-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Chinasoft International (354.HK) - The Leader of the software market in China

Friday, October 19, 2018  14488

14488

Chinasoft International(354)

| Recommendation | Buy |

| Price on Recommendation Date | $4.150 |

| Target Price | $5.530 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

Chinasoft International (Chinasoft) is one of the leading software and information services companies in China. Its major business includes consulting services, technical services, outsourcing services and training services. Based on 2018 net profit, we assume a P/E ratio of 16.5x (the average over the past two years), deriving a target price of HK$5.53, and a “Buy” rating with a potential return of approximately 33.3%. (Closing price at 16 Oct 2018)

Thanks to the SaaS market and industry digitalization, software market in China will continue to grow

According to Battery Ventures, the future growth driver of the software market will be the SaaS market. The compound growth rate of the world and China will be 18% and 40% respectively in 2017-2021. In addition, thanks to factors such as the digitalization of traditional industries and the "Internet Plus" policies, software will be applied to various industries in the future, especially those traditional ones. We believe that software business revenue in China will gradually rise in the future with stable growth.

Experienced in industry solution with technological advantages

The company has been focusing on the solution business since its establishment, and has accumulated enriched experience and technological advantages in various industries, including Finance, Telecommunications, Internet and High-tech and Public affairs industries. It serves customers, such as Huawei, HSBC, Tencent, Alibaba, China Mobile and so on. In the meantime, the company also develops its own software products, such as ResourceOne, Toplink/Flowpower and Ark.

Optimizing business model by the launch of Jointforce, attached multiple platforms

At the end of 2014, the company launched a crowdsourcing platform “Jointforce”, which targets small and medium-sized customers and the long-tailed market, enabling the company to concentrate resources on serving large customers. At the same time, forming an ecological platform, the company launched the Cloud Software Park, Honeycomb and Cloud Integrative Service in Jointforce, in order to enhance the function and attractiveness of the platform.

Interim net profit rose significantly, but revenue growth slowed down

The interim net profit increased by 48.0% to RMB 356 million. However, revenue growth was only 16.1%, reaching RMB 4.81 billion, lower than the growth rate in 2017 interim results. Operating cash flow was negative RMB 869 million, up 40.6% YoY. The service revenue of the top five customers accounted for 67.7% of the company's total service revenue. And, the number of employees in the company reached 54,663, up 8.6% YoY.

Corporate development

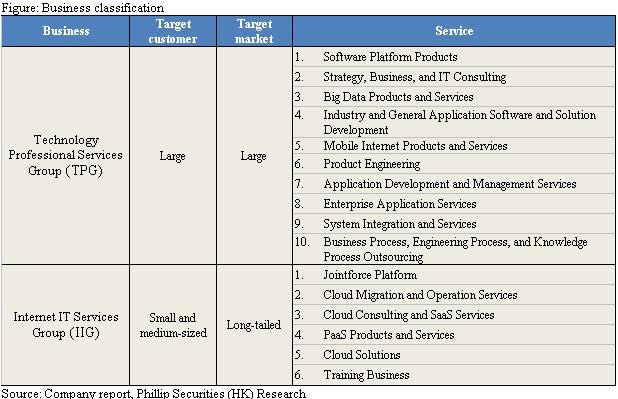

Founded in 2000, ChinaSoft is one of the leading software and information services companies in China. Its major businesses include consulting services, technical services, outsourcing services and training services. At the beginning of its establishment, the company mainly engaged in e-government projects from government departments, as well as office automation projects from the auditing department and the transportation department. The company has also established a strategic partnership with the National Tobacco Monopoly Bureau. Later, the company expanded its customers into different areas, such as financial services, technology, power and transportation, and successfully acquired large customers such as Huawei, Tencent, Alibaba, Baidu, Ping An and HSBC. Among them, Huawei is the largest customer of the company, and has signed a strategic cooperation agreement with Chinasoft in August 2014 for the field of computing, network security, and industry 4.0. At the end of 2014, the company officially launched a crowdsourcing platform “Jointforce”, and attached with other platforms such as Cloud Software Park, Honeycomb and Cloud Integrative Service. In 2015, the company reorganized the business classification and divided it into Technology Professional Services Group and Internet IT Services Group. The former is mainly for the quality-sensitive and large customers; the latter is for the price-sensitive and small and medium-sized customers.

