-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Zenergy (3677 HK) - Lightly equipped, diverse growth

Wednesday, June 24, 2026  19864

19864

Zenergy

| Recommendation | BUY (Initiation) |

| Price on Recommendation Date | $6.050 |

| Target Price | $9.000 |

Weekly Special - 002050 Sanhua

Company profile

Jiangsu Zenergy is a leading lithium-ion battery manufacturer in China, providing integrated solutions covering battery cells, modules, battery clusters and battery management systems (BMS). The Company focuses primarily on the passenger vehicle EV battery market while expanding into all-scenario applications across land, sea and air (LISA). Its products cover EV batteries, energy storage batteries and aviation batteries. By market share, the Company ranked eighth in China's EV battery market from January to May 2026, while its ternary battery installation volume in domestic passenger vehicles rose to fifth place. The Company primarily enhances manufacturing efficiency through standardised battery cells and platform-based battery packs, optimizing quality cost control via intelligent manufacturing and lean management systems to build core competitiveness, thereby building its core competitiveness. Its customers are concentrated among leading automakers, including Leapmotor, GAC Toyota, FAW Hongqi, SAIC-GM, SAIC-GM-Wuling and Volkswagen.

Investment Summary

Strong Late-Mover Advantage; Capacity Ramp-Up Drives Rapid Earnings Growth

The Company was established in 2019 through a reorganisation led by the former core team of Fuyao Glass. It is one of the few top-ten battery manufacturers with roots in the automotive components industry, and its core management team has deep insights into production process management and cost control. The Company has a significant late-mover advantage and is well positioned to benefit from expanding battery application scenarios and rapid technological advances in the battery industry.

The Company completed its IPO and listing on HKEX in April 2025 and completed a placing in October, raising a total of approximately HK$1.4 billion. The vast majority of the proceeds was used to expand capacity at its Changshu production base. As of May 2026, the Company's capacity reached 35.5 GWh, up 39.2% from 25.5 GWh at end-2025. Capacity is expected to reach 70 GWh by end-2026 and potentially 120 GWh within the next two to three years.

The Company adopts a three-pronged operating model integrating "technology-driven development + intelligent manufacturing + customer integration". It centres on three differentiated products: an NCM-LFP blended chemistry, polyanionic sodium-ion batteries and AS9100D/CAAC dual-certified aviation battery cells. Its self-developed "Three-in-One Manufacturing" intelligent production lines---Workstation-integrated Logistics, Manufacturing-integrated Workstations and Quality-integrated Manufacturing---enable flexible, high-yield mass production. Following the implementation of the MOM system and ZOE operational excellence platform, its production-line automation rate reached 95%, while depreciation per unit was the lowest in the industry.

Benefiting from rapid capacity expansion and economies of scale beginning to take effect, the Company turned profitable for the first time in 2024, and its operations began to move onto a sound footing. In 2025, the Company reported revenue of RMB8,101 million (RMB, the same below), up 57.9% yoy, and net profit attributable to the parent company of RMB809 million, up 788.4% yoy. Its net profit margin reached 10.0%, well above the industry average, validating its "lean set-up + efficient manufacturing" investment case.

EV Battery Business Drives Earnings Surge

The Company's core business is EV batteries for new energy passenger vehicles, which accounted for more than 90% of revenue in 2025, reaching 94.8%. Its products cover all powertrain types, including BEVs, PHEVs, EREVs and HEVs, and focus on high energy density, 8C fast charging and battery cells for 800 V high-voltage platforms. They are installed in several popular models from leading automakers, including Leapmotor, FAW Hongqi, GAC Motor and Volkswagen. The Company's 400 V high-voltage ternary lithium-ion battery, with peak 5C fast charging, achieves zero thermal propagation even at a high temperature of 45°C. Its 800 V high-voltage ternary lithium-ion battery, with peak 8C ultra-fast charging, has a cell energy density of more than 240 Wh/kg. Its high-specific-energy LFP battery has a volumetric energy density of 435 Wh/L, while its fast-charging LFP battery supports 4C--8C fast charging and has an energy density of 185-190 Wh/kg.

In 2025, driven by a 66.7% yoy increase in shipment volume to 19.82 GWh, revenue from the Company's EV battery business reached RMB7,681 million, up 64.7% yoy, making it the primary driver of the surge in results. The segment's gross margin increased by 3.7 ppts to 18.9%, reflecting the benefits of economies of scale and cost optimisation. Net profit per watt-hour of batteries exceeded RMB0.02.

Looking ahead, as the number of automakers awarding project nominations to the Company increases, particularly given the significant rise in the number of battery cells per vehicle under 800 V high-voltage platform architectures, the capacity and efficiency of its new production lines are expected to move towards a faster production pace of more than 30 ppm per line and more than 60 ppm under a one-to-two configuration.

