-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李曉然小姐(Margaret Li)

分析師

分析師

本科主修市場行銷和英語,並於香港浸會大學獲得經濟學碩士學位。現為輝立証券持牌分析師,主要負責能源和公用事業等板塊的研究。曾在大型銀行、券商和資產管理公司工作,對於期貨和大宗商品衍生品領域擁有銷售、研究分析和市場推廣等工作經驗。

Margaret, a holder of a Bachelor`s degree in Marketing and English and a Master`s degree in Applied Economics from Hong Kong Baptist University, is currently employed as a licensed analyst at Phillip Securities. She specializes in conducting research focusing on the energy and utilities sectors. Prior to her current position, Margaret gained valuable work experience in a large bank, securities firm, and asset management companies. Her expertise lies in sales, research analysis, and marketing within the fields of futures and commodities derivatives.

| Phone: | 22776535 | Email: | margaretli@phillip.com.hk | |

CMOC Group Limited (3993.HK) - The production and sales of major products such as copper, cobalt were booming, and the cooperation agreement of the Nzilo II hydropower station in the Democratic Republic of the Congo (DRC) has been signed.

Thursday, November 7, 2024  3634

3634

CMOC Group Limited(3993)

| Recommendation | Accumulate |

| Price on Recommendation Date | $6.870 |

| Target Price | $7.770 |

Weekly Special - 2333 Great Wall Motor

Overview

CMOC (3993.HK) engages in the non-ferrous metal industry, mainly the mining and processing business, which includes mining, beneficiation and smelting of base and rare metals, and mineral trading business. With its main business located over Asia, Africa, South America and Europe, the Company is a leading producer of copper, cobalt, molybdenum, tungsten and niobium in the world. It is also a leading producer of phosphate fertilizer in Brazil. In terms of trading business, the Company is one of the leading metal traders in the world. CMOC is one of the very few mining companies that has mastered a world-class metals trading platform.