Business Overview

The company divides its business into two major components: 1) Technology Professional Services Group (TPG) and 2) Internet IT Services Group (IIG). TPG mainly provides services such as software development, business consulting, solutions and process outsourcing to customers, and is mainly for large customers and industries. The major customers are Huawei, HSBC, Tencent and so on. IIG is mainly an online business, providing services to price-sensitive customers and the long-tailed market, such as online distribution, cloud services and training services.

Industry Overview

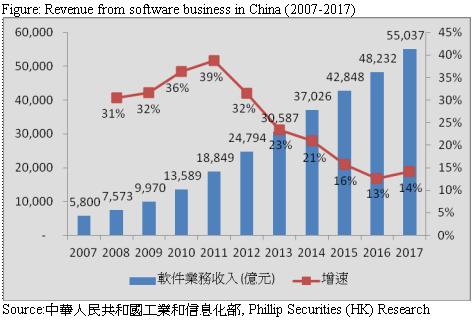

Due to the rise of digitalization and smart phones, and benefiting from the support of policies from government, the software industry in China has continued to develop steadily. Revenue from software business has remained an uptrend over the past decade, from RMB 580 billion in 2007 to RMB 5,573.7 billion in 2017, a CAGR of 25%. However, the growth has reached the peak in 2011 and dropped since then. But, software revenues rebounded slightly in 2017, mainly due to the growing popularity of big data and cloud services.

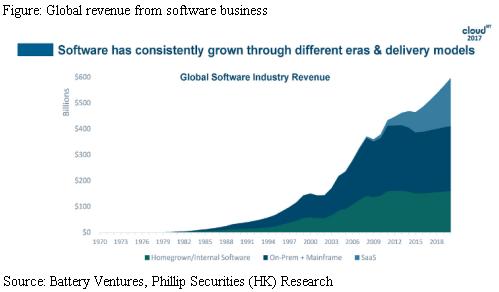

SaaS will become the new growth driver of software market in future

Before 2000, the growth of the software market was driven by Homegrown and Internal software. After 2000, On-Prem and Mainframe software became a new driver. In 2006, SaaS started to develop and became the new engine of the software market. According to Gartner's forecast, global SaaS revenue will reach $11.11 billion in 2021, with a CAGR of 18% in 2017-2021, where SaaS market in China will be growing stronger. According to IDC, SaaS market in China will reach US$4.89 billion by 2021, with a CAGR exceeding 40% in 2017-2021.

The digitalization of traditional industries

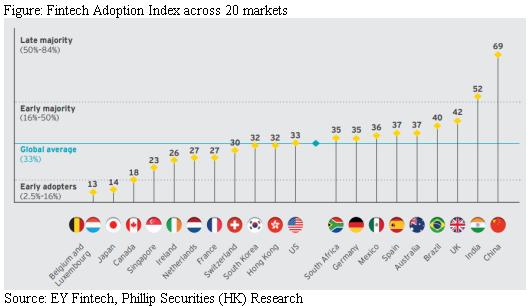

Under the trend of digitalization, software technology has gradually been introduced into different industries, such as government, medical, energy, finance, logistics and other industries. Among them, Fintech is the representative in the integration of software technology and traditional finance. Software technology has been widely applied in finance, such as payment and e-wallet, investment, P2P lending, insurance and financial management. In China, electronic payment instruments such as WeChat Payment and Alipay have been widely used. According to the Fintech Adoption Index calculated by EY Fintech, the global average adoption index has increased significantly from 16% in 2015 to 33% in 2017, reaching the Early Majority, where China (69%) and India (52%) even reached the Late Majority. With the increase in adoption index in South Africa, South Korea and Mexico, EY expects the global average application rate to reach 52% in the future. we believe that there will be more and more digitalization in traditional industries in the future, leading to a strong demand for software technology.

