-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李曉然小姐(Margaret Li)

分析師

分析師

本科主修市場行銷和英語,並於香港浸會大學獲得經濟學碩士學位。現為輝立証券持牌分析師,主要負責能源和公用事業等板塊的研究。曾在大型銀行、券商和資產管理公司工作,對於期貨和大宗商品衍生品領域擁有銷售、研究分析和市場推廣等工作經驗。

Margaret, a holder of a Bachelor`s degree in Marketing and English and a Master`s degree in Applied Economics from Hong Kong Baptist University, is currently employed as a licensed analyst at Phillip Securities. She specializes in conducting research focusing on the energy and utilities sectors. Prior to her current position, Margaret gained valuable work experience in a large bank, securities firm, and asset management companies. Her expertise lies in sales, research analysis, and marketing within the fields of futures and commodities derivatives.

| Phone: | 22776535 | Email: | margaretli@phillip.com.hk | |

LAOPU GOLD (6181.HK) - Unfazed by gold price fluctuations, both performance and luxury status are doubly validated

Friday, April 10, 2026  7736

7736

LAOPU GOLD(6181)

| Recommendation | Buy (upgraded) |

| Price on Recommendation Date | $657.500 |

| Target Price | $815.960 |

Weekly Special - 2333 Great Wall Motor

Overview

Laopu Gold (6181.HK) is the top heritage gold jewelry brand in China. Based on data of Frost & Sullivan, Laopu Gold was the first brand in the industry to introduce diamond-inlaid pure gold jewelry, leading trends for the industry. In 2025, the company's average annualized sales per shopping mall approached nearly RMB 1 billion. According to Frost & Sullivan data, among global luxury groups operating in mainland China in 2025, the company ranked first in both sales per shopping mall and sales per unit area.

Strong performance growth was achieved in both the full year of 2025 and the first quarter of 2026

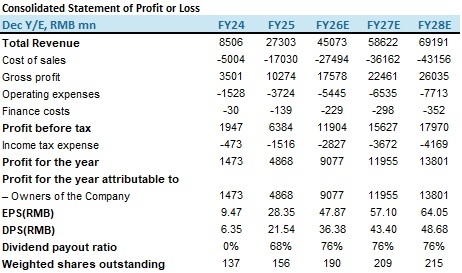

In 2025, the company's revenue reached RMB 27.30 billion, + 221% YOY. Among this, revenue from mainland China was RMB 23.36 billion, + 205.4% YOY, accounting for 85.6% of total revenue; overseas revenue was RMB 3.94 billion, + 361% YOY, accounting for 14.4% of total revenue with an increase of 4.3 pct. Laopu Gold's first overseas store officially opened in June 2025 at Marina Bay Sands Shopping Mall in Singapore, located in a high-end luxury area. In addition, Laopu Gold has three stores in Hong Kong, including a flagship store at IFC. The company plans to further expand by opening 6--9 overseas stores in 2026 and 2027, entering markets such as Japan, North America, Australia, and the Middle East, in order to further expand its international footprint. We expect the overseas revenue share to continue climbing, contributing more significantly. Gross profit was RMB 10.27 billion, + 193.4% YOY; net profit attributable to the parent company was RMB 4.87 billion, + 230.45% YOY; EPS was RMB 28.35, + 299.4% YOY. In 2025, the company paid an interim dividend of RMB 9.59 per share and a final dividend of RMB 11.95 per share, resulting in a full-year dividend payout ratio of 76%. The above growth was mainly driven by brand advantages, product update, and store expansion (10 new stores added and 9 optimized in 2025). For the first quarter of 2026, the company expects to achieve sales (revenue including tax) of approximately RMB 19.0--20.0 billion, revenue of approximately RMB 16.5--17.5 billion, and net profit of approximately RMB 3.6--3.8 billion.

As of the end of 2025, the company's total assets reached RMB 21.25 billion, + 235.4% YOY; total liabilities were RMB 10.16 billion; the asset-liability ratio stood at 47.8% with an increase of 9.5 pct YOY, mainly due to continuous store expansion and increased demand for gold raw material procurement, which drove up the scale of borrowings. Shareholders' equity was RMB 11.10 billion, + 183% YOY, reflecting a significant increase in owners' equity and further strengthening of the company's capital base. Cash and bank balances amounted to RMB 2.07 billion, + 252.3% YOY, indicating a substantial enhancement in cash reserves. Inventory was RMB 16.04 billion, covering raw materials, work in progress, and finished goods, + 292.5% YOY, primarily due to stockpiling in preparation for expected sales growth during the peak Spring Festival season. As a result, inventory turnover days extended from 195 days in the same period last year to 216 days. Accounts payable, other payables, and accrued expenses + 178.7% and 581.2% YOY respectively, reflecting the company's strong ability to occupy funds from upstream suppliers and downstream customers, highlighting its advantage in trade credit utilization, which helps free up its own funds for operating activities such as R&D investment and store expansion.

