-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李曉然小姐(Margaret Li)

分析師

分析師

本科主修市場行銷和英語,並於香港浸會大學獲得經濟學碩士學位。現為輝立証券持牌分析師,主要負責能源和公用事業等板塊的研究。曾在大型銀行、券商和資產管理公司工作,對於期貨和大宗商品衍生品領域擁有銷售、研究分析和市場推廣等工作經驗。

Margaret, a holder of a Bachelor`s degree in Marketing and English and a Master`s degree in Applied Economics from Hong Kong Baptist University, is currently employed as a licensed analyst at Phillip Securities. She specializes in conducting research focusing on the energy and utilities sectors. Prior to her current position, Margaret gained valuable work experience in a large bank, securities firm, and asset management companies. Her expertise lies in sales, research analysis, and marketing within the fields of futures and commodities derivatives.

| Phone: | 22776535 | Email: | margaretli@phillip.com.hk | |

CHINA RISUN GP (1907.HK) -

Friday, November 7, 2025  28

28

CHINA RISUN GP(1907)

| Target Price | $3.130 |

Weekly Special - 3606 Fuyao Glass

Overview

CHINA RISUN GP (1907.HK), founded in 1995, has grown into a leading integrated producer, supplier, and service provider of coke, coking products, fine chemicals, and hydrogen energy products in China and globally. According to a 2024 industry report by Frost & Sullivan, the company is the world's largest independent coke producer and supplier; the world's largest processor of crude benzene from coking, the second-largest processor of high-temperature coal tar, and the second-largest producer of caprolactam by capacity. It is also China's largest producer of phthalic anhydride from industrial naphthalene and methanol from coke oven gas, as well as the largest supplier of high-purity hydrogen in the Beijing-Tianjin-Hebei region by output.

Company performance review

Core Business Under Pressure, Trade Business Becomes the Only Growing Segment

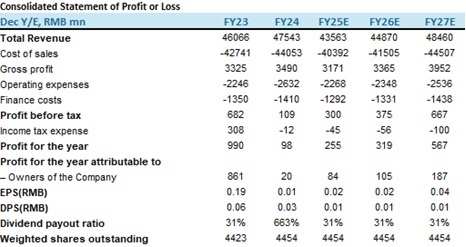

In H1 2025, the company's revenue was RMB 20.549 billion with a year-on-year decrease of 18.5%. Among this, revenue from the coke and coking products production business was RMB 6.358 billion, down 35.2% YoY, mainly due to supply-demand imbalances, declining coking coal prices, and export challenges, which led to a significant drop in coke prices. Revenue from the fine chemical products production business was RMB 9.096 billion, down 12.6% YoY, primarily because of falling crude oil prices and weak demand, which significantly reduced the average prices of products such as caprolactam and pure benzene. However, losses in the styrene segment narrowed due to improved supply-demand dynamics. Revenue from the operations management business was RMB 1.275 billion, down 47% YoY, mainly as agreements for three projects---Wanshan Chemical, Baoshun Chemical, and Chenyao Chemical---were completed, leading to a decrease in operations management income. Revenue from the trade business was RMB 3.73 billion, up 53.3% YoY, driven by increased trade volume of coke. Revenue from other businesses was RMB 90 million, down 43.2% YoY, mainly due to the completion and sale of real estate projects, which reduced income from commercial housing, partially offset by increased rental income from Risun Building. Profit for the period was RMB 87 million, down 34.9% YoY. Basic earnings per share were 0.66 cents with a decrease of 74% YoY.

Cost Control Drives Profit Improvement, Gross Profit Margin Rises 0.8 Percentage Points YoY

In H1 2025, the cost of sales was RMB 18.862 billion, down 19.23% year-on-year. Breaking it down: The cost of sales for the coke and coking products production business was RMB 5.602 billion, a decrease of 38.3% YoY, primarily due to the continuous decline in coking coal market prices, which led to a corresponding reduction in coal blending costs; the cost of sales for the fine chemical products production business was RMB 8.34 billion, down 12.4% YoY, mainly because raw material prices fell to varying degrees compared to the previous year; the cost of sales for the operations management business was RMB 1.213 billion, a decrease of 47.1% YoY, also influenced by the completion of the three projects mentioned in the revenue section; driven by increased business volume, the cost of sales for the trade business was RMB 3.641 billion, up 57.3% YoY; due to reduced property sales, the cost of sales for other businesses was RMB 66 million, down 56.2% YoY. The gross profit margin was 8.2%, an increase of 0.8 percentage points YoY, reflecting the company's effective cost control measures. Notably, the gross profit margin for the coke and coking products segment improved by 4.4 percentage points YoY.

Coke Business Strengthens Leading Position with Diversified Growth Drivers

As the world's largest independent coke producer and supplier, the company's coke business is poised to maintain steady growth, driven by capacity expansion, deepening internationalization, and optimization of the industry's supply structure. Downstream demand for coke primarily stems from the steel industry. Data from the National Bureau of Statistics show that China's crude steel output from January to August 2025 reached 672 million tonnes, down 2.8% year-on-year. China Steel News projects that China's crude steel output in 2025 will decline by 2% to approximately 986 million tonnes. However, coupled with steel capacity expansion in Southeast Asia (largely driven by Chinese investments), this indicates that coke demand remains resilient. Currently, the company's managed coke capacity stands at 26.6 million tonnes, with 17 operational coke production lines. Supported by the capital-light expansion of operations management services and the commissioning of overseas projects such as those in Indonesia, the stability of business revenue has been further enhanced. The company is developing the Pingxiang production base in the Xiangdong Industrial Park, constructing coke production facilities with an annual capacity of 1.8 million tonnes, expected to be completed by the end of 5 or early 2026. Additionally, the company has successfully commissioned the first coke oven of the 3.2-million-tonne-per-year coking project in the Indonesia Sulawesi Park. To date, the company has established subsidiaries/offices in 11 countries and regions, including Indonesia, Singapore, and Japan, with business operations spanning 41 countries. The establishment of Brazil office will further expand its presence in the Latin American market, underscoring the company's deepening global footprint. The Central Financial and Economic Affairs Commission has repeatedly emphasized curbing "low-price, disorderly competition" and facilitating the exit of inefficient production capacity. The sixth meeting of the commission in July this year explicitly called for "addressing low-price, disorderly competition in accordance with laws and regulations." It is expected to accelerate the phase-out of capacity from small and medium-sized coking enterprises and increase industry concentration. Amid the industry's "anti-involution" trend and capacity consolidation, leading companies are set to become stronger. We believe the company will directly benefit from this trend, continuously expanding its market share and strengthening its pricing power.

