-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

TME (1698.HK)-ARPPU as the primary growth driver

Thursday, July 24, 2025  109

109

TME(1698)

| Recommendation | Accumulate |

| Price on Recommendation Date | $84.000 |

| Target Price | $95.000 |

Weekly Special - 1024 Kuaishou

Company background

Tencent Music Entertainment (TME) is China’s trailblazer in online music entertainment services, offering both online music and music-centric social entertainment services. The company boasts an extensive user base and operates four leading mobile music products in the domestic market: QQ Music, Kugou Music, Kuwo Music, and WeSing. TME provides users with diversified music social entertainment products, creating an all-scenario music experience that includes "discover, listen, sing, watch, perform, and socialize." This empowers users to engage in music creation, appreciation, sharing, and interaction.

Financial performance

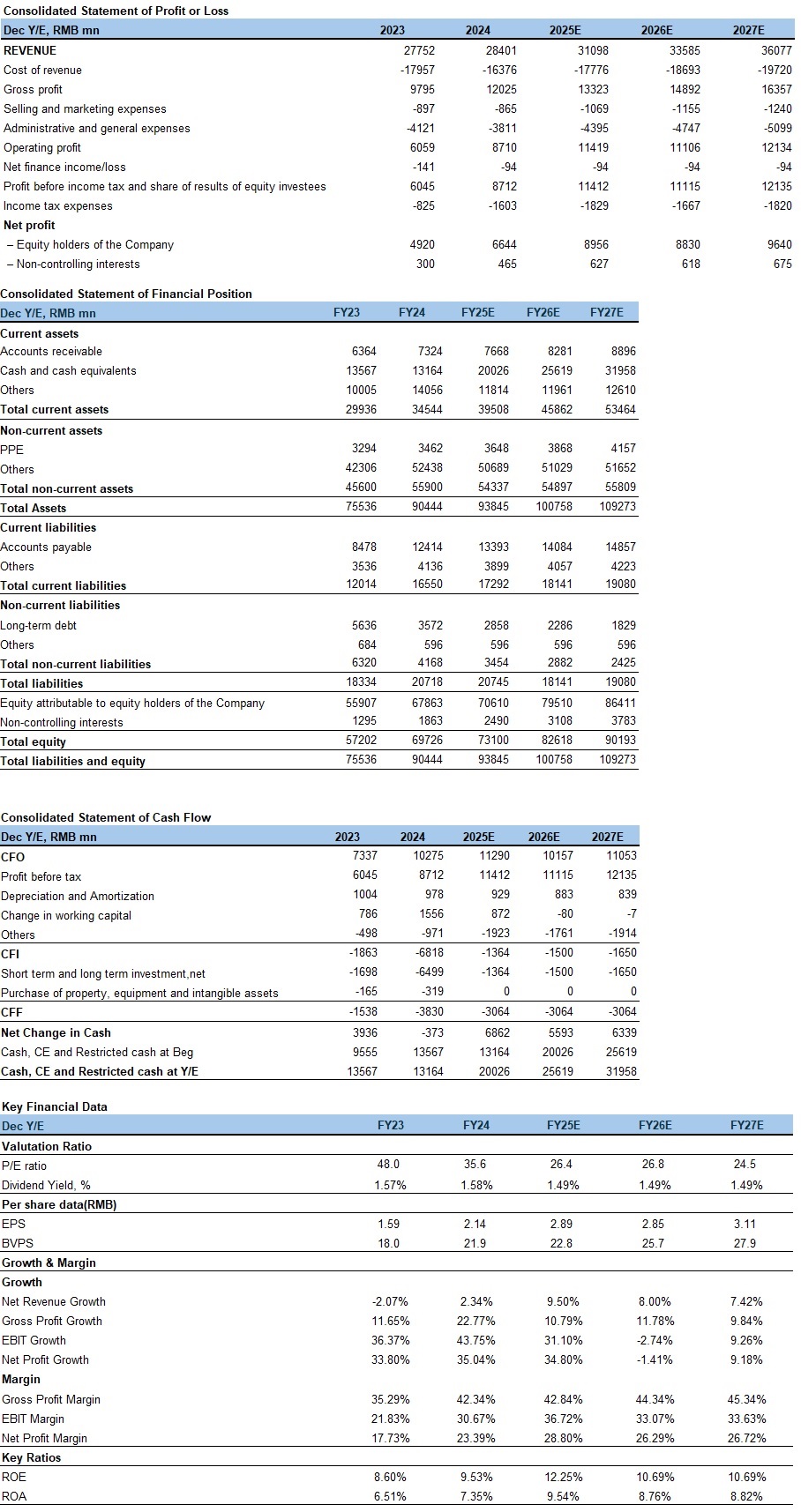

In the first quarter of 2025, the company generated total revenue of RMB 7.4 billion, representing a year-over-year increase of 8.7%. By segment, online music service revenue reached RMB 5.8 billion, up 15.9% year-over-year, primarily driven by growth in subscription service revenue and advertising service revenue. Social entertainment service and other service revenue amounted to RMB 1.6 billion, down 11.9% year-over-year, mainly due to impacts from compliance procedures and adjustments to live-streaming features. In terms of profitability, the company’s gross profit margin rose to 44.1% in Q1 2025, largely attributable to an optimized membership mix and increased proprietary content. Operating profit surged to RMB 4.8 billion, a 146.9% year-over-year increase, primarily fueled by a one-time gain from equity obtained through an associate company. Adjusted net profit grew to RMB 2.2 billion, up 22.8% year-over-year. Concurrently, the company announced an annual dividend of USD 0.09 per ordinary share for 2024.

Online Music Services: ARPPU as the Core Growth Engine

In the first quarter of 2025, online music subscription revenue reached RMB 4.2 billion, up 16.6% year-over-year, primarily driven by Super Digital Music Package (SDIP) growth and reduced promotional discounts. Advertising service revenue totaled RMB 1.6 billion, increasing 13.7% year-over-year, mainly attributable to diversified product offerings. Operationally, the number of online music paying users grew 8.3% YoY to 123 million, with the paying ratio further rising to 22.1%. Narrower promotional discounts lifted Average Revenue Per Paying User (ARPPU) by 7.5% YoY from RMB 10.6 to RMB 11.4 monthly, while Monthly Active Users (MAU) contracted 4.0% YoY to 555 million.

