-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Yunnan Baiyao (000538.CH) - Implementation of Composite-Ownership Reform Helps Enter New Stage of Development

Friday, January 6, 2017  23955

23955

Yunnan Baiyao

| Recommendation | BUY |

| Price on Recommendation Date | $73.900 |

| Target Price | $90.600 |

Weekly Special - 2333 Great Wall Motor

Strong Brand Extension Ability

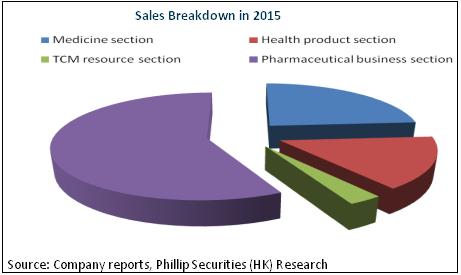

Yunnan Baiyao started from producing and selling an anti-infective, hematostatic traditional Chinese medicine (TCM) "Baiyao". The Baiyao formula, a state-level secret, has no direct competitor and strong pricing ability. In recent years, the company has actively implemented the "medicine-centered" strategy of developing "New Baiyao, Great Health", focusing on boosting four major business sectors: in the medicine section, Yunnan Baiyao core/transdermal series are mature cash cow varieties, and the generic drugs are promoted steadily by a series of new products, such as Qixuekang oral solution and Xuesaitong capsule; the health product section focuses on promoting Yangyuanqing hair wash & care series and Qingyitang sanitary towel series, while ensuring the rapid growth of Baiyao toothpaste; the TCM resource section, in light of the resource edge of natural, genuine vegetable drugs from Yunnan, has built a complete industrial chain of raw materials; in addition, the company's pharmaceutical business section has made stable revenue contribution to the company via continuous channel improvement.

It is worth mentioning that the company brand extension ability has been prominent in the new strategy promotion, and Yunnan Baiyao toothpaste has become a well-known brand, ranking among the top three in terms of market share and being the only homegrown brand in the top five taking the largest market shares. Therefore, the company has been a long-term champion among the pharmaceutical stocks over the past 10-odd years.

Implementation of Composite-Ownership Reform Helps Enter New Stage of Development

According to the announcement, New Hua Du intends to issue a capital increase of around RMB25.4 billion to the company's controlling shareholder Yunnan Baiyao Holdings Limited. When completed, Baiyao Holdings` ownership will be equally held by the SASAC of Yunnan Province and New Hua Du, each with a 50% equity, instead of being held by the SASAC of Yunnan Province exclusively. Meanwhile, Baiyao Holdings still holds 41.52% share of the company. This transaction also triggered a tender offer at the listed company.

After the completion of the composite-ownership reform, the group will be state-owned and private-owned rather than solely state-owned, and the private owner has sufficient right of speech as a shareholder, which will contribute to Yunnan Baiyao's more flexible and market-oriented management (Baiyao Holdings` directors, supervisors and senior management will be recruited under the market-oriented principle) and lay the foundation for the listed company's future promotion of stock ownership incentive. At the same time, the company's external M&A is also expected to accelerate and new business development to step into a new stage. In the future, the company is expected to speed up businesses in precise medical care, pension & health care, medical services and other major health areas, thus promoting the company's entering a new stage of development.

It is notable that the reform has fully triggered a tender offer of Yunnan Baiyao, not at the cost of terminating the listing status of the company. The purchase price of up to RMB64.98, only 6.1% lower than that before the suspension, will provide strong support for the stock price.

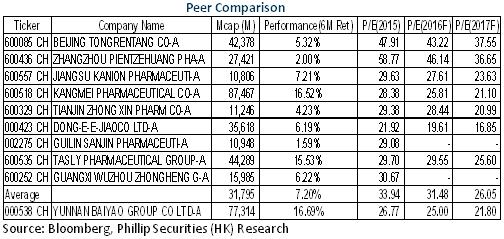

Valuation Lower Than Counterparts

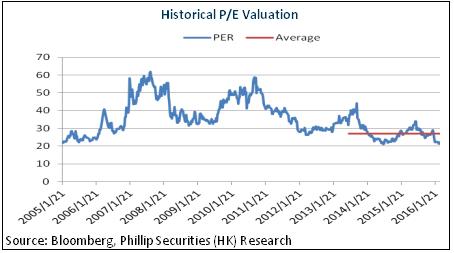

Yunnan Baiyao, a leading TCM enterprise in Mainland China, has attained significant results in implementing the Great Health strategy over the recent years. And the fast implementing speed and high efficiency of approval of the composite-ownership reform are rarely seen in the industry and expected to become the industry's benchmarking event. In light of the company's steady development of the original major businesses and profound resource value of brand, coupled with the development opportunity brought by the composite-ownership reform, we grant it an estimation of 27.5x EPS in 2017 and a target price of RMB90.6, with the "Buy" rating initially. (Closing price as at 4 Jan 2017)

Risks

The growth rate of everyday chemicals below expectations;

Rising price of major raw materials;

Results of the reform of state-owned enterprises below expectations.

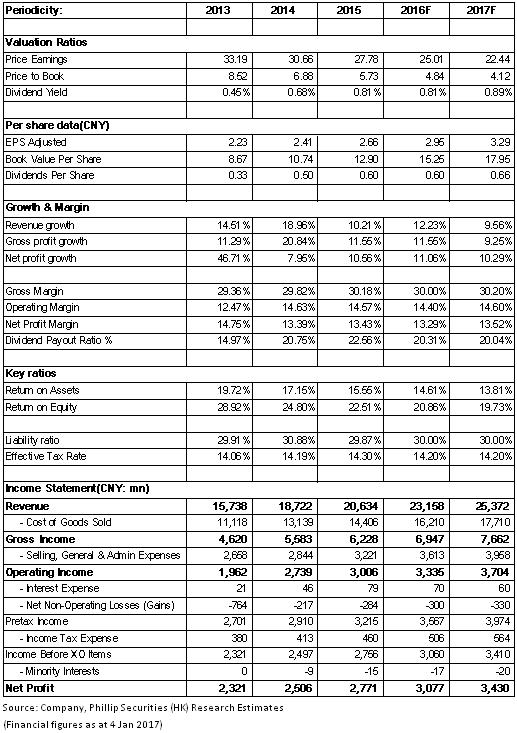

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()