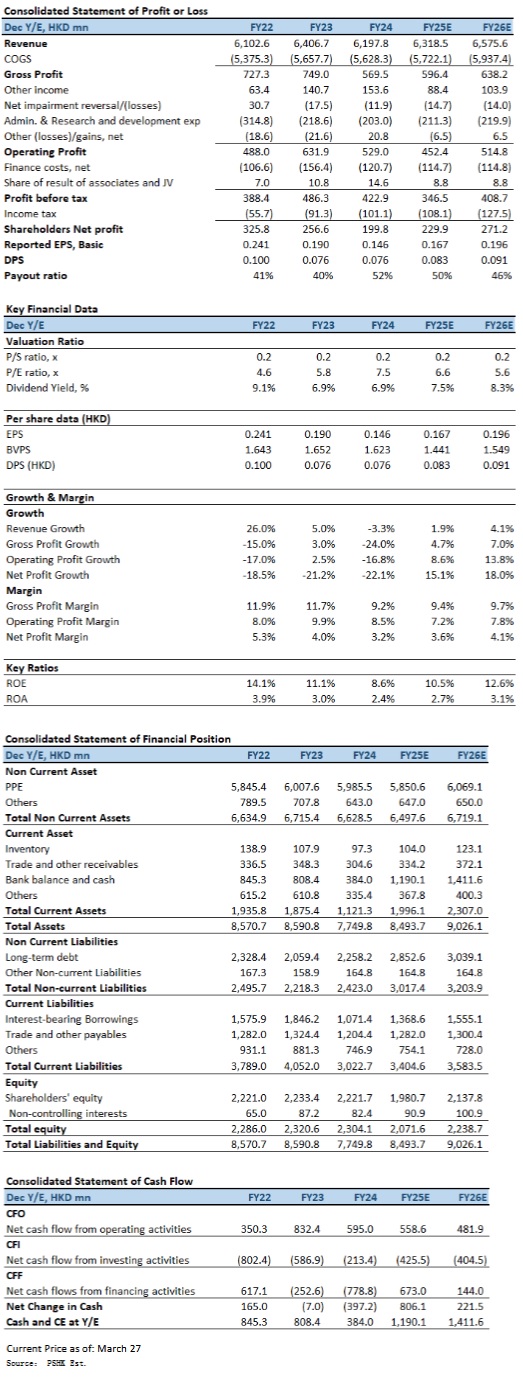

Binhai Investment (02886.HK) announced its financial results for the fiscal year ending December 2024, with overall performance impacted by prolonged weakness in the real estate sector, a mild winter in northern China, and RMB depreciation. Total revenue declined by 3% YoY to HK$6.198 billion, net profit fell by 21% to HK$209 million, and profit attributable to shareholders dropped by 22% to HK$200 million. Basic earnings per share (EPS) stood at HK$0.146, while dividend per share remained stable at HK$0.076. The company plans to gradually increase dividends by no less than 10% annually over the next three years.

Revenue and Profitability Analysis

Company's revenue recorded a 3% YoY decline in FY2024, primarily due to the downturn in the real estate sector, which led to a sharp 35% drop in revenue from engineering construction and natural gas pipeline installation services to HK$327 million. Meanwhile, pipeline natural gas sales remained largely stable at HK$5.803 billion, down only 0.8%. The natural gas transmission business, however, demonstrated strong growth, with revenue rising by 32% YoY to HK$68 million, driven by increased gas demand from power plant customers.

In terms of gross profit, the company reported a 24% YoY decline to HK$569 million (FY2023: HK$749 million), with the gross profit margin contracting from 11.7% to 9.2%. This was mainly due to a higher proportion of lower-margin pipeline gas sales and a decline in engineering service revenue, leading to an unfavorable business mix. However, the company successfully optimized its procurement strategy, reducing purchase costs and implementing price adjustments in the end market, contributing to a HK$0.17 per cubic meter increase in urban gas gross margin in 2H24, rising from HK$0.41 in 1H24 to HK$0.58 in 2H24. Additionally, the value-added services segment sustained strong profitability, with gross profit growing 10% YoY to HK$54.67 million. This segment maintained a compound annual growth rate (CAGR) of 42% over the past four years, demonstrating robust earnings potential. On the financing side, the company's weighted average financing cost decreased by 20 basis points to 5.3% in 2024. It also optimized its debt structure, reducing the proportion of USD-denominated financing from 26% to 20%. Furthermore, the company improved its loan maturity profile, lowering the share of short-term borrowings (maturing within one year) from 47% to 32%, while increasing the proportion of long-term borrowings (above five years) from 6% to 16%, effectively mitigating short-term liquidity risks.

