-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CATL (3750.HK) - Accelerate global production capacity building and continuously launch innovative products

Friday, September 26, 2025  2763

2763

CATL(3750)

| Recommendation | Accumulate (maintain) |

| Price on Recommendation Date | $501.500 |

| Target Price | $566.000 |

Weekly Special - 1318 MAO GEPING

Company Profile

Contemporary Amperex Technology Co., Limited ("CATL") is a global leader in the supply of power battery systems, focusing on the research and development, production, and sales of power battery systems and energy storage systems for new energy vehicles. Its main businesses include power battery systems, energy storage systems, and lithium battery material systems (mainly ternary precursors). Specifically, the power battery system comprises cells, modules, and battery packs, which are used in electric passenger vehicles, commercial vehicles, and other applications. In addition, CATL has entered the field of battery recycling through the acquisition of Brunp Recycling and invested in and held stakes in overseas lithium mines to secure ties with raw material suppliers, thereby achieving a closed-loop layout of the upstream and downstream industry chain.

Investment Summary

A Global Leader in the Supply of Power Battery Systems

CATL is a global leading innovative technology company in new energy. Founded in 2011, the company is mainly engaged in the R&D, production, and sales of power batteries and energy storage batteries. In addition, the company has realised a closed-loop layout of the upstream and downstream industry chain through investing in, constructing, and operating battery materials and recycling, as well as battery mineral resources. As of 30 June 2025, the company had established six major research and development centres and thirteen major battery production bases worldwide (including eleven in China and two in Germany and Hungary, respectively). Its service network covers 64 countries and regions. On average, one in every three new energy vehicles worldwide is equipped with CATL batteries, and its energy storage batteries have been applied in over 1,700 projects globally. In 2024, the company ranked first in global power battery installations for the eighth consecutive year with a market share of 37.9%, and also ranked first for the fourth consecutive year in energy storage batteries with a market share of 36.5%.

Stable Shareholding Structure, Management with Strong Technical Background, and Equity Incentives Binding Core Talents

As of the first half of 2025, the company's actual controller and founder, Dr. Robin Zeng, held 100% equity in Xiamen Ruiting Investment through direct and indirect shareholding, while Xiamen Ruiting Investment held 22.47% of CATL's total shares, making it the largest shareholder. CATL's co-founder and former Vice Chairman, Huang Shilin, held 10.22%, while Vice Chairman Li Ping held 4.42%. Founding shareholders in total held approximately 43% of the company's shares, reflecting a relatively concentrated ownership. Hong Kong Securities Clearing Company ("HKSCC") was the second-largest shareholder, holding 13.31%.

The company's founder and Chairman, Dr. Robin Zeng, holds a PhD from the Institute of Physics of the Chinese Academy of Sciences. He founded ATL and CATL successively, with profound theoretical knowledge and extensive practical experience in the lithium battery industry.

The company launched multiple rounds of equity incentives in 2015, 2018, 2019, 2020, 2021, 2022, and 2023, deeply binding employees' interests with the company. This has been particularly conducive to stimulating employees' creativity and enthusiasm in the fast-iterating battery technology field.

Strong Competitive Advantages Forging a ~RMB400 Billion Lithium Battery Empire

The company has been deeply engaged in the lithium battery industry for many years and has established full-chain independent and efficient R&D capabilities. It holds core technological advantages and a forward-looking R&D layout in battery materials, battery systems, and battery recycling, covering the world's most extensive customer base of power and energy storage applications. Through continuous technological innovation, industry chain integration, and global market expansion, the company has gradually established its core position in the new energy vehicle industry chain.

R&D

The company attaches great importance to R&D, with six major R&D centres and more than 21 thousand R&D personnel. R&D expenditure increased from RMB1,991 million in 2018 to RMB18,607 million in 2024 (RMB, the same below), and was fully expensed, with the R&D expense ratio maintained at around 5%. As of 30 June 2025, the company held a total of 49,347 patents and patent applications, consisting of 29,709 domestic and 19,638 overseas ones. The company owns a provincial-level key laboratory for lithium-ion batteries and a CNAS-certified testing and validation centre, and has participated in the formulation of multiple national and industry standards. Also, it has undertaken several national-level projects, such as the ൔth Five-Year Plan" National New Energy Vehicle Industry Technology Innovation Project and the ൕth Five-Year Plan" National Key R&D Programme for New Energy Vehicles.

Technology

In terms of core technological competitiveness, since its establishment, the company has successively launched products such as large-format cells for commercial vehicles, high-nickel ternary batteries, and module-free CTP (cell-to-pack) design, all of which have achieved large-scale commercial applications. It has also taken the lead in introducing innovative products such as high-energy-density sodium-ion batteries, M3P batteries, and condensed matter batteries, thereby forming the most comprehensive and advanced product portfolio in the industry. These products are widely applied in passenger vehicles, commercial vehicles, as well as energy storage and emerging scenarios, with advantages including high energy density, long cycle life, high charge rate, wide temperature adaptability, and high safety.