Unfazed by gold price fluctuations, Laopu's luxury status has been further consolidated

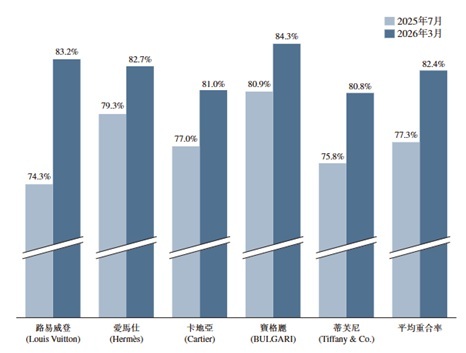

Since the beginning of 2026, intensifying geopolitical conflicts and a tightening global security situation have led to sharp fluctuations in gold price, which once fell from USD 5,500 per ounce to USD 4,500 per ounce. Against this backdrop, the company's performance in Q1 2026 rose against the trend, with net profit for the quarter exceeding 70% of its full-year 2025 net profit, demonstrating strong operational resilience. The company has been listed on the Hurun Best of the Best for four consecutive years from 2023 to 2026, and in 2026 ranked among the top three jewelry brands most favored by China's high-net-worth individuals, being the only Chinese brand on the list. According to Frost & Sullivan, in 2025 the company ranked second among global luxury brands in mainland China by revenue and was the only Chinese brand among the top five. The overlap rate of its consumers with five major international luxury brands such as LV and Hermès increased from 77.3% (July 2025) to 82.4% (March 2026), continuously validating its high-end positioning. A Rothschild report noted that Laopu Gold, with its unique positioning of "integrating ancient craftsmanship with luxury fashion," has become an industry disruptor, achieving breakthroughs that other brands have not. The institution believes that the company surpassed the China jewelry business of Richemont Group in the second half of 2025. Richemont is one of the world's three largest luxury goods groups, with its jewelry business including Cartier, Van Cleef & Arpels, and Buccellati. Laopu Gold has approximately 610,000 loyal members, a net increase of 260,000 (or 74.3%) from the end of 2024, with its consumer base continuing to expand. While gold's high value-retention attribute certainly enhances the products, Laopu Gold's core competitiveness that distinguishes it from traditional gold jewelry retailers lies in its ancient method gold craftsmanship, brand influence, and strong luxury attributes.

Figure 1: Gold price

Resources:Wind,PSHK

Figure 2: High-end brand overlap rate

Resources:Annual Report,PSHK

Investment Thesis

We believe that gold price in 2026 will show a "decline first, then rise" trend: in the first half, price will fluctuate within the range of USD 4,300--5,000 per ounce, digesting geopolitical premiums; in the second half, supported by a recovery in expectations of Fed rate cuts and continued central bank gold purchases, price will rebound to the target range of USD 5,200--5,500 per ounce. Core drivers include the evolution of the Middle East situation, the Fed's policy path, and the continued trend of central bank gold buying. Laopu Gold has carved out an independent path as an Eastern luxury brand, with low sensitivity to gold price fluctuations. In fact, higher gold price will be beneficial to its brand premium and earnings resilience.

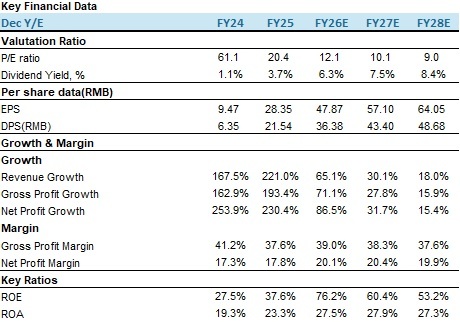

Laopu Gold's core advantage lies in its unique "cultural gold" positioning and high-growth model. Its prospects mainly depend on whether it can balance financial health and brand value amid rapid expansion. The company has built a moat in the traditional gold retail market through differentiated product positioning (Eastern aesthetics + ancient method gold) and has opened up new growth space through store upgrades and overseas expansion. We are optimistic about the company's medium-to-long-term development prospects and believe it can achieve sustainable growth while maintaining its premium brand positioning. We forecast the company's revenue for 2026--2028 to be RMB 45.07 billion, RMB 58.62 billion, and RMB 69.19 billion respectively. EPS is projected at RMB 47.87 / 57.1 / 64.05, corresponding to P/E ratios of 12.1x / 10.1x / 9.0x. Based on a target P/E of 15x for 2026, we set a target price of HKD 815.96 and upgrade the rating to "Buy". (Current price as of April 8)

Risk factors

Gold price fluctuations, intensified industry competition, macroeconomic recovery is weaker than expected, and store expansion is weaker than expected.

Financial

Current Price as of: 08 Apr

Exchange rate: HKD/CNY = 0.88

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()