-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Cathay Pacific (293 HK) - FY25 result beat, while soaring oil prices would weight on short-term bottom-line

Monday, March 30, 2026  36

36

Cathay Pacific(293)

| Recommendation | Accumulate (Maintain) |

| Price on Recommendation Date | $12.310 |

| Target Price | $13.600 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

Strong Recovery Momentum Continued in H2 Last Year, Profit Reached HK$7.2 Billion and Nearly Doubled HoH

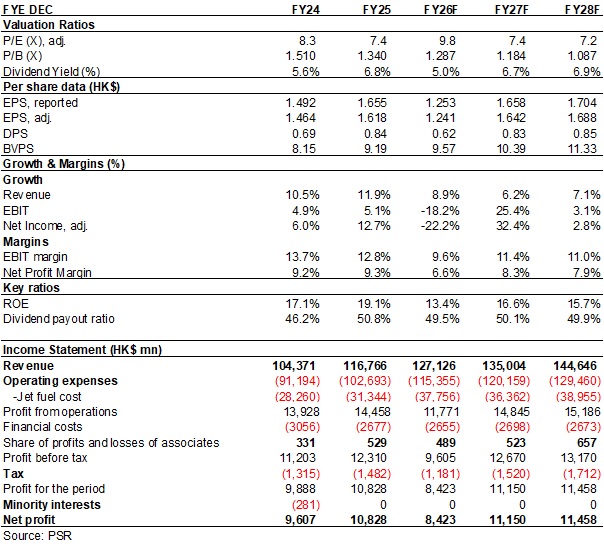

Cathay Pacific reported its 2025 results, with the Group recording total revenue of HK$116,766 million (HK$, the same below) for the full year, up 11.88% yoy; profit attributable to shareholders reached HK$10,828 million, up 9.5% yoy, marking the third consecutive year of robust profit at around HK$10 billion and validating its operating resilience. Basic EPS was HK165.5 cents, up 10.9% yoy. The result was mainly driven by increased capacity, stable passenger volumes and strong cargo demand, which supported financial growth, although part of the increase was offset by yield normalisation and losses at HK Express.

The Group announced a final dividend of HK$0.64 per share. Together with the interim dividend of HK$0.20 per share, the full-year dividend totalled HK$0.84 per share, up 21.74% yoy.

The strong momentum in H2 continued, with revenue rising 14.04% yoy to HK$62,457 million and profit attributable to shareholders increasing 15.11% yoy to HK$7,177 million, almost doubling from H1. In addition to the factors mentioned above, this was also supported by a one-off gain of HK$880 million from HAECO and a larger contribution from associates, mainly Air China and Air China Cargo. If excluding these factors, core profit attributable to shareholders in H2 would have been approximately HK$5,914 million, up 4.99% yoy and 61.98% hoh, indicating a steadily improving performance.

Fare Tailwinds Continued to Fade, Network Expansion Became the Core Driver

The Group’s passenger services revenue reached HK$78,848 million, up 15.0% yoy, with growth lagging behind the increase in passenger traffic. The Group continued to progressively expand its route network, adding 20 new destinations in 2025, bringing its passenger network to over 100 cities worldwide. During the reporting period, Cathay Pacific’s passenger capacity (available seat kilometres, ASK) increased by 25.8% yoy, passenger traffic (revenue passenger kilometres, RPK) rose by 28.9%, and total passengers carried reached 28.87 million, up 26.5% yoy, with passenger load factor improving by 2.0 percentage points to 85.2%.

HK Express, the Group’s wholly owned low-cost carrier, recorded more pronounced capacity expansion during the period, contributing 12 new destinations. Its ASK increased by 31.9% yoy, RPK rose by 25.8%, and passengers carried reached 7.91 million, up 29.7% yoy, while passenger load factor declined by 3.8 percentage points yoy to 79.6%.