Segment Performance

Sales volume reached 1.714 billion cubic meters, up 6.5% YoY. However, due to a warmer-than-expected winter, heating season demand underperformed, resulting in flat revenue at HK$5.803 billion (FY2023: HK$5.850 billion). Industrial and commercial gas consumption increased from 80% to 81% of total volume, while residential consumption declined from 20% to 19%, reflecting structural changes in end-user demand.

Transmission volume rose 32% YoY to 801 million cubic meters, exceeding initial targets. This was mainly driven by increased power generation tasks among power plant customers and the company's ability to leverage its resource pool to flexibly allocate gas supply. Revenue from this segment grew by 32% to HK$68 million (FY2023: HK$52 million), and future growth is expected to remain stable.

Revenue from Construction & Pipeline Installation Services recorded a significant 35% YoY decline to HK$327 million (FY2023: HK$505 million), as the sluggish real estate market led to fewer new projects. However, total user connections continued to grow steadily, reaching 2.44 million households by the end of 2024, a 3% increase from 2023. Notably, industrial and commercial users grew by 9%.

Value-Added Services maintained strong momentum, with gross profit rising 10% YoY to HK$54.67 million, achieving a gross margin of 73%. Gas appliance sales saw a notable improvement in profitability, with gross margin increasing from 43% to 49%, driven by the launch of the company's proprietary brand, "TAIYUEJIA". Additionally, the company plans to expand into e-commerce platforms and smart security solutions to further penetrate the B2B and B2C markets, enhancing overall profitability.

Financial Position

As of December 2024, total current assets stood at HK$1.121 billion (FY2023: HK$1.875 billion), while current liabilities amounted to HK$3.023 billion (FY2023: HK$4.052 billion), resulting in a current ratio of 0.37, indicating ongoing short-term liquidity pressure. However, through debt structure optimization, the company successfully reduced its gearing ratio from 73% to 70% and lowered its exposure to foreign currency loans, mitigating FX risk. Additionally, the company actively pursued government-backed ultra-long special treasury bonds funding. In 2024, it secured HK$86.78 million in approved funding, with HK$39.36 million received. The company plans to apply for an additional HK$1.05 billion in 2025 to support gas pipeline safety upgrades and urban renewal projects.

Investment Thesis

Looking ahead to 2025, the company targets a total gas sales volume of 2.7 billion cubic meters, representing a 9% YoY increase. Pipeline natural gas sales are expected to reach 1.9 billion cubic meters, growing 9% YoY, while gas transmission volume is projected to remain stable. Urban gas gross margin is anticipated to improve to HK$0.52 per cubic meter. In terms of capital management, the company plans to further reduce financing costs by RMB 20 million while maintaining HK$500 million in capital expenditures to support business expansion. Additionally, it aims to increase dividend payouts annually by no less than 10% from 2025 to 2027, with the dividend per share expected to rise to HK$0.10 by 2027. The company also plans to optimize its gas procurement strategy to mitigate supply chain risks and enhance upstream direct sourcing while expanding its downstream market presence. In 2025, it will continue strengthening partnerships with "three barrels of oil" (i.e. CNPC, SINOPEC and CNOOC), Beijing Gas Group, and China Suntien Green Energy to further optimize procurement costs. Despite short-term headwinds impacting profitability in FY2024, efforts in procurement optimization, debt restructuring, and end-market expansion should support earnings recovery in FY2025. Additionally, the company's commitment to improving dividend payouts enhances shareholder returns. We expect FY2025E-FY2026E EPS to be HK$0.167 and HK$0.196 respectively, with PT of HK$1.05, implies a FY2025E P/E of 6.3x (~5-yrs historical average). Our investment rating is “Neutral”.

Risk factors

1) Higher-than-expected increases in natural gas procurement costs; 2) Significant fluctuations in RMB exchange rates; 3) Weaker-than-expected economic recovery momentum.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()