Company Performance review

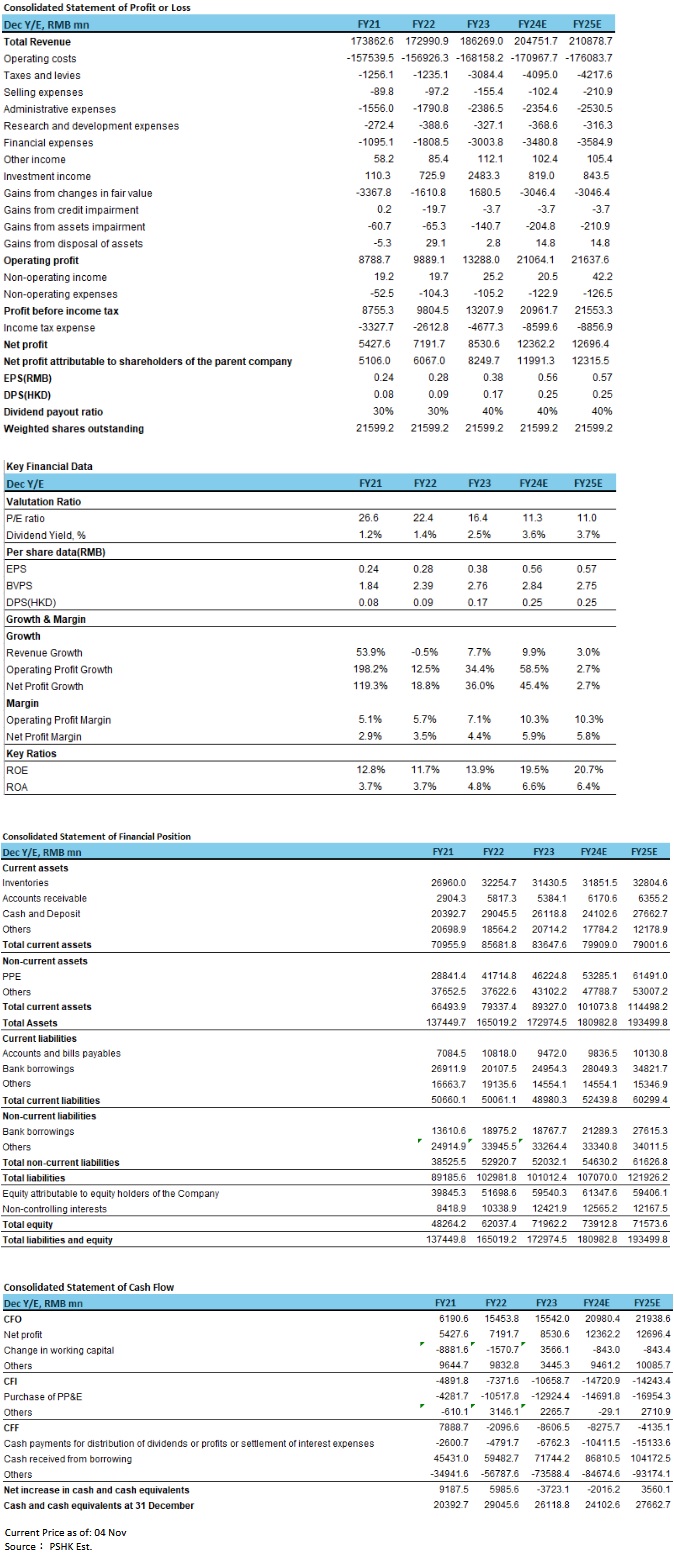

The company's operating income in the third quarter of 2024 was 51.94 billion yuan (RMB, the same below), a year-on-year increase of 15.53%; the net profit attributable to shareholders of listed companies was 2.84 billion yuan, a year-on-year increase of 64.12%; EPS was 0.14 yuan. From January to September, operating income was 154.75 billion yuan, a year-on-year increase of 17.52%; net profit attributable to shareholders of listed companies was 8.27 billion yuan, a year-on-year increase of 238.62%; EPS was 0.39 yuan. The company's production and sales of copper and cobalt products had increased, the overall cost had decreased compared with the same period last year, and profits had increased year-on-year.

The production and sales of major products such as copper, cobalt were booming

During the third quarter of 2024, the Company's new projects, TFM western area and KFM Phase II have carried out preliminary exploration, and the mineralization effect was good. In the first half of 2024, TFM and KFM maintained a fast-paced production mode with output exceeded their targets, achieving record-breaking monthly output and achieved significant results of cost reduction and efficiency improvement. TFM became the first mine in Africa and the first Chinese-owned mine in the world to be awarded The Copper Mark certificate. Through process adjustment and technological innovation, the recovery rate of copper and cobalt had been greatly improved. In the first three quarters of 2024, the company's copper output reached 0.48 million tons, a year-on-year increase of 78.20%, and its sales volume reached 0.47 million tons, a year-on-year increase of 160.98%; its cobalt output reached 0.08 million tons, a year-on-year increase of 127.39%, and its sales volume reached 0.08 million tons, a year-on-year increase of 1,021.07 %; molybdenum production reached 0.01 million tons, a year-on-year decrease of 6.34%, and sales volume reached 0.01 million tons, a year-on-year decrease of 6.91%; tungsten production reached 6,129 tons, a year-on-year increase of 3.79%, and sales volume reached 5,919 tons, a year-on-year increase of 4.02%; niobium production reached 7,682 tons, a year-on-year increase of 5.40%, sales volume reached 7,555 tons, a year-on-year increase of 8.65%; phosphate fertilizer output reached 0.90 million tons, a year-on-year increase of 2.26%, and sales volume reached 0.86 million tons, a year-on-year decrease of 4.74%.

Valuation and recommendation

CMOC has provided guidance for the annual output of its main products in 2024. Among them, copper output is expected to be 520,000-570,000 tons, significantly exceeding the actual output in 2023; cobalt output is expected to be 60,000-70,000 tons; molybdenum output is expected to be 12,000-15,000 tons; tungsten output is expected to be 6,500-7,500 tons; niobium output is expected to be 9,000-10,000 tons; phosphate fertilizers output is expected to be 1.05-1.25 million tons.

