-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

A-Share Research Report

The articles are produced in Chinese only.

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Tuopu Group (601689.CH) - Steady Growth in the Core Automotive Business, with Robotics and Liquid Cooling a New Growth Curve

Friday, May 29, 2026  8412

8412

Tuopu Group(601689)

| Recommendation | Accumulate (Maintain) |

| Price on Recommendation Date | $65.820 |

| Target Price | $76.200 |

Company Profile

Tuopu Group is an industry leader in the field of automotive NVH that is capable of synchronous design with the original equipment manufacturer. In recent years, on the basis of the original business of shock absorbers and interior functional parts, the Company has proactively arranged the module of the lightweight chassis system and the automotive electronics business as the future Ŗ+3" strategic development projects, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles.

Investment Summary

A Period of Strategic Investment, with Short-Term Pressure on Profits

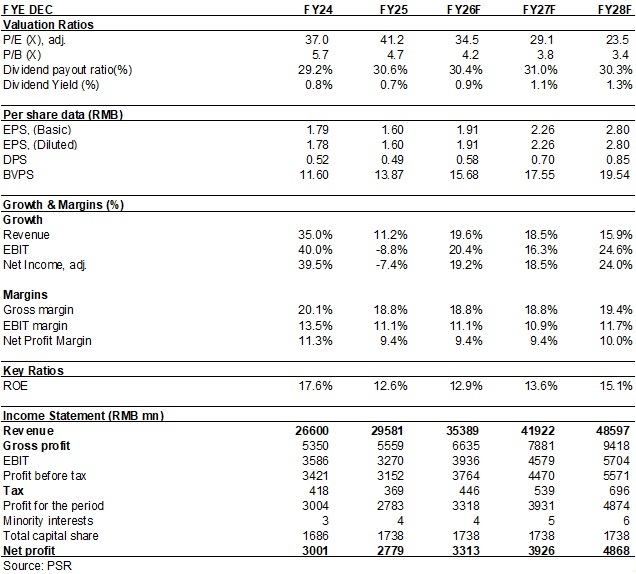

In 2025, Tuopu Group reported total revenue of RMB29.581 billion (RMB, the same below), up 11.21% year on year, showing a steady growth trend; net profit attributable to the parent company was RMB2.779 billion, down 7.38% yoy, and net profit attributable to the parent company after deducting non-recurring gains and losses was RMB2.611 billion, down 4.30% yoy. Revenue growth was mainly driven by the deepening of the company's "Tier 0.5" cooperation model and the realization of its platform-based strategy. The platform-based deployment of its nine major product lines generated a synergistic growth effect, and the supporting value per vehicle continued to increase. Combined with sales growth from core customers, this drove revenue scale to a new record high. However, due to cost pressure during the period of strategic investment and sales fluctuations among some customers, profits came under short-term pressure.

By quarter, Q1/Q2/Q3/Q4 operating revenue reached RMB5.768/7.167/7.994/8.653 billion, respectively (YoY +1.40%/+9.69%/+12.11%/+19.38%), with the growth rate rising steadily quarter by quarter; net profit attributable to the parent company for each quarter was RMB565/729/672/813 million, respectively (YoY -12.39%/-10.04/-13.65%/+6.0%), showing a trend of initial decline followed by improvement.

In the first quarter of 2026, the company reported operating revenue of RMB6.628 billion, up 14.92% year-on-year, continuing its steady low-double-digit growth. This was mainly driven by the Tier0.5 cooperation model gaining broad recognition from domestic and overseas customers, the continuous expansion of the customer base, stronger synergies among the nine major product series, and the orderly advancement of overseas production bases. However, net profit attributable to the parent company declined 2.4% year-on-year to RMB552 million, mainly due to the impact of exchange losses and rising raw material prices, as well as relatively high fixed costs during the ramp-up period of newly established overseas capacity.

Due to the reasons mentioned above, the company's gross profit margin in 2025 and the first quarter of 2026 was 19.43% and 19.26%, respectively (YoY -1.37/-0.63 pcts), and the net profit margin was 9.41% and 8.35%, respectively (YoY -1.88/-1.46 pcts), reflecting that profitability during the strategic transformation period was challenged by overseas expansion and the price war in the automotive market in terms of cost control.

In terms of expenses, the company's sales/administrative/R&D/financial expense ratios in 2025 were 0.94%/2.60%/5.06%/0.37%, respectively, representing year-on-year changes of -0.09/+0.27/+0.46/-0.25 pcts, respectively. The increase in the administrative expense ratio was mainly due to an increase in the number of management personnel, higher compensation, and increased depreciation and amortization. The increase in the R&D expense ratio was due to the company's continued increase in forward-looking R&D investment, mainly used for cutting-edge technologies such as intelligent driving, robotics, and liquid cooling.