Policies like "Internet Plus" provide momentum to the digitalization

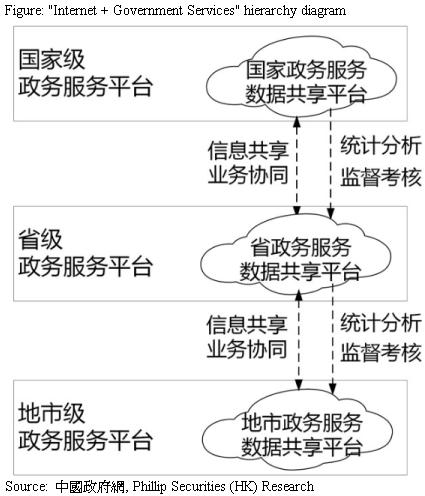

In the 12th National People's Congress in 2015, Premier Li Keqiang put forward the "Internet Plus" policies in the government report, suggesting taking advantage of Internet technologies, such as cloud computing, big data and the Internet of Things, to integrate with various industries, such as Industrial, financial, communications, transportation, medical and education, etc., to improve and optimize the business model of the industry and efficiency. For example, the "Internet + Government Services" guide launched by the General Office of the State Council requires the use of Internet, big data, cloud computing and other technological means to solve the problems of non-interoperability and non-sharing in online government service platforms. By unified platform and data sharing, the management from central government to provinces, cities and administrative efficiency will be effectively strengthened. In addition, the Ministry of Industry and Information Technology also announced in 2018 that the “Guidelines for Enterprise Cloud Migration (2018-2020)” encourages cloud migration in domestic enterprises. The goal is to reach the number of enterprises applying cloud by 1 million in 2020, and to form more than 100 typical application cases. With the promotion and encouragement of the government, the demand for software technology will be raised.

Competitive advantages

Focus on industry solutions business, rich experience builds technological advantages

Compared to software outsourcing services, industry solutions are located at the higher position in the value chain, bringing more valuable experiences and making the company easier to build long-term competitive advantage. Industry solution services require not only to deal with software coding, but also to perform system setup as well as conduct demand analysis. This requires companies with rich project experience and technological advantages. In addition, by developing industry-specific solution software, the company can repeatedly apply to similar scenarios, which will help improve efficiency and accumulate technological advantages. Moreover, as service providers need time to familiarize with other providers` systems, customers generally have greater switching cost on service providers. Therefore, we believe that industry solution services have higher barriers to entry, technological requirements and switching costs than software outsourcing services, and is able to establish significant and long-term competitive advantages.

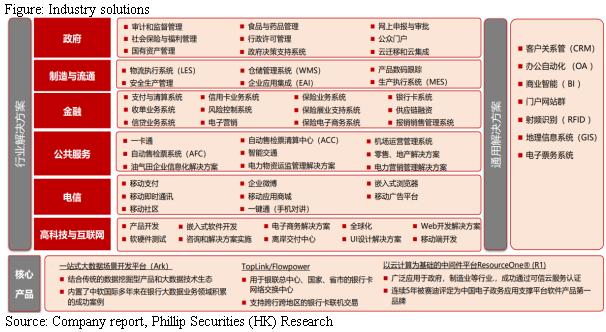

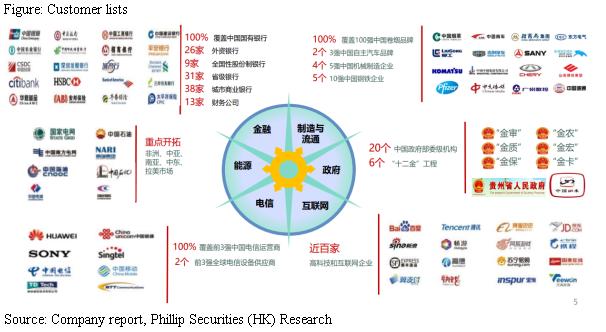

The company has been focusing on the solution business since its establishment, and has accumulated enriched experience and technological advantages in various industries, including: Finance, Telecommunications, Internet and High-tech and Public affairs industries.

In terms of Finance, Toplink/Flowpower, a self-developed payment platform product, is one of the company's core products. It is mainly used in the UnionPay General Center, the national, provincial and municipal bank card exchange centers, and also supports cross-regional bank card transaction. In China, the company has been providing industry solutions, system integration services and related high-end services to customers such as the five major state-owned banks, postal savings banks and foreign-funded financial institutions. In oversea, HSBC is the company's major customer, the major supplier of HSBC Global in China. In addition, the company's experience was across a wide range of businesses in the financial industry, including: payment and settlement systems, credit card business, insurance business systems, bank card systems, credit business systems and risk control systems. Menawhile, the company achieved "three national firsts" - the first national bank card interbank payment network system, the first national financial IC card payment clearing system and the first national e-commerce online payment and settlement system.

In terms of Telecommunications, the major customers are Huawei, China Mobile and China Telecom, among which Huawei is the largest customer. The company provides functions such as mobile payment, mobile instant messaging, and mobile application store. In 2016, the company and China Mobile cooperated to launch the "Fetion" communication business, and work on product design, software R&D, business operation, risk control and project management together. Moreover, the company has been involved in Huawei software development, and focused on software custom development and delivery services, telecommunications network management systems, telecommunications BSS systems, telecom value-added services, telecommunications network operation and maintenance tools and telecom equipment embedded software.