For example, CATL's Shenxing Pro Ultra-fast Charging Edition battery is the world's first product to adopt lithium iron phosphate ("LFP") material and achieve 4C ultra-fast charging. It supports a peak charging rate of 12C, enabling an additional driving range of 478 kilometres (under WLTP conditions) in just 10 minutes, or a charge from 10% to 80% within 20 minutes, while maintaining efficient charging capability even at low temperatures of -20°C in Europe.

The Kirin Battery adopts third-generation CTP technology, integrating high-nickel ternary or other chemical system cells. Its energy density can reach up to 255 Wh/kg, with ultra-fast charging capability up to 5C. It features high energy density, excellent fast-charging performance, and enhanced safety, allowing a vehicle range of over 1,000 kilometres. The company claims it can achieve "zero thermal runaway" for ternary lithium batteries. If this technology is validated on a large scale, it will significantly enhance the acceptance of ternary lithium batteries in the commercial vehicle segment.

Clients

In terms of customer engagement, CATL has established long-term partnerships with many internationally renowned automakers and expanded its influence in Europe, the United States, and other emerging markets through technology licensing and overseas capacity expansion. The company's customers cover nine of the world's top ten new energy vehicle manufacturers, including BMW, Mercedes-Benz, Stellantis, Volkswagen, Ford, Toyota, Hyundai, Honda, Volvo, SAIC, Geely, NIO, Li Auto, Yutong, Xiaomi, and others. Its energy storage customers and partners include NextEra, Synergy, Wärtsilä, Excelsior, Jupiter Power, Flexgen, China Energy, SPIC, China Huaneng, China Huadian, and PetroChina.

Capacity and Supply Chain

On capacity expansion, the company's annual battery capacity increased from 53 GWh in 2019 to 676 GWh in 2024, representing a compound annual growth rate of 66.4%, higher than the 59.3% CAGR of China's new energy vehicle sales during the same period. In the first half of 2025, CATL had a total capacity of 345 GWh and an output of 310 GWh, with a utilisation rate of 89.86%. The high utilisation rate reflects the positive effects of production efficiency and economies of scale. The company also had 235 GWh of capacity under construction, and expects to reach 900 GWh by the end of 2025.

In addition, the company has effectively mitigated risks of raw material price fluctuations and technology upgrade uncertainties through long-term agreements with suppliers and foreign exchange hedging. For example, CATL prepaid for cathode material purchases from Jiangxi Shenghua, a subsidiary of Fulin Precision, securing no less than 80% of its capacity from 2025 to 2029, thereby substantially enhancing the supply guarantee for lithium iron phosphate cathode materials.

Market Share

Through technological iteration, capacity expansion, and customer binding, CATL has further consolidated its leading position in the power battery industry, while also demonstrating strong technological strength and market influence in energy storage systems, battery materials, and recycling.

According to SNE Research, from January to May 2025, CATL's global market share in power batteries reached 38.1%, an increase of 0.6 percentage points compared with the same period last year. In the domestic market, the company maintained a leading market share of between 42% and 45%. In the European market, its share rose by 5 percentage points to 43%. Meanwhile, CATL's energy storage business continued to expand globally, with the company remaining the world's largest producer of energy storage batteries from January to June 2025.

Profitability Further Improved in Mid-2025, Market Share Remained Stable

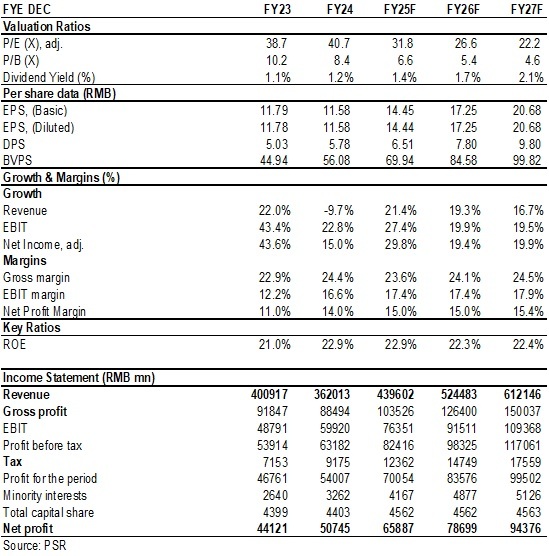

According to the latest financial report, CATL achieved revenue of RMB178,886 million in the first half of 2025, representing a year-on-year growth of 7.27%, of which overseas revenue was RMB61,208 million, accounting for 34.22% of total revenue. Net profit attributable to shareholders was RMB30,485 million, a year-on-year increase of 33.33%. Net profit excluding non-recurring items attributable to shareholders was RMB27,197 million, a year-on-year increase of 35.62%. EPS was RMB6.92. The company distributed a cash dividend of RMB1.007 per share to all shareholders, equivalent to a payout ratio of 15%.

