-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

Trip.com Group (9961.HK) - The inbound tourism market has shown significant growth momentum with policy support

Thursday, October 2, 2025  1670

1670

TRIP.COM-S(9961)

| Recommendation | Neutral |

| Price on Recommendation Date | $598.000 |

| Target Price | $610.000 |

Weekly Special - 3750 CATL

Financial performance

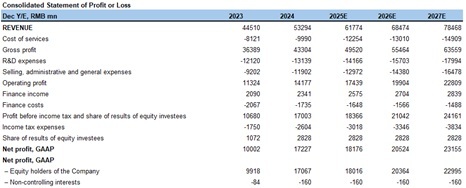

In the second quarter of 2025, the company achieved total revenue of RMB 149 billion, a year-on-year increase of 16.2%, primarily driven by strong travel demand. In terms of profitability, net profit reached RMB 49 billion, up 25.5% year-on-year, with a corresponding net profit margin of 32.9%, an increase of 2 percentage points compared to the same period last year.

By segment revenue, accommodation reservation revenue amounted to RMB 62 billion, a year-on-year increase of 21.2%, mainly due to strong growth in domestic and outbound hotel businesses. Transportation ticketing revenue reached RMB 54 billion, up 10.8% year-on-year, driven primarily by outbound and international ticketing. Tourism vacation revenue totaled RMB 11 billion, a year-on-year increase of 5.3%, mainly attributed to heightened travel demand during holidays. Business travel management revenue was RMB 7 billion, up 9.3% year-on-year, largely due to increased demand for corporate travel management services.

In terms of expenses, the company's total operating expenses for the quarter were RMB 79 billion, a year-on-year increase of 14.7%, which is generally in line with the fluctuations in total revenue during the period. The company's R&D expense ratio, sales expense ratio, and administrative expense ratio for 2Q25 were 23.6%, 22.4%, and 7.4%, respectively, representing year-on-year changes of +0.1 pct, +0.2 pct, and -1.0 pct. The company continues to intensify its efforts in international business expansion and promotion.

Performance Summary

Inbound tourism market demonstrated significant growth, driven by supportive policies

In the first half of the year, the number of inbound visitors in China increased by approximately 30% year-on-year, while the booking volume for inbound travel on the Ctrip platform surged by over 100% year-on-year. With further relaxation of visa policies, the continuous enhancement of China's tourism appeal, and the improvement of related service systems, inbound tourism is expected to consistently contribute to the growth of domestic business.

Meanwhile, the structure of domestic travel demand is also evolving. According to management, the "silver-haired generation" is emerging as a key growth driver. As of the second quarter of 2025, both the user base and gross merchandise volume of the "Friends of Seniors" program have more than doubled compared to the end of 2024. At the same time, younger travelers are showing a stronger preference for integrated "entertainment + tourism" experiences, such as music festivals, themed tours, and immersive destination activities. In the second quarter of 2025, revenue from such businesses grew by over 100% year-on-year, indicating that younger users' travel consumption is rapidly shifting toward experiential and themed offerings.

International business maintains rapid growth, with user acquisition efficiency exceeding expectations

In the second quarter of 2025, overall cross-border flight capacity in the industry recovered to 84% of pre-pandemic levels. The company's outbound hotel and flight booking volumes have fully surpassed 120% of the same period in 2019, consistently outperforming the industry by 30-40 percentage points.

Entering the summer season, as capacity further recovers, airfare prices have decreased year-on-year but remain higher than pre-pandemic levels. Hotel prices, on the other hand, have remained stable. It is anticipated that outbound travel revenue will continue to achieve relatively fast year-on-year growth in the third quarter. Meanwhile, total bookings on the Trip.com platform grew by over 60% year-on-year in the second quarter. The Asia-Pacific region remains the focal point of business, while emerging markets such as the Middle East have also demonstrated strong growth momentum.

Investment thesis

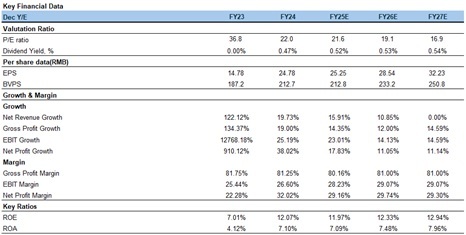

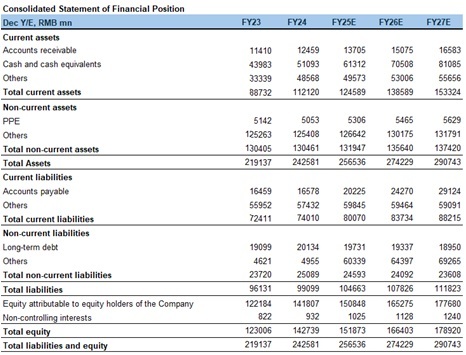

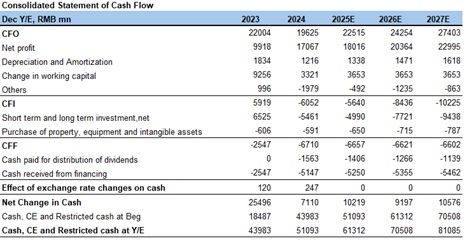

We forecast the company's operating revenue for 2025-2027 to be RMB 61.8/68.5/78.5 billion, with net profit attributable to shareholders of RMB 18.0/20.4/23.0 billion. The corresponding diluted EPS is projected to be RMB 25/29/32, and the current stock price implies a P/E ratio of 21.6x/19.1x/16.9x. We have selected domestic and international OTA companies—Booking, Expedia, Airbnb, and Tongcheng Travel—as comparable firms. Applying a 22x P/E multiple based on the 2025 forecast, we have accordingly raised our target price to HKD 610 and maintain a "Neutral" rating.

Risk factors

1) Domestic consumption demand is weaker than expected;

2) International business expansion is slower than anticipated;

3) Hotel ADR and airfare pricing pressures are greater than expected.

Financials

(Current Price as of: Sep 29 2025)

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()