In terms of Internet and High technology, the company serves multiple Internet giants such as Tencent, Alibaba, Baidu and Sina, providing product development, embedded software development, hardware and software testing, UI design, mobile development and e-commerce solutions.

In terms of Public affairs, the company has been the leader in the solution market for public transportation, rail transit, airport management and other pan-traffic areas, and established three “First National Systems” – the first urban traffic card payment clearing system in the country, the first urban rail transit one-ticket transfer payment system and the first automatic ticket-checking (AFC) system with independent intellectual property rights. The one-card solution has been implemented in more than 30 cities, and the number of cards issued on the online system exceeds 100 million, which proves that the technology is highly regarded by customers. Besides, the company's self-developed middleware platform product, ResourceOne, is widely used in public affairs scenarios, helping to accumulate technological advantages in this industry.

The risk of customer concentration is greatly reduced by establishing a close relationship with Huawei

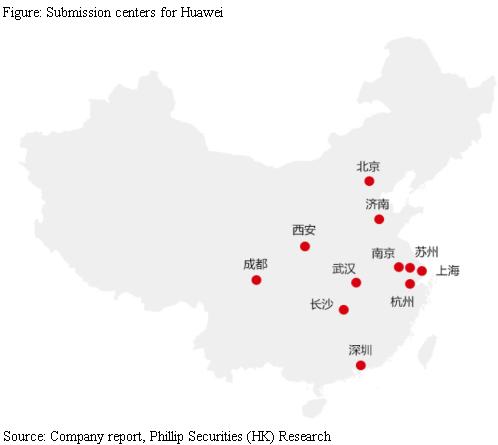

As of 2017, revenue from Huawei accounted for approximately 52.71% of total turnover. Many have regarded it as a big risk. If Huawei stops cooperating with Chinasoft, the company will lose almost half of its turnover, and we cannot deny that risk. However, the risk is not as big as it is supposed to be, because Huawei is highly concerned about the quality of its suppliers. It examines suppliers each year, and if they perform well, Huawei will be distributed more projects to them.Therefore, in order to meet it needs and examinations, we believe that it is difficult to establish a supplier relationship with Huawei in the beginning. Now, the company has established submission centers in 11 cities across the country, with 4 special laboratories and more than 20,000 people serving Huawei. Meanwhile, the company has also ranked first in Huawei's inspections in the past few years. This shows that Huawei may not be so easy to find other suppliers in the market to replace the company.

Huawei holds at least two supplier meetings each year, including: “Partners Meeting” and “Core Supplier Meeting”. It proves that Huawei highly regards its supplier partners. In 2017, the company signed to become Huawei's first “同舟共濟合作夥伴”, making Chinasoft no longer just a supplier, but a partner for Huawei.

As the company's cooperation with Huawei continues to go on, we believe that the risk of suddenly losing this big customer is not significant.

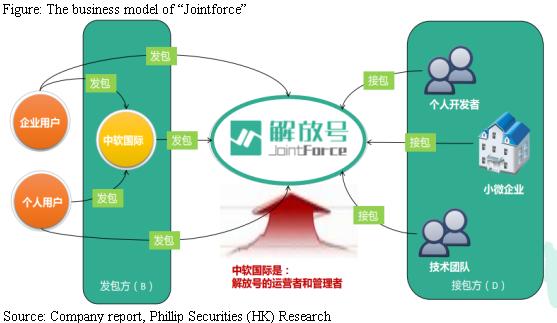

Optimizing the business model by the launch of “Jointforce”

For software development projects from small and medium-sized customers, the biggest problem is that most customers do not have the ability to distinguish the quality of products because of the lack of professional IT knowledge. Small and medium-sized customers often choose those outsourcing companies that can meet their demand and only ask for very low price. In other words, software products offer little differentiation for small and medium-sized customers, so they will rely more on price to make decisions, which undoubtedly makes the competition in the long-tailed market very fierce, and the project not so profitable.

Owing to the characteristic of the long-tailed market, Chinasoft launched the crowdsourcing platform “Jointforce” at the end of 2014 to outsource the small and medium-sized projects of the company. This not only helps Chinasoft to release resources and concentrate on large customers, but also does not have to give up small and medium-sized customers, and earn stable income from it. Therefore, the launch of Jointfore has helped Chinasoft optimize its business model.

