-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

Meituan (03690.HK) - Intensified competition may continue to put pressure on the profitability

Friday, September 5, 2025  1448

1448

Meituan(3690)

| Recommendation | Accumulate |

| Price on Recommendation Date | $100.500 |

| Target Price | $118.300 |

Weekly Special - 175 Geely

Company Profile

Meituan is a leading e-commerce platform for lifestyle services in China, providing services including food delivery, in-store, hotel and travel, and new initiatives. Its Core Local Commerce segment includes food delivery, Meituan Instashopping, in-store, hotel and travel, etc. New Initiatives include Meituan Select, Meituan Grocery, ride-hailing, shared bikes, charging, and restaurant management systems.

Financial summary

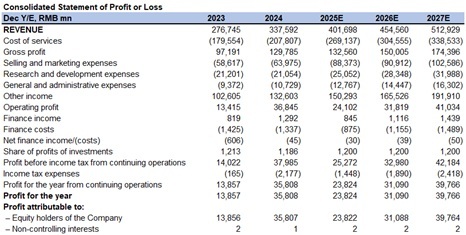

In the second quarter of 2025, Meituan reported total revenue of 91.8 billion yuan (RMB, same below), a year-on-year increase of 11.7% and a quarter-on-quarter increase of 6.1%. In terms of profitability, operating profit was 200 million yuan, down 98.0% year-on-year and 97.9% quarter-on-quarter. Adjusted net profit was 1.5 billion yuan, down 89.0% year-on-year and 86.3% quarter-on-quarter. By segment, Core Local Commerce revenue in Q2 2025 was 65.3 billion yuan, up 7.7% year-on-year. Operating profit was 3.7 billion yuan, down 75.6% year-on-year, with an operating profit margin decreasing by 19.4 percentage points year-on-year to 5.7%, primarily due to intense competition in the food delivery industry. New Initiatives revenue was 26.5 billion yuan, up 22.8% year-on-year. Operating loss was 1.9 billion yuan, broadening by 43.1% year-on-year, mainly due to expanded overseas expansion. The operating loss ratio improved by 3.1 percentage points quarter-on-quarter to 7.1%, primarily due to improved operational efficiency.

In terms of expenses, sales costs in Q2 2025 were 61.4 billion yuan, up 27.0% year-on-year, accounting for 66.9% of revenue, up from 62.6% in the previous quarter, mainly due to rider subsidies and the expansion of instant retail business. Sales and marketing expenses were 22.5 billion yuan, up 51.8% year-on-year, accounting for 24.5% of revenue, up from 18.0% in the previous quarter, primarily due to increased user incentive spending. R&D expenses were 6.3 billion yuan, up 17.2% year-on-year, accounting for 6.8% of revenue, remaining stable quarter-on-quarter. General and administrative expenses were 2.7 billion yuan, accounting for 2.9% of revenue, also stable quarter-on-quarter.

Financial performance

Food Delivery & Instashopping Business

The food delivery industry is becoming increasingly competitive. In April, competitor JD Delivery rapidly increased order volumes through its 'Billion-Dollar Subsidy' program, and competition intensified further in May when Taobao Flash Purchase joined the subsidy war. In response, the company employed strategies such as 'Shen Qiang Shou', 'Pin Hao Fan', and subsidies for both consumers and merchants to tackle the competition. This drove overall expansion in the food delivery market order volume. We estimate that Meituan's food delivery order volume growth accelerated to 10.0% year-on-year in Q2 2025, boosted by competition, while delivery service revenue grew by only 2.8% year-on-year, slower than the order volume growth. Meanwhile, the AOV for food delivery declined more significantly due to subsidies, coupled with higher per-order subsidies year-on-year and increased costs from improved social security systems. We expect the per-order UE for food delivery to turn negative in Q2 2025.

Looking ahead to the second half of the year, intensified competition is expected to continue driving order volume growth, but profitability may remain under pressure. In Q3, Taobao Flash Purchase launched a 50-billion-yuan subsidy plan and initiated the 'Super Saturday' campaign. The company quickly responded by matching subsidies, leading to record-high order volumes in instant retail. As of July 12, peak order volume reached 150 million orders, with 'Shen Qiang Shou' contributing over 50 million orders and 'Pin Hao Fan' contributing over 35 million orders. Due to the increased intensity and prolonged duration of competition in food delivery and flash purchase, we expect year-on-year order volume growth for both segments in Q3 and Q4 to further accelerate compared to Q2. However, profitability is likely to remain under pressure. Considering management's guidance that the Core Local Commerce segment may turn from profit to loss in Q3, we expect the operating profit margin for Meituan's food delivery and flash purchase businesses to turn negative in 2025.

New Business

The company has restructured its fresh grocery business, significantly scaling back 'Meituan Select' and fully committing to 'Xiaoxiang Supermarket', with plans to cover all first- and second-tier cities. For overseas operations, Keeta has entered the Qatar market, setting a long-term goal of achieving $100 billion in GMV over the next decade. While the company is not rushing this process, it remains optimistic about the long-term growth potential. According to management, due to restructuring costs associated with business adjustments and the expansion of Keeta in the Middle East, the loss for the New Initiatives segment is expected to widen to 2.3-2.4 billion yuan in the third quarter.

Company valuation

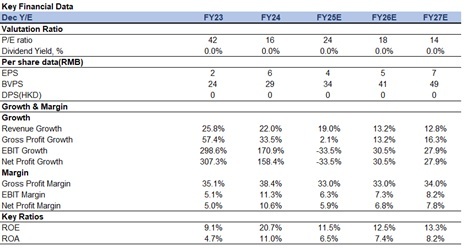

The company's financial resources are more limited compared to Alibaba, which may put it at a disadvantage in a prolonged cash-burning competition and pose a risk of market share loss. However, considering the potential for profit recovery between 2026 and 2027, we have adjusted our revenue forecasts for 2025-2027 to 401.7/454.6/512.9 billion yuan, with net profit attributable to shareholders at 23.8/31.1/39.8 billion yuan, corresponding to EPS of 4/5/7 yuan.

Based on the SOTP valuation method, we estimate Meituan's total target market capitalization for 2025 to be 664.7 billion yuan. We have lowered the target price to HK$118.3. The current stock price corresponds to a PE ratio of 24x/18x/14x for 2025-2027. We downgrade our rating to 'Accumulate'. The segment valuation includes the following parts:

1) Core Local Commerce is valued at 526.8 billion yuan, using an 8% weighted average cost of capital and 5% perpetual growth rate;

2) New Initiatives are valued at 81.8 billion yuan, applying a 0.8x 2025 P/S multiple;

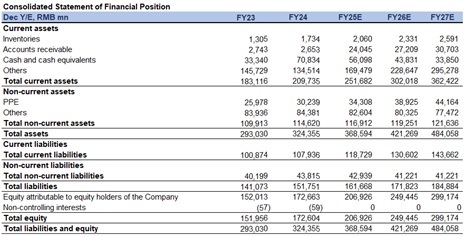

3) Net cash amounts to 56.1 billion yuan.

Risk factors

1) New business performance below expectations;

2) Intensified competition in the food delivery and travel industries;

3) Weaker than expected recovery in consumer demand.

Financials

(Closing price as of 3 Sep 2025)

Exchange rate: RMB/HKD = 1.09

Source: PSHK Est.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()