As global capacity supply continued to recover and market competition intensified, fare tailwinds further faded. Cathay Pacific’s yield (revenue per passenger kilometre) declined significantly by 10.3% yoy to HK60.4 cents, while HK Express’ passenger yield decreased by 15.3% yoy to HK44.2 cents.

Affected by changes in customer travel destination preferences, the launch of multiple new routes (which require time to mature), and the continued grounding of part of its fleet due to the industry-wide unresolved Pratt & Whitney engine issues, HK Express’ EBIT loss widened from HK$204 million in the same period last year to HK$996 million.

In the cargo segment, impacted by additional tariffs and changes in de minimis policies, although available cargo tonne kilometres increased by 8.3% yoy, yield declined slightly by 4.6% to HK$2.69, and cargo load factor decreased by 1.1 percentage points yoy to 58.8%. The Group responded by diversifying its layout and adjusting its global network, with cargo services revenue remaining stable, up 0.6% yoy to HK$27,572 million.

Unit Costs Further Diluted, Financial Structure Continued to Improve

In terms of cost components, non-fuel costs increased by 13.4% yoy to HK$71,349 million, driven by capacity expansion. Among these, staff costs, inflight service costs and ground handling costs increased by 19.2%, 35.8%, and 22.7%, respectively, reflecting higher manpower input as well as increased route and maintenance expenses associated with capacity growth. Total fuel costs rose by only 8.3% yoy, benefiting from a 9% decline in fuel prices and remaining significantly below the increase in capacity, which led to a 2.4% yoy decrease in fuel cost per ATK and a 1.7% yoy decrease in non-fuel unit costs. The expansion of available capacity helped dilute unit costs.

Among other expenses, net finance charges decreased by 12.4% yoy, while aircraft depreciation and leasing costs declined by 4.1% yoy, reflecting the effectiveness of fleet optimisation.

The Company’s financial structure further improved. Net borrowings decreased to HK$46,812 million during the year, down 19.2% yoy; net debt-to-equity ratio declined from 1.10x to 0.78x, indicating that the high leverage accumulated during the pandemic is being gradually digested.

As at the end of 2025, Cathay Group operated a total of 237 aircraft, including 152 owned and 85 leased. In 2026, eight new-generation narrow-body aircraft will be delivered, with passenger capacity expected to increase by approximately 10%, which will also support growth in cargo capacity.

Investment thesis

As fuel costs typically account for one-third of total airline costs, the recent surge in international oil prices driven by geopolitical factors in the Middle East has raised market concerns over margin pressure on airlines. However, the International Air Transport Association (IATA) noted that global aviation demand has not weakened, with many itineraries originally destined for the Middle East being redirected to Europe or Asia. IATA continues to forecast a 4.4% increase in global passenger traffic this year.

In our view, the key takeaway from Cathay Group’s 2025 results is that, at a time when the industry is generally under pressure, strategic discipline can be translated into financial resilience. While the challenges in 2026 will be more complex, with volatility in oil prices, trade tensions, and fare competition posing significant tests not only of strategic direction but also of execution capability.

We revised the EPS forecast of Cathay to be HK$1.253/1.658 in 2026/2027/2028. Based on the revised financial forecast, we lift target price to HK$13.6 for the Company, equivalent to 2026/2027/2028E 10.9/8.2/8.0 x P/E, 1.42/1.31/1.20x P/B , the Accumulate rating. (Closing price as at 26 March)

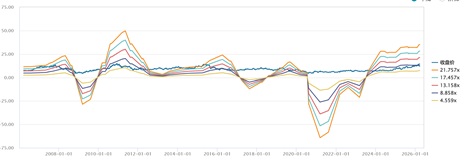

CX’s P/E trend

Source: Wind, Phillip Securities Hong Kong Research

CX’s P/B trend

Source: Wind, Phillip Securities Hong Kong Research

Risk

Surging oil price

Unfavorable Exchange fluctuations

Weaker Demand affected by economy

Fiercer ticket competition

War, Epidemic, etc

Financials

(Closing price as at 26 March)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()