The business model of Jointforce is to let the vendors enter the platform by charging the annual fee. The platform has two sources, and the client can directly place their package on the platform; or the client could place the package to Chinasoft, and then Chinasoft place the project to the platform later. In other words, the company act as a subcontracting role. As of 2017, there were a total of more than 300,000 engineers, 10,000 vendors and more than 30,000 clients in Jointforce, and the amount of the package has exceeded RMB 1.2 billion in the first half of 2018.

Rich industry experience enhance the credibility of the platform

Currently, the software crowdsourcing platforms in the market are only an Internet platform, such as: “滙新雲”, “開源眾包”, “碼市” and so on. They just simply link up the vendor and client, and have no experience or ability to assess the quality of vendors which receive the package. In fact, the platform needs to have rich industry experience to review the vendor, so it could enhance the level of the vender to attract more clients, forming a virtuous circle. In light of this, for the projects that Chinasoft subcontracts, the company will only select those vendors that they have already done research on them to receive the package, and will sign a strategic cooperation agreement with them. At the same time, the company will also provide quality assurance to the clients. For projects that are directly placed in the platform, the model is same with “Taobao”. The clients can visit the score of the vendor and the projects they have been done before, such as whether there delivered on time, etc., to review the quality of the vendors. Besides, the trading process of the parties, including signing, payment and delivery, will be carried out on the platform. The platform can provide evidence in case any argument in the future. The platform also has a third-party payment platform similar to Alipay to handle cash settlement. In 2018, Jointforce launched the Membership Privilege 3.0, which provides management tools and business data analysis tools for the members, as well as the optimization of user experience. In addition, the company launched the intelligent recommendation system 3.0 based on AI+ big data, the system dispatch time is as high as 92%, an increase of 12%.

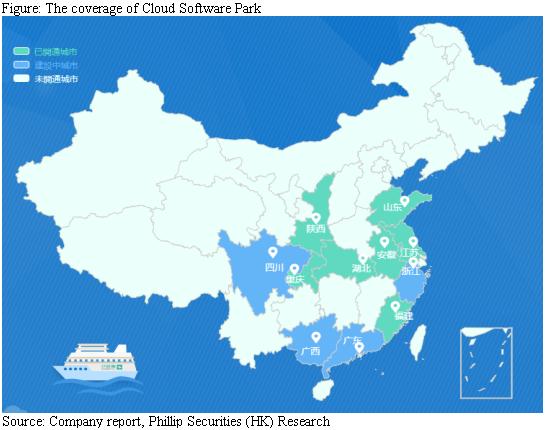

Attached a variety of platforms to Jointforce

ChinaSoft has launched three platforms on Jointfore – Cloud Software Park, Honeycomb and Cloud Integrative Service. By adding a variety of additional functions, it creates an ecosystem and maximize the potential of Joinforce.

By attracting the local software park vendors, Cloud Software Park aims to create a virtual software park online. Joinforce also provides software services and cloud development tools to bring online business to local software parks. At present, the cloud software park has covered 18 cities, including: Qingdao, Weihai, Jining, Xuzhou, Nanjing, Shanghai, Hefei, Zhangzhou, Nanping, Wuhan and Xi`an.

Cloud Integrative Service is designed to provide online procurement transaction services for government IT service projects. Through the research of nearly 10,000 software suppliers in the top 50 cities in the country, it can help the government find suitable suppliers. Now, it has successfully operated in Nanjing, has entered the verification phase in Xi`an, and also has strategic cooperation with the Zhenjiang Municipal Government.

Honeycomb is mainly for the manufacturing industry. It mainly provides testing services for the manufacturing industry to see if it meets industry standards. It will also provide manufacturing enterprises with a one-off solution for transformation and upgrading.

Earnings forecast

Revenue

The company divide its turnover into traditional business and emerging business from this year. We forecast the growth of traditional business in 2018/19F to be 15/14% respectively, as the company predicts that revenue growth from Huawei will begin to slow down in the future. However, business growth of other customers (such as HSBC, Tencent and Ping An, etc.) will remain strong, about 20-30%. For the emerging business, based on the network effect, we expect Jointforce and cloud business growth to gradually increase in 2018/19F, around 80/85% respectively.

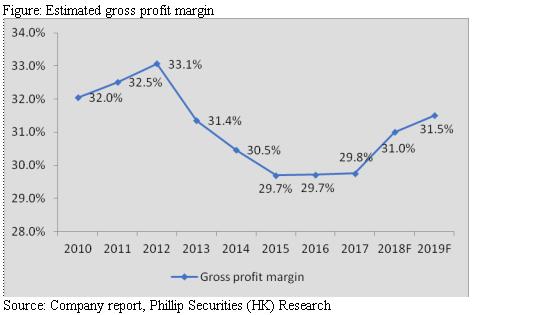

Gross profit margin

The gross profit margin of the company has fallen since 2012. However, due to the higher gross profit margin of emerging businesses, we estimate the gross profit margin to be 31/31.5% in 2018/19F, as the proportion of emerging businesses increases.