Scale Leadership and Industrial Chain Extension Drive Long-Term Chemical Growth

The company's chemical business has established significant scale and market position advantages, with its core products occupying key roles in the global industrial chain. Starting from coking, the company has adopted a vertically integrated business development model, extending into three chemical industrial chains: carbon materials, aromatics, and alcohol-ammonia. The total managed capacity reaches 6.04 million tonnes per year, of which 660,000 tonnes per year come from operations management service projects. The company aims to achieve an operational scale of over 1.65 million tonnes per year for caprolactam by 2030, further solidifying its leading position in the industry. Its production bases are distributed across multiple locations, including Xingtai, Dingzhou, Cangzhou, Leting, Yuncheng and Dongming in Shandong Province, and Hohhot in Inner Mongolia. The company is committed to becoming a globally leading nylon new materials enterprise. In October 2025, it plans to commence production of 50,000 tonnes per year of hexamethylenediamine. Through continuous R&D and innovation, the company will further extend its reach into downstream sectors such as PA66 and high-temperature nylon, among other new materials.

Venturing into the Clean Energy Blue Ocean, Building a Hydrogen Business Growth Engine

In H1 2025, the company's high-purity hydrogen sales volume reached 11.43 million cubic meters with a year-on-year increase of 22.9%, while revenue from the hydrogen segment was RMB 56 million, up 47.4% year-on-year. Since 2020, the company has actively expanded into the hydrogen sector and has established a foundation for scaled production capacity. As of the end of March in 2025, the company operates five high-purity hydrogen production lines located in Dingzhou, Xingtai, Tangshan, and Hohhot (Inner Mongolia), with a total production capacity of 34 tonnes per day. It also operates four hydrogen refueling stations with a combined capacity of 5 tonnes per day, making it the second-largest high-purity hydrogen supplier in China and the largest in the Beijing-Tianjin-Hebei region. Guided by its core development strategy of "Production-Storage-Transportation-Refueling-Application + R&D," the company has built a comprehensive value chain covering hydrogen supply, storage and transportation technologies, and end-use applications. Additionally, the company plans to advance hydrogen industrialization projects in Hebei, Inner Mongolia, and other regions, gradually expanding into applications such as synthetic ammonia and hydrogen fuel. In September 2025, the company successfully launched the 5,000 Nm³/h hydrogen project at its Leting Park, achieving full operational status. The first shipment of high-purity hydrogen was loaded and dispatched, marking a significant milestone in scaling the company's hydrogen business and further enhancing its market share. This success solidifies the company's leading position in the Beijing-Tianjin-Hebei hydrogen market. The company has expressed its intention to continue exploring merger and acquisition opportunities in the hydrogen sector. A successful acquisition would help address technological gaps and accelerate the commercialization process.

CHINA RISUN GP and Haidian District State-owned Assets Investment Group Co., Ltd have established a strategic cooperation relationship

This partnership is expected to provide critical support for CHINA RISUN GP in its industrial upgrading, business expansion, and market-oriented transformation through resource synergies, complementary businesses, and capital empowerment, delivering long-term benefits to the company.

Company valuation

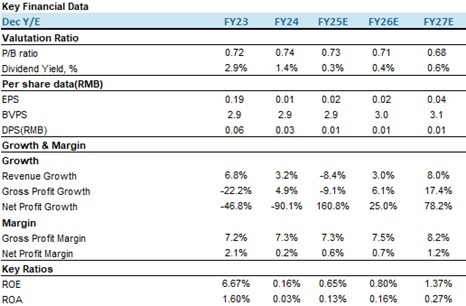

As a global leader in coking and fine chemicals, CHINA RISUN GP leverages its scale advantages and integrated industrial chain capabilities, demonstrating resilience across industry cycles through its traditional businesses, while its fine chemical and hydrogen energy initiatives provide long-term growth potential. In the short term, the focus should be on the pace of coke profit recovery and the effectiveness of cost control measures; in the long term, performance will depend on the industrialization progress of its hydrogen energy business and the success of its international expansion. The company is currently trading at a historical low valuation, with a potential valuation rebound expected by year-end. We forecast the company's revenue for 2025-2027 to be RMB 43.563 billion, RMB 44.870 billion, and RMB 48.460 billion, respectively, with BVPS of RMB 2.9, RMB 3.0, and RMB 3.1. The target price is set at HKD 3.13, corresponding to a projected price-to-book (P/B) ratio of 0.96x for 2026, which is in line with the average P/B ratio over the past three years. The rating is "Buy." (Current price as of November 5)

Risk factors

1) Macroeconomic downturn;

2) Intensifying industry competition;

3) Decline of coke price.

Financial

(Current Price as of: 05 Nov 2025)

Exchange rate: HKD/RMB = 0.92

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()