-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ADD Industry (603089 CH) - Effective Cost Rate Control Boosted Net Profit Margin,with Overseas Plant to Commence Production Soon

Thursday, September 11, 2025  200

200

ADD Industry(603089)

| Recommendation | Accumulate (Initiation) |

| Price on Recommendation Date | $16.480 |

| Target Price | $18.780 |

Weekly Special - 2145 CHICMAX

Company Profile

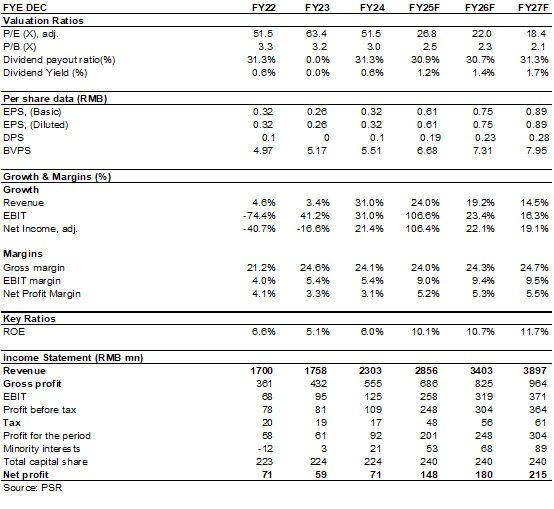

ADD Industry was established in 1994, specialising in the field of shock absorbers of the automotive suspension system. It has nearly 20 thousand product models covering most vehicle types worldwide and is a leading enterprise in China's shock absorber industry. At present, its business mainly includes shock absorbers of the automotive suspension system, automotive rubber damping products, as well as engine sealing components and other auto parts. In 2024, revenue reached RMB2,303 million (RMB, the same below), up 31.0% yoy, with overseas sales accounting for 82%. Net profit attributable to the parent company was RMB71 million, and net profit attributable to the parent company excluding non-recurring items was RMB64 million, up 21.4% and 22.2% yoy, respectively.

Investment Summary

Strong Growth in H1 2025 Results

The Company released its 2025 semi-annual report. In H1 2025, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB1,356 million/RMB119 million/RMB69 million, up 39.62%/420.67%/269.37% yoy, respectively. In Q2 2025 alone, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB740 million/RMB89 million/RMB41 million, up +34.62%/+1113.3%/+914.6% yoy, respectively.

Effective Cost Rate Control Boosted Net Profit Margin

According to the semi-annual report, gross margin was 24.29%, down 0.53 ppts yoy, remaining broadly stable, while gross profit increased by RMB88.4 million yoy. Period cost rate declined 3.2 ppts yoy to 12.6%, with sales/administration/R&D/financial cost rates down by-1.8/-1.3/+0.01/-0.2 ppts yoy, respectively, showing significant benefits from scale effect and cost control. In addition, the Company disposed of a piece of plant land during the period, recording a one-off disposal gain of RMB55 million, which also contributed to earnings growth. Net profit margin rose 7.07 ppts to 10.16%, and net profit margin excluding non-recurring items rose 3.16 ppts to 5.08%. Meanwhile, net cash flow from operating activities surged 412.6% yoy, reflecting continuous improvement in earnings quality.

Capacity Upgrade and Value Chain Integration

The Company is actively promoting capacity upgrading with its "Zhengyu Intelligent Manufacturing Park" as a platform. By the end of the reporting period, the Park had achieved a significant increase in production capacity, and the intelligent factory capacity matrix had been gradually established. The new Park not only significantly shortened the order delivery cycle but also formed an integrated "R&D--Intelligent Manufacturing--Delivery" closed-loop system, consolidating the Company's capability for rapid product iteration and continuously strengthening its technological moat in the industry. In terms of vertical integration, the Park extended the industrial chain upstream and has begun mass production of self-made high-precision stamping parts, high-precision piston rods, solenoid valves and other key shock absorber components, achieving in-house production of core parts. The deep extension of the industrial chain effectively reduced product defect rates, further optimised production costs, and established a rapid response mechanism, perfectly meeting the global customers' flexible customisation and high-frequency turnover demand for "multi-variety, small-batch, multi-batch" one-stop procurement.

Global Deployment Accelerating Capacity Expansion, with Overseas Plant to Commence Production Soon

The Company's intelligent manufacturing base in Thailand has already entered large-scale production, and investment will continue to be increased to expand capacity. At present, the Company's capacity expansion is entering an accelerated phase. Capacity was RMB1.7 billion in 2023 and is expected to reach RMB4.4 billion by 2027, an expansion of 2.5 times in four years. The Company has a production capacity of RMB3.4 billion in China and a capacity of RMB1.0 billion in Thailand, further strengthening its global delivery capability.

Investment Thesis

As a leading enterprise in the domestic shock absorber industry, the Company has achieved in-house production of core components through the construction of intelligent manufacturing parks, enhancing its vertical integration capability. Such technological barriers and economies of scale enable it to occupy a favourable position in the global automotive after-market. With global vehicle ownership exceeding 1.6 billion units, equivalent to demand for over 800 million shock absorbers, and a market size of about RMB70 billion, the Company is well positioned to continue benefiting from this trend.As for valuation, we expected diluted EPS of the Company to RMB 0.61/0.75/0.89 of 2025/2026/2027. And we accordingly gave the target price to RMB18.78, respectively 31/25/21x P/E for 2025/2026/2027. "Accumulate" rating. (Closing price as at 10 September)

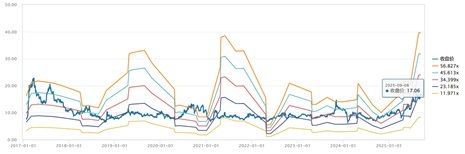

Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

Risk Factors

1) Progress of new production line is below expectations;

2) Overseas market risk;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices.

Financial Data

(Closing price as at 10 September 2025)

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()