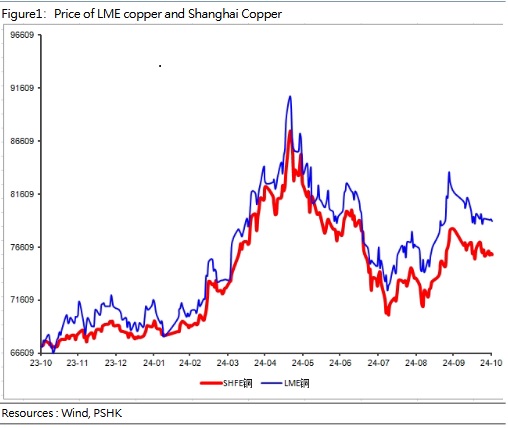

Affected by the shortage of mine supply, expected reductions in refined copper production, and sanctions on Russian metals, copper prices increased significantly from January to May this year, and subsequently fell back as demand from China weakened. BHP Billiton, the world's largest mining company, predicted that the development of AI will aggravate the copper shortage. The company predicted that global copper demand will increase from 30.4 million tons per year in 2021 to 52.5 million tons in 2050, an increase of 72%. In the future, AI Development may become a new growth point for copper demand. Starting from October, interference in the smelting process has increased, and domestic supply is expected to continue to decrease. The consumption side is not strong, but the market is placing its hope on China to issue more stimulus measures. As the United States presidential election is coming, there is no determination of direction. It is expected that copper price will be at a high level and fluctuate in the short term.

The International Cobalt Industry Association predicted that cobalt supply will be approximately 305,000 tons in 2024, while demand will be approximately 251,000 tons. Global cobalt resources are concentrated. After the increased amount in existing supply is released, it is expected that there will be few new resources in the long term. The main terminal demand for cobalt comes from new energy vehicle power batteries. From July to September this year, the penetration rate of new energy vehicles exceeded 50% for three consecutive months. Cobalt demand is expected to grow further in the future, and cobalt price may grow in the medium and long term.

The demand for high-end steel types such as molybdenum-containing steel is expected to return to high levels later. The strategic requirements for the overall upgrading of the manufacturing industry will also promote the overall upgrading of the steel industry, and the demand for special steel products will continue to increase. The supply and demand of Molybdenum will remain tightly balanced and price may become more stable. The company continues to be optimistic about the molybdenum market. There is no large-scale new production capacity released on the molybdenum supply side. At the same time, large-scale molybdenum mines are facing varying degrees of decline in raw ore grades. New production capacity at the smelting end and chemical end will be gradually invested, which will further absorb raw materials.

The tungsten market is expected to remain in tight supply, and tungsten price is expected to maintain steady growth.

Recently, the government had been continuously issuing favorable policies such as subsidies for home appliances and new energy vehicles, which is expected to increase the demand for special steel, thus increasing the demand for niobium. The price of niobium is expected to rise in the future.

The third quarter is the traditional peak season for fertilizer sales in Brazil. Fertilizer price is expected to continue to rise and return to stabilization in the fourth quarter.

We predict that the company's revenue will be 204.8 billion yuan and 210.9 billion yuan respectively in 2024 and 2025, EPS will be 0.56/0.57 yuan per share, and the BVPS will be 2.84/2.75 yuan per share, P/B will be 2.21x/2.28x. The company has world-class mining resources. Congo (DRC) TFM is one of the world's largest copper and cobalt mines, KFM is the world's largest cobalt mine, Brazil's niobium mine is the world's second largest niobium mine, China's Sandaozhuang molybdenum and tungsten mine is one of the largest molybdenum mines in the world. The company's resources cover basic metals and special metals, which are closely related to the fields of energy transformation and industrial upgrading. At the same time, it is involved in agricultural applications through phosphorus. In the field of new energy metals, the company has important layouts in copper and cobalt, and is the world's leading new energy metal producer. It also has unique and scarce product portfolios such as molybdenum, tungsten, niobium, and phosphorus, all of which have leading industry positions. The cooperation agreement of the Nzilo II hydropower station in the Democratic Republic of the Congo (DRC) has been signed, and the power generation capacity of 200 MW will provide long-term and stable power guarantee for a new round of capacity leapfrogging. We believe that the company's in-depth development in the copper and cobalt industries will achieve more significant results in the future, giving the company a P/B of 2.5 times in 2024, a target price of HK$7.7, and an "Accumulate" rating. (Current price as of Nov 04)

Risk factors

Main product price fluctuations, geopolitical and policy risks, interest rate risks, exchange rate risks, safety and environmental protection and natural disaster risks.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()