In Q1 2026, the sales/management/R&D/financial expense ratios were 0.97%/3.14%/5.54%/1.45%, respectively, representing yoy changes of -0.22/-0.16/-0.39/+1.35 pcts, respectively. The increase in the financial expense ratio was mainly due to exchange losses caused by exchange rate fluctuations.

Steady Growth in the Core Automotive Business, with Robotics and Liquid Cooling Launching a New Dual-Engine-Driven Growth Curve

In the domestic market, the company's cooperation with automakers such as SERES, Xiaomi, Geely, BYD, Chery, Li Auto, NIO, Great Wall, and XPeng continues to expand, with order volume steadily increasing and the supporting amount per vehicle reaching approximately RMB30,000. In the international market, the company has also carried out comprehensive cooperation in the new energy vehicle sector with innovative U.S. automaker Client A, RIVIAN, and automakers such as FORD, GM, STELLANTIS, BMW, and MERCEDES-BENZ.

By business segment, in 2025, the interior/chassis/rubber vibration damping/automotive electronics/thermal management/robot actuator businesses achieved revenue of RMB9.67/8.72/4.26/2.77/2.09/0.01 billion, respectively, up +14.7%/+6.3%/-3.3%/+52.1%/-2.3%/+1.2% year-on-year, respectively.

(1) In terms of interiors, the successive mass production of the company's high-value-added intelligent surface and healthy cockpit system projects has laid a solid foundation for the transformation of the interiors business from functional components to systematization and intelligence;

(2) The large-scale mass production of air suspension products has supported the steady growth of the chassis business. Air suspension production capacity is accelerating expansion and will increase to approximately 1,500 thousand units by 2026;

(3) The automotive electronics business achieved impressive growth, mainly benefiting from the continued volume ramp-up of IBS intelligent braking products and the scaled mass production of intelligent cockpits.

(4) The company applies thermal management technologies and products in industries such as liquid-cooled servers, energy storage, and robotics. It has developed products such as liquid cooling pumps and liquid cooling cold plates, and is actively engaging with overseas Client A, NVIDIA, META, and other customers. It has secured the first batch of orders totalling RMB1.5 billion.

(5) The company's core components, such as robot rotary actuators and dexterous hand motors, have completed multiple rounds of sample delivery, and have expanded horizontally to robot body structural parts, sensors, foot shock absorbers, and electronic flexible skin. It currently has four robot actuator system production lines, and plans to establish new factories related to actuator and dexterous hand motor module deployment, with a planned production capacity of 300 thousand sets. Construction is expected to be completed in 2026, and production is expected to begin in 2027.

Based on the situation of newly received orders and combined with judgments on the future penetration rate of new energy vehicles, the company continues to advance the implementation of its globalization strategy and increase its global production capacity scale: Hangzhou Bay Phase IX and Phase X have completed construction, the Thailand plant will be completed and put into operation in the first half of 2026, and Mexico Phase II and Poland Phase II are under planning to further increase production scale.

Planning to Issue and List Hong Kong Stocks, Accelerating Global Expansion

The company is planning a Hong Kong stock listing, aiming to raise approximately USD1 billion (about HK$7.8 billion), to support two core strategic directions: global capacity expansion and mass production of humanoid robot actuators. The goal is to establish overseas production bases in Thailand, Mexico, and other locations, in order to respond to downstream customers' "going global" needs, achieve localized delivery, avoid geopolitical risks, and seize the first-mover advantage in the trillion-yuan robot components track. We believe that a Hong Kong stock listing is a key step for Tuopu to leap from a "China leader" to a "global giant", helping it transform from a "Chinese supplier" into a "globally localized partner", thereby securing more global nominated projects.

Investment Thesis

As the Mexico and Thailand factories gradually reach full production capacity in 2026, economies of scale are expected to dilute fixed costs, and profit margins are likely to see a marginal recovery. In the long term, the company's strategic positioning in humanoid robots and liquid cooling has entered the eve of commercialization. If it can achieve large-scale mass production in 2026–2027, it will completely raise the valuation ceiling, enabling its re-rating from a traditional auto parts stock to an emerging technology growth stock. At the same time, investors also need to pay attention to the impact of overseas geopolitical risks on capacity expansion, as well as the risk that the commercialization progress of the robotics business falls short of expectations.

Overall, we believe the Company possesses sustainable growth capability. We expect the EPS for 2026/2027/2028 to be 1.91/2.26/2.80yuan. So, we revise the Company's target price to RMB 76.2 yuan, respectively 40/34/27x P/E for 2026/2027/2028, a "Accumulate" rating. (Closing price as at 28 May)

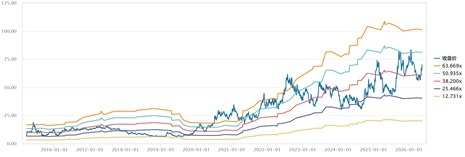

Source: Wind, Phillip Securities Hong Kong Research

Financials

(Closing price as at 28 May)

Risk

Price war among peers

Raw material price increase

New business risk

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()