-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李曉然小姐(Margaret Li)

分析師

分析師

本科主修市場行銷和英語,並於香港浸會大學獲得經濟學碩士學位。現為輝立証券持牌分析師,主要負責能源和公用事業等板塊的研究。曾在大型銀行、券商和資產管理公司工作,對於期貨和大宗商品衍生品領域擁有銷售、研究分析和市場推廣等工作經驗。

Margaret, a holder of a Bachelor`s degree in Marketing and English and a Master`s degree in Applied Economics from Hong Kong Baptist University, is currently employed as a licensed analyst at Phillip Securities. She specializes in conducting research focusing on the energy and utilities sectors. Prior to her current position, Margaret gained valuable work experience in a large bank, securities firm, and asset management companies. Her expertise lies in sales, research analysis, and marketing within the fields of futures and commodities derivatives.

| Phone: | 22776535 | Email: | margaretli@phillip.com.hk | |

MINISO (9896.HK) - Better-than-expected Jan-Feb same-store growth may drive a full-year Davis double play

Friday, March 27, 2026  505

505

MINISO(9896)

| Recommendation | Buy |

| Price on Recommendation Date | $32.240 |

| Target Price | $39.200 |

Weekly Special - 2333 Great Wall Motor

Company Overview

MINISO is a global self-owned brand integrated retailer featuring IP design, mainly engaged in lifestyle home products and trendy toy cultural creations. Its core businesses include MINISO (value-for-money lifestyle products) and TOP TOY (trendy toys). Adopting an “IP collaboration + high cost-performance” model, the Company sells through a global store network covering toys, beauty, and lifestyle products. Since opening its first store in 2013, the Company has built a retail network spanning 112 countries and regions worldwide, with more than 7,700 stores globally and over 100 million cumulative registered members. Leveraging the dual-brand matrix of MINISO and TOP TOY, the Company has achieved multi-format synergies and built significant global channel advantages and user-base barriers.

Figure 1: MINISO Store

Resources: Company Website, Phillip Securities

Figure 2: TOP TOY Store

Resources: Company Website, Phillip Securities

Highly concentrated ownership with sound governance

MINISO’s largest shareholder, Mini Investment Limited, holds 26.24%, while YYY MC Limited and YGF MC Limited hold 20.61% and 16.25%, respectively. The actual controllers are founder Ye Guofu and his wife Yang Yun, forming a stable concerted action relationship. The top ten shareholders together hold more than 80%. Overall, this forms a stable structure centered on Ye Guofu, with concerted parties controlling more than 60% of voting rights, providing strong support for the continuity of the Company’s long-term strategy and governance stability.

Figure 3: Shareholding Structure

Resources: WIND, Phillip Securities

Industry Analysis

Lifestyle home products broadly refer to various consumer-facing household and daily-use products, covering personal care, bags and accessories, small consumer electronics, digital accessories, stationery and cultural products, leisure snacks, daily necessities, home textiles, toys, and other subcategories. According to data from Huajing Industry Research Institute, the global household goods market grew from US$655.079 billion in 2017 to US$779.094 billion in 2023, representing a CAGR of about 2.9%. As the global economy recovers, incomes rise, and consumption frequency increases, demand for household goods is expected to maintain steady growth. Guangdong Toy Association estimates that China’s traditional toy market reached about RMB80.13 billion in 2025, up about 3.5% year-on-year, while China’s trendy toy market reached about RMB87.97 billion, up 21% year-on-year, far outpacing traditional toys. TOP TOY is accelerating overseas expansion and in March 2025 announced a globalization strategy targeting entry into core business districts in 100 countries and more than 1,000 stores over the next five years, potentially forming the Company’s second growth curve.

