-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Railway Signal & Communication (3969.HK) - Advantage Prominent but Undervalued

Tuesday, May 3, 2016  22228

22228

China Railway Signal & Communication(3969)

| Recommendation | Buy |

| Price on Recommendation Date | $4.620 |

| Target Price | $5.560 |

Weekly Special - 1836 Stella International

Stable Growth in 2015

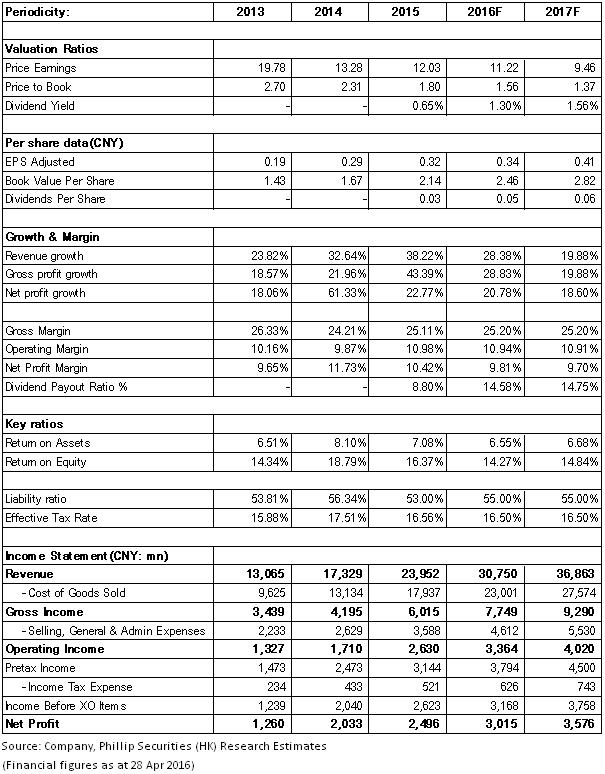

China Railway Signal & Communication (CRSC) is the world's largest solution provider for rail control system. With world's leading technology, it has monopolistic advantages in the field of railway signal, and is the leader in other rail traffic signal fields. In 2015, the company recorded the revenue of RMB23.95 billion, up 38.2% year-on-year. The net profit was RMB2.5 billion, an increase of 22.8%.

Among the three businesses, the revenue of design integration business increased by 18.3% to RMB5.808 billion, and the revenue of equipment manufacturing business grew by 17.6% to RMB6.9 billion, and that of the system delivery business increased by 38.6% to RMB7.44 billion. The three businesses were mainly benefited from the stable development of Chinese rail transit industry. In addition, the revenue of other businesses soared by 221.9% to RMB3.8 billion, which was also benefited from the company's efforts in vigorously developing related business besides devoting to signal business in the meantime.

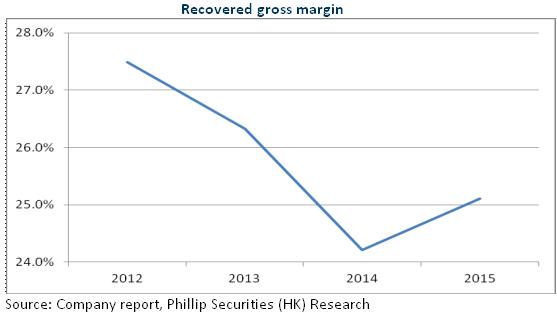

As for the profitability, the company reversed the small decline in the last two years, resulting in a year-on-year increase in gross profit margin by 0.9% to 25.1%. The gross profit margin of design integration, equipment manufacturing and delivery system businesses increased by 3.8%, 3.0% and 1.0%, respectively as the company reduced the cost and increased the efficiency through fine management and adjustments of sales structure. However, the company's operating expenses increased a bit faster as the sales expenses grew by 41%, mainly on expansion of the business. The administrative cost grew by 31% due to the increased R&D input, which also dragged down the company's result growth.

Rapid Outbreak in Urban Rail and Overseas Market

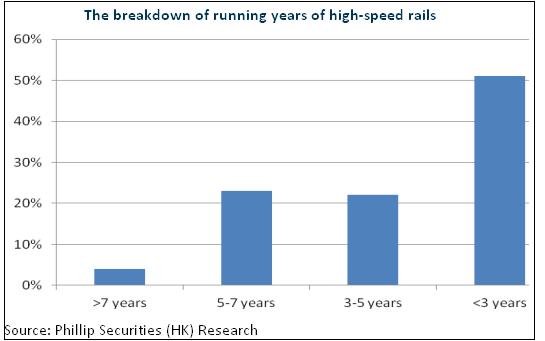

The rapid growth period of railway business has come to past already, and the 12,000 km high-speed railway newly built during the “13th Five-Year Plan” will maintain a normal growth in the railway sector. However, China's vast rail network will face huge market in terms of system upgrade and operation maintenance. Currently, the high-speed rails running over 7 years account for only 4% of the total operating mileage, but those running for 5 to 7 years take up about 23%. Thus, the revenue from operation and maintenance is expected to rise soon. In general, the railway business is still expected to experience a double-digit growth continuously in the future.

The company has equipped Line 8 of Beijing Subway with its CBTC system of proprietary intellectual property rights, and will cooperate with CASCO to seek more metro market opportunities. Rapid growth is expected to take place in 2016. Tram market has been rising rapidly with its advantages of low cost, short construction cycle, large capacity and use of clean energy. The estimated annual growth is expected to be 64%. As the leader in control system of this field, the company is expected to take up over 40% of market share. Presently, the company has officially started its construction project cooperated with Tianshui City in PPP mode. In 2015, the company signed new contracts in the field of urban rail transit, worth RMB9.92 billion with a Y-o-Y increase of 209.1%, which will support the rapid growth in coming two years.

Besides, although the proportion of revenue from overseas market decreased slightly in 2015, the total amount of contracts newly signed increased by 57%. Projects of Indonesia high-speed railway and Mongolia-Inner Mongolia railway will contribute to profits if they both progress smoothly in 2016. The company's high-speed railway technology connects with European standard seamlessly, which can help its “One Belt, One Road” oversea expansion face a promising prospect.

Advantage Prominent but Undervalued

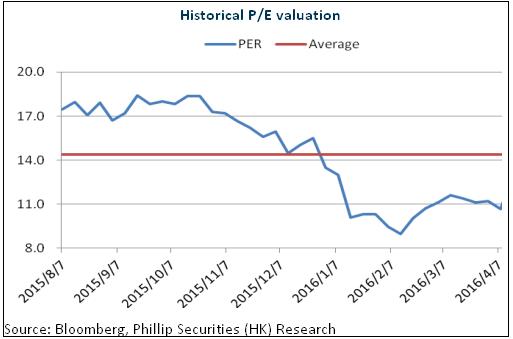

With leading technology, oligopoly status, sufficient funds and lower debt ratio, CRSC not only maintains a steady growth in the field of railway, but will also expand rapidly in emerging areas such as PPP. In addition, the company will maintain an explosive growth on urban rail transit market. Meanwhile, the company will continue relying on reducing cost and increasing efficiency, bulk procurement and lean management, thus maintaining the gross profit margin at 25%. Therefore, the company is still expected to experience a promising prospect in rapid growth. We give an estimation of 13.5x EPS in 2016, and the target price is HKD5.56, with the "Buy" initially. (Closing price as at 28 Apr 2016)

Risks

The development of overseas business could not meet expectation.

Safety accidents break out.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()