-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Dongfeng Group (489.HK) - New power from launch of new models in 2014

Monday, May 19, 2014  8492

8492

Dongfeng Group(489)

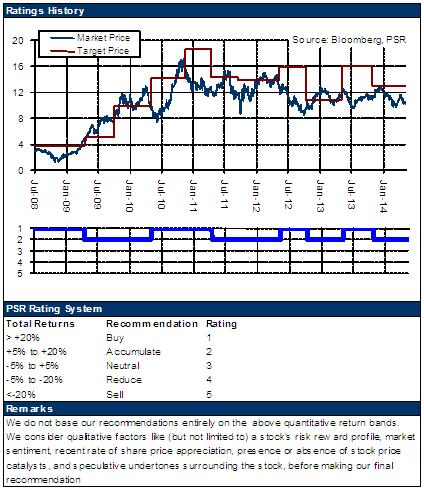

| Recommendation | Accumulate |

| Price on Recommendation Date | $10.280 |

| Target Price | $12.300 |

Weekly Special - 002050 Sanhua

Company Profile

As the third largest automaker in China, Dongfeng is primarily engaged in the manufacture and sale of commercial vehicles, passenger vehicles and auto engines and parts as well as other automotive-related businesses. It listed in HKEx in 2005. Under its banner there are 3 joint ventures Dongfeng Nissan, Dongfeng Peugeot Citroen and Dongfeng Honda.

Summary

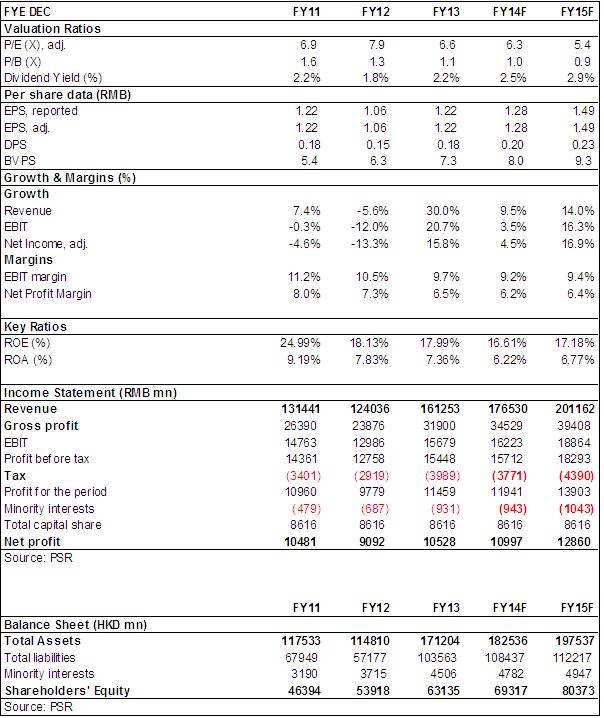

-FY2013 result review: Revenues of Dongfeng Group in 2013 amounted to 161.253 billion (the proportionate consolidation method), up 30% y-y. Net profit attributable to the parent company was 10.528 billion, increased by 15.8% y-y. The EPS was 1.22 compared with 1.06 in last year, and the DPS recorded 18 cents compared with 15 cents in last year.

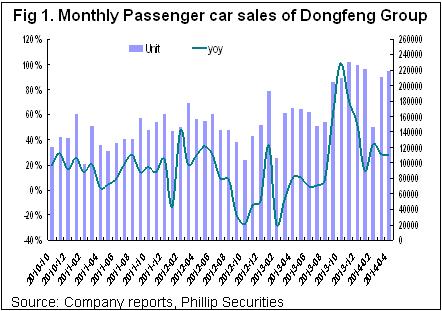

-Sales volume amounted to 2.57 million, up 19%: The sales volume of the Group in 2013 increased by 19.1% y-y to 2,567,700 units, the growth rate trended to go up from the low rate at the beginning, and the market share grew 0.52ppts to 11.7%. APS of passenger and commercial vehicles increased by 0.2% and 51% respectively benefited from the better structure of sales

-13H2 saw obvious improvement: The performance developed obviously in 2H2013 as our expectation, net profit increased largely by 34% y-y, main reasons are: 1) low base affected by the political event at the same period of 2012, 2) the quantity increased after important models launched, 3) the strong recovery of heavy-duty truck industry from the middle of 2013. The gross margin increased from 19.2% in 2012 to 19.8% affected by the above positive factors, the gross margin of passenger vehicles increased by 0.4ppts from 20.8% to 21.2%, and the gross margin of commercial vehicles grew 1.8ppts from 12.7% to 14.5%. However, sales and administrative expenses, and financial cost ratio increased due to the growth of the market promotion expense, labor cost and R&D.