Revenue up over 26%, Jan-Feb same-store GMV beat expectations

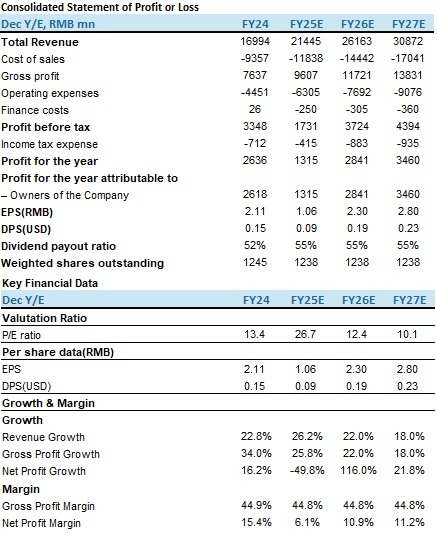

The Company expects FY2025 revenue of about RMB21.44 billion, up 26% year-on-year; operating profit of about RMB3.30-3.305 billion; and adjusted operating profit of about RMB3.665-3.675 billion, mainly benefiting from product mix optimization, stronger branding, and channel expansion. Net profit is expected at about RMB1.32-1.33 billion, with the decline mainly due to: 1) about RMB740 million share of loss from Yonghui investment; 2) about RMB400 million combined impact from TOP TOY share-based compensation and fair value changes in preferred shares; and 3) about RMB190 million interest expense on stock-linked securities, of which RMB170 million is non-cash. Excluding these non-operating items, adjusted net profit is about RMB2.89-2.90 billion, up 6.2%-6.6% year-on-year.

Operational momentum remained strong. In Jan-Feb 2026, domestic MINISO GMV rose over 25% year-on-year, with same-store GMV recording high-single-digit growth; U.S. market GMV rose over 50% year-on-year, with same-store GMV up over 20%; and overseas market management efficiency improved significantly. We believe these data show that the Company’s IP strategy, channel optimization, and globalization capabilities are accelerating into tangible operating results, laying a solid foundation for long-term value growth.

TOP TOY spin-off approaching, RMB10bn valuation anchors value realization

The TOP TOY spin-off is approaching. In the first three quarters of 2025, TOP TOY store count reached 307, up 31% year-on-year, and revenue reached RMB1.317 billion, up 88% year-on-year. After completing Temasek strategic financing last year, its valuation has been anchored at RMB10 billion. We believe that if TOP TOY is successfully spun off while remaining a non-wholly-owned subsidiary of MINISO, it may bring multi-dimensional re-rating to the parent company through valuation premium, strategic focus, and capital-market catalysts, marking the formal value realization stage of MINISO’s “second growth curve.”

Valuation and investment recommendation

In January-February 2026, total retail sales of consumer goods reached RMB8,607.9 billion, up 2.8% year-on-year, 1.9 percentage points faster than in December last year. On a month-on-month basis, February total retail sales of consumer goods rose 0.81%. We believe MINISO is poised to become a global leading IP-driven retail platform. As its IP matrix continues to improve and globalization deepens, brand value and market share are expected to rise further. We forecast revenue of RMB21.445 billion, RMB26.163 billion, and RMB30.872 billion in 2025-2027, with EPS of RMB1.06/2.3/2.8 and corresponding P/E of 26.7x/12.4x/10.1x. We assign a target price of HK$39.2, corresponding to 15x 2026E P/E, and maintain a Buy rating. (Current price as of 25 Mar)

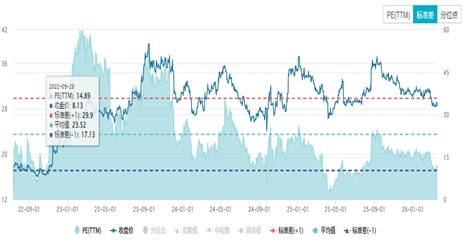

Figure 4: PE Curve

Resources: WIND, Phillip Securities

Risks

Consumption recovery falls short of expectations; intensifying industry competition and severe IP homogenization; overseas expansion risk and trade policy volatility; IP life-cycle management risk.

Financial Data

(As of 25 Mar 2026)

Exchange Rate: HKD/RMB = 0.88

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()