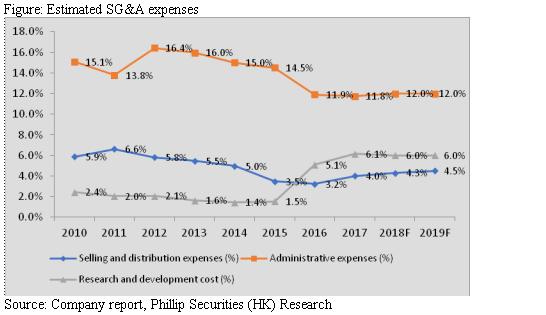

SG&A expenses

We predict that the administrative cost and R&D expenses as of revenue will remain stable in 2018/19F respectively, at 12% and 6%; the selling expenses as of revenue will increase due to the rapid growth of emerging businesses in 2018/19F around 4.3/4.5% respectively.

Net profit

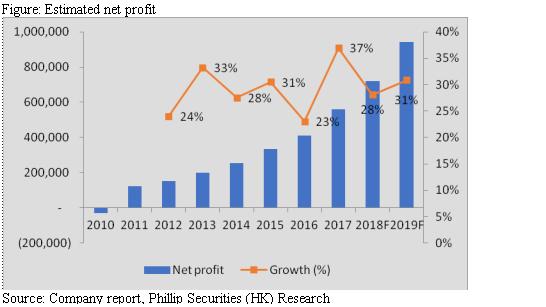

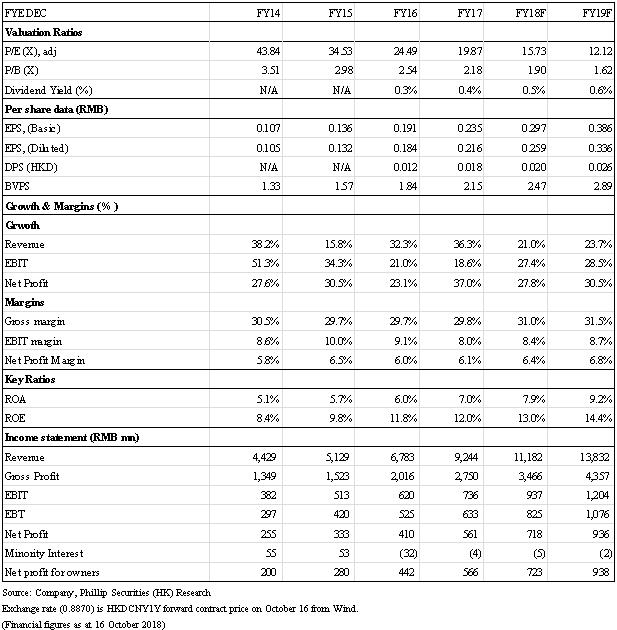

Based on the above assumptions, we expect net profit growth to be 28/31% in 2018/19, reaching RMB 720/940 million.

Valuation

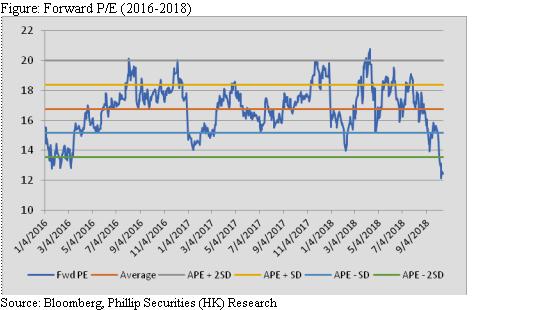

ChinaSoft is one of the leading software companies in China and has rich experience in industry solutions and software outsourcing services. At the same time, the company also has a strong customer base and is committed to developing platforms and cloud services. We believe that under the technological revolution, software market in China will continue to grow. The recent decline in stock prices has brought buying opportunities. Based on 2018 net profit, we assume a P/E ratio of 16.5x (average over the past two years), deriving a target price of HK$5.53, and a “Buy” rating with a potential return of approximately 33.3%. (HKD/CNY=0.887)

Risk

1. Slower-than-expected growth in SaaS market

2. Suddenly loss on major customers

3. New products replace the company's existing products

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()