The company stimulates deeper and broader music consumption through enriched content services, diversified membership privileges, and precision operations, driving high-quality growth in both standard and premium memberships. For non-paying users: on one front, incentive-based advertisements and interactive tasks maintain engagement while generating ad revenue; on another front, fan economy models – including digital albums, merchandise, and song rewards – create additional monetization touchpoints to enhance overall user monetization efficiency. We expect ARPPU elevation to remain the primary growth driver.

Company valuation

According to management, the company will continue optimizing its membership system, enriching exclusive benefits, and implementing precision operation strategies to drive dual growth in both SDIP scale and ARPPU. Consequently, we forecast 2025-2027 online music service revenue at RMB25.4/28.5/31.3 billion, representing YoY growth of 17%/12%/10%. Simultaneously, considering tightening regulations and plateauing traffic in the livestreaming industry, we project social entertainment service and other service revenue at RMB5.7/5.1/4.7 billion, reflecting YoY declines of 15%/10%/7%.

For the full-year outlook, the dual engines of SVIP subscriptions and advertising revenue – coupled with optimized content cost control and deepened partnerships with copyright holders – will sustain momentum. Management anticipates accelerated full-year revenue growth and continued gross margin expansion. While sales expenses will increase moderately but at a slower pace than revenue growth, administrative expenses will remain stable. This will drive significant YoY improvement in net profit margin. Therefore, we project 2025-2027 total operating revenue at RMB31.1/33.6/36.1 billion, with net profit attributable to shareholders at RMB9.0/8.8/9.6 billion, translating to EPS of RMB2.89/2.85/3.11. Given the company’s high-growth profile, we select NetEase Cloud Music and Spotify as comparable companies. Applying a 30x 2025 forecasted P/E multiple yields a target price of HKD 95. Current share price implies 2025-2027 P/E multiples of 26/27/25x. We initiate coverage with a "Accumulate" rating.

Risk factors

1) Intensifying competition;

2) Slower-than-expected user growth;

3) Copyright risks.

Financials

Current Price as of: Jul 21

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()