The gross margin was 25.0%, down 1.51 percentage points year-on-year. Under the new accounting standards, warranty provisions were reclassified from expenses to costs, which reduced the sales expense ratio while slightly lowering the gross margin. In addition, due to fluctuations in lithium carbonate and other raw material prices, the unit selling price of the company's products declined slightly.

The net margin was 18.1%, an increase of 3.17 percentage points year-on-year, reaching a new high since 2018, mainly benefiting from high-capacity utilisation, improved localisation and yield rate, economies of scale, optimised product mix, increased foreign exchange gains, and higher overseas contributions.

Breaking down by quarter, in Q1/Q2 2025, the company achieved revenue of RMB84,705 million/RMB94,182 million, representing year-on-year growth of 6.2%/8.26%, and net profit attributable to shareholders of RMB13,963 million/RMB16,523 million, representing year-on-year growth of 32.9%/33.73%.

Breaking down by business segment, power battery revenue was RMB131.57 billion, up 16.80% year-on-year, with strong performance in overseas markets, especially Europe. Segment gross margin was 22.41%, down 1.07 percentage points year-on-year. Energy storage battery revenue was RMB28.4 billion, down 1.47% year-on-year, mainly affected by tariffs, and segment gross margin was 25.52%, up 1.11 percentage points. Revenue on battery materials and recycling was RMB7,887 million, down 44.97% year-on-year, and segment gross margin was 26.42%, up 18.21 percentage points. Battery mineral resources revenue was RMB3,361 million, up 27.86% year-on-year, and segment gross margin was 9.07%, up 1.26 percentage points. Other businesses generated revenue of RMB7,665 million, down 8.0% year-on-year. Segment gross margin was 73.6%, up 22.6 percentage points.

The company's asset-liability ratio continued to decline, standing at 62.59% in the first half of 2025, significantly improving from 69.26% in the same period of 2024. Cash flow remained strong, with net operating cash flow of RMB58,687 million, up 31.26% year-on-year.

Accelerating Global Capacity Construction, Continuously Launching Innovative Products to Strengthen Competitive Advantages

In terms of power batteries, the company has established production bases in Germany, Hungary, and other countries, and plans to add 50 GWh of capacity in Spain. Benefiting from the rapid expansion of the European new energy vehicle market, the growth of CATL's overseas business will provide it with new profit sources. In terms of energy storage, CATL has extended downstream into system integration, with projects in the Middle East and Australia contributing considerable profitability. With the rise of new application scenarios such as AI data centres and 5G base stations, demand for energy storage will continue to grow.

CATL continues to push forward in solid-state batteries, sodium-ion batteries, and all-climate batteries. In the first half of the year, it launched the second-generation Shenxing Ultra-fast Charging Battery, the Xiaoyao Dual-core Battery, and the new-generation sodium-ion battery. In the energy storage field, the company announced the mass production and delivery of 587 Ah large-capacity energy storage cells, as well as released the world's first mass-producible 9 MWh ultra-large-capacity energy storage system solution, TENERStack. In solid-state battery development, the company has built a leading technical team and increased investment, with most scientific challenges already resolved. It expects to achieve mass production of solid-state batteries before 2028. These technological breakthroughs will help the company address future market demand changes, and further consolidate its competitive advantages and industry-leading position.

Investment Thesis

In the long term, the boom in electric vehicles, especially in Europe and China, is expected to continue. The prospects for innovative businesses are immense, and the advantages of leading enterprises will become even more prominent. The "strong get stronger" pattern is expected to sustain.

As for valuation, we expected diluted EPS of the Company to RMB 14.45/17.25/20.68 for 2025/2026/2027. And we accordingly gave the target price to HKD 566, respectively 36/30/25x P/E for 2025/2026/2027. "Accumulate" rating.

Risk

1) Technical Iteration Risks;

2) Raw material price fluctuation risk;

3) The downturn in macroeconomics affects demand for end-use products;

4) Geopolitics and Trade Policy Risks.

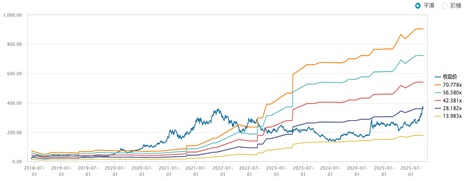

P/E Band trend for its A share

Source: Wind, Company, Phillip Securities Hong Kong Research

Financials

(Closing price as at 23 September 2025)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()