-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

SOHO CHINA (410.HK) - At the Key Phase of Business Transformation

Wednesday, August 26, 2015  3940

3940

SOHO CHINA(410)

| Recommendation | Neutral |

| Price on Recommendation Date | $3.300 |

| Target Price | $3.500 |

Weekly Special - 2333 Great Wall Motor

Summary

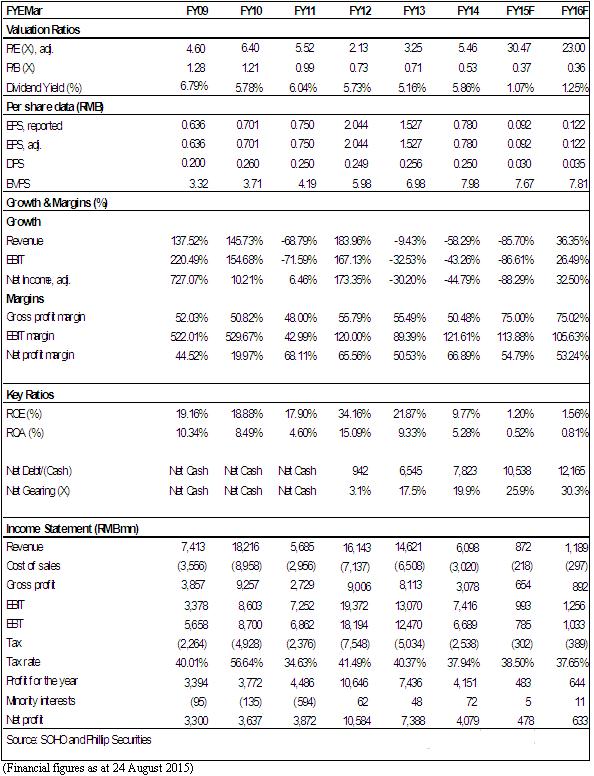

-Realized revenue of SOHO China dropped by 92% yoy to RMB393 million while realized core profit fell by 94% yoy to around RMB72 million. The sharp deterioration in income statement of the company was directly related to its change in business model. During the period, gross profit margin jumped by 25%-point yoy to 75%, reflecting that gross margin of the property leasing business is significantly higher than that of property sales business.

-Rental income of SOHO China for the period jumped by 164% to RMB439 million. The remarkable increase in rental income was mainly attributable to the rental contribution from new projects, such as SOHO Tower 3, which were completed in the second half of 2014. SOHO China now has 6 completed projects for leasing, with total leasable GFA of 522,100 sq. m. The average occupancy rate was around 73%.

-In January 2015, SOHO China launched its first online product, SOHO3Q, which is an “online + office space leasing” product. Its key features include online leasing, flexible lease terms and the creation of a communitized platform for exchange. By the end of July 2015, 5 SOHO3Q centers were established with over 3,000 seats in place.

-Can SOHO China become the Chinese version of WeWork? This will depend on whether SOHO3Q can transform from the current asset-intensive operating to the economy sharing model that is adopted by venture companies like Uber and Airbnb. The Economy Sharing + Asset-Light model is the major reason for the high valuation given by investors to WeWork. Of course, we believe that even the valuation of SOHO3Q is not as high as WeWork, it is still expected to be an important product for SOHO China during its business transformation, and will be the key driver of its earnings and valuation.

-By the end of June 2015, cash and cash equivalents and deposits of SOHO China amounted to RMB9.77 billion. Its net debt was RMB10.2 billion and its net gearing ratio increased by 6%-point from 2014. With the transition of its business model, SOHO China will see the trend of decreasing cash and cash equivalents as well as higher net gearing ratio. We believe that this situation will last to 2017, until the scale of its property leasing business will be grown to a meaningful level and its occupancy rate can be sustained at a higher level. Overall speaking, while the safety margin of its financial position decreases, we believe the balance sheet of SOHO China will remain intact.

-For the first time, SOHO China did not record any contribution from property sales in its income statement. Investors already expected a plummet in its earnings during its 2015 interim result. The sharp increase in the contribution from rental income was positive to the company but the sustainability of growth will be under pressure amid slower economic growth. With its new business model of “online + office space leasing”, SOHO3Q will become a key growth driver of SOHO China's earnings valuation. We expect during the important transition period of its business transformation, there is low visibility of the impact from the exit from the old business and the expansion of the new business on the fundamentals of company. We recommend a Neutral rating, with a 12-month target price of HKD3.5. (Closing price as at 24, August, 2015)

Financials

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()