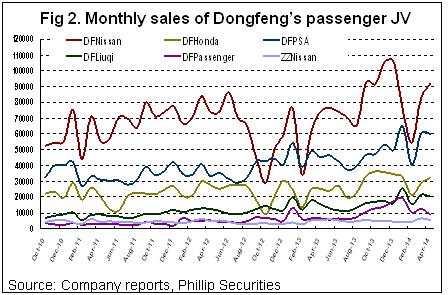

-Lack of the sustained momentum for strong recovery: On a closer look, passenger vehicles were sold by 2,118,500 units, up 21.7% y-y, and commercial vehicles were sold by 449,200 units, up 8.3% y-y. In the Group's joint venture companies, the growth of Japanese cars was lower than others: The sales volume of Dongfeng Nissan rose 20% y-y to 926,000 units, Dongfeng Honda increased by 14% y-y to 320,000 units, Dongfeng PSA grew 25% y-y to 550,000 units, and self-owned brand Fengshen sold 80,000 units, up 33% y-y.

Dongfeng Liuzhou sold about 180,000 units, up 32% y-y, and Zhengzhou Nissan sold 55,000 units, increased by 16% y-y. According to the latest sales data of 2014, there seemed to be lack of the sustainability of the strong recovery for its main models although the Japanese JVs have resuscitated. From March 2014, the sales volume of Venucia's two models started to increase, total sales surpassed 10,000 units, but Teana only sold around 25,000 units in 1Q2014, much inferior to the German peers.

-New power of sales due to the launch of new models in 2014: the Company's sales target is 2.84 million units in 2014, up 10.6% y-y, with 2.4 million units of passenger vehicles (+13.3%), and 0.4 million units of commercial vehicles (-11%). According to JV companies, the targets are Dongfeng Nissan's 1.05-1.1 million units, Dongfeng Citroen's 0.6-0.65 million units, Dongfeng Honda's 0.35 million units, and the self-owned brand, Aeolus's 0.1 million units, increased by 13.4-18.8%, 9.1-18.2%, 9.4% and 25% y-y respectively. The Group is planning to introduce 10 new passenger vehicles among which four of them focus on the current popular SUV market, including Dongfeng Nissan's new X-Trail, Infinite's domestic model Q50L, Venucia's A0-class model R30 and a new model of SUV, Dongfeng Honda's new Spirior, Dongfeng PSA's new 408 and SUV2008, the self-owned brand, Fengshen's compact sedan D23 and SUVG29, and Dongfeng Liuzhou's Joyear S3 and DM7.

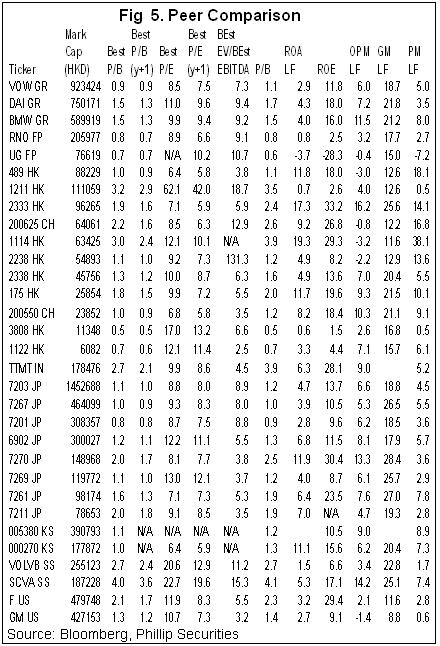

-Valuation and rating: We have respectively adjusted the company's profits forecast and revise our target price for 12 months to HK$12.3, equivalent to 7.6/6.4xP/E and 1.2/1.0xP/B in2014/2015 respectively, which is the lowest valuation among peers in HKEx. We maintain our “Accumulate” rating.

Risk

Fuel and material cost up greatly.

Deterioration of automobile demand led by further crisis

Popularity of new models launched by the joint ventures

The non-controllable factors impact through supply chain.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()