The Company is also focusing on incremental opportunities arising from the electrification of EREVs. The energy density of its next-generation LFP and NCM blended-chemistry battery is expected to exceed 215 Wh/kg. The product will be used in customers' premium C/D-segment BEV and EREV models, enhancing the Company's overall competitiveness.

Energy Storage and Aviation Batteries Open Up a Second Growth Curve

In the energy storage battery sector, the company's products are primarily used in household energy storage, industrial and commercial energy storage, independent energy storage stations, long-duration energy storage, and AIDC applications. Key clients include Deye Technology and Toyota's residential energy storage projects. Among these, the household energy storage products feature long-cycle batteries with an energy efficiency exceeding 95% and a cycle life surpassing 8,000 cycles, with the products already in mass production and delivery; Its second-generation products focus on improving low-temperature performance and support charging at temperatures as low as -10°C, primarily targeting applications in extremely cold regions and countries. Another 314 Ah energy storage battery achieves an energy conversion efficiency of 95%, a cycle life of more than 12,000 cycles and a calendar life of over 25 years, thereby reducing customers' system costs.

In 2025, constrained by limited capacity, revenue from energy storage batteries decreased by 9.9% yoy to RMB420 million, although the segment's gross margin increased by 1.4 ppts yoy. The company plans to increase the production capacity of next-generation large-capacity lithium-ion batteries for energy storage by 2026. Meanwhile, products such as the 104Ah and 314Ah models will be mass-produced and sold in the first half of 2026, while the 587Ah and 588Ah models will gradually achieve large-scale sales in the second half of the year, further enhancing the scale and market competitiveness of energy storage batteries.

For aviation batteries, the Company has made forward-looking investments in technology R&D for many years and achieved phased progress. It has launched its second-generation "Three Highs and One Fast" aviation battery, which adopts dual semi-solid-state technologies and meets ppb-level aviation safety standards. The battery has an energy density of more than 320 Wh/kg, can still deliver a 12C discharge rate at a low state of charge and supports 15-minute fast charging, meeting the requirements of frequent and diversified flight scenarios. The product entered mass production and delivery in 2025 and may also be applied in embodied-intelligence robots in the future. Aviation batteries have a significantly higher value per unit and gross margin than EV batteries, making the segment the largest source of future earnings upside.

In advanced battery technologies, the energy density of the Company's sodium-ion battery system has exceeded 170 Wh/kg. It has already been exported in small batches to EU countries for applications including PHEVs and UPS systems, and may subsequently be expanded into areas such as AIDC to meet instantaneous high-power electricity demand, offering broad development prospects. The Company's pilot production line for all-solid-state batteries will be completed in 2026, enabling the production of 100 Ah-class high-specific-energy lithium batteries and all-solid-state batteries with capacities of more than 60 Ah, marking a critical transition from "technology validation" to "large-scale profitability".

Investment Thesis & Valuation

Driven by the three growth engines of EV batteries, energy storage batteries and aviation batteries, the Company is entering a fast track of "capacity ramp-up → cost reduction → profit release".

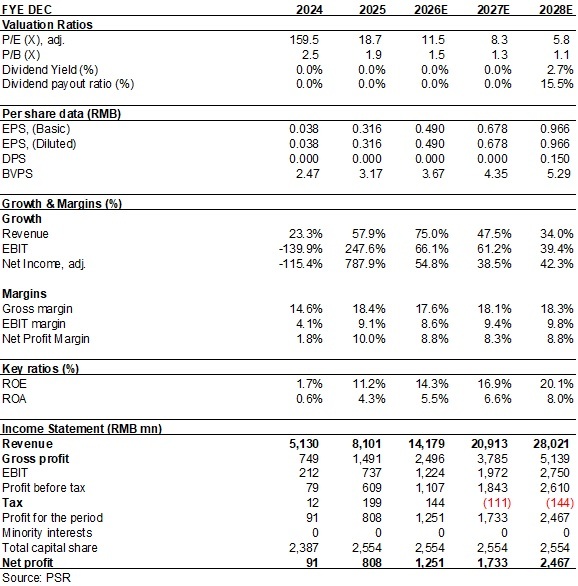

As analyzed above, we expected diluted EPS of the Company to RMB 0.49/0.68/0.97 of 2026/2027/2028. And we accordingly gave the target price to HKD9, respectively 16/11.5/8.1x P/E for 2026/2027/2028. "Buy" rating. (Closing price as at 23 June)

Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

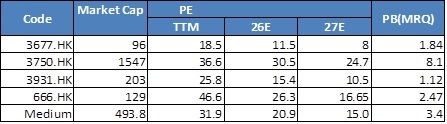

Peer Comparison

Source: Wind, Company, Phillip Securities Hong Kong Research

Financials

(Closing price as at 23 June)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()