-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Sunny Optical (2382.HK) - A full-year positive profit alert announced, and the premiumization of mobile products is expected to continue

Monday, March 17, 2025  3014

3014

Sunny Optical(2382)

| Recommendation | Accumulate |

| Price on Recommendation Date | $88.200 |

| Target Price | $97.320 |

Weekly Special - 2333 Great Wall Motor

Company profile

Sunny Optical Technology, founded in 1984, is a leading global manufacturer of optical components and products. Specializing in optical and optoelectronic product design, R&D, production, and sales, its key offerings include optical components (mobile phone lenses, automotive lenses, surveillance lenses, etc.), optoelectronic products (mobile phone camera modules, 3D optoelectronic modules, automotive modules), and optical instruments (microscopes, smart inspection equipment).

Positive profit alert for 2024

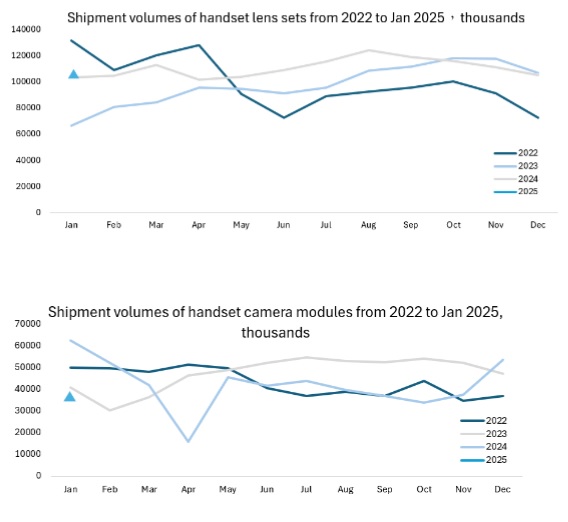

The company has issued a positive profit alert for 2024, expecting full-year net profit to reach RMB 2.64–2.75 billion, marking a YoY growth of 140.0%–150.0%, slightly exceeding market expectations. This growth is primarily driven by the recovery of the global smartphone market, with shipments rising to 1.22 billion units, strong demand for high-end models, and AI integration in smartphone hardware, resulting in a 13.1% YoY increase in mobile phone lens shipments and improved product mix, boosting ASP and gross margins. Additionally, the development of intelligent driving assistance systems increased the adoption rate of automotive lenses, with the company's total automotive lens shipments reaching 102 million units, a 12.7% YoY increase, meeting the previous guidance.

In 1H 2024, the company achieved revenue of RMB 18.86 billion (+32.1% YoY) and net profit of RMB 1.08 billion (+147.1% YoY), with robust growth across smartphone, automotive, and AR/VR businesses. Optical components revenue grew to RMB 5.48 billion (+26.9% YoY), while optoelectronic products revenue reached RMB 13.19 billion (+35.5% YoY), driven by higher sales of smartphone camera and automotive modules.

Smartphone: focus on high-end products and product mix optimization

The recovery in the smartphone segment prompted a 13.1% YoY growth in smartphone lens shipments (1.32 billion units, greater than the previous guidance) but a 5.9% decline in smartphone camera module shipments (530 million units, a bit smaller than the previous guidance) due to a strategic shift away from low-end products. The improved product mix is expected to enhance ASP and gross margins, with projected 2024 full-year revenue of RMB 12.19 billion for optical components and RMB 23.84 billion for optoelectronic products. The integration of AI in smartphones is driving smarter and more personalized devices, stimulating replacement demand and accelerating camera upgrades, creating new opportunities for the camera module supply chain.

Automotive: Strong development of new energy vehicles drives further expansion of optical product applications

According to data from the China Association of Automobile Manufacturers, in 2024, the production and sales of new energy vehicles reached 12.89 million and 12.87 million units, respectively, representing year-on-year growth of 34.4% and 35.5%. The sales of new energy vehicles accounted for 40.9% of total new vehicle sales, an increase of 9.3 percentage points compared to 2023. With the ongoing electrification, digitalization, and intellectualization of the automotive industry, the demand for cameras in intelligent driving and cabin sensing systems continues to grow, creating new opportunities for manufacturers. Additionally, market requirements for the performance and quantity of perception hardware such as in-vehicle cameras and LiDAR are increasing, further driving the expansion of optical product applications. Furthermore, in February 2025, BYD launched its "Mass Intelligent Driving" strategy, making intelligent driving systems standard across its 100,000/150,000/200,000 RMB vehicle models, with partial adoption in models below 100,000 RMB. We believe this strategy may lead a new wave of industry competition in configurations, and the company, as a leader in in-vehicle lenses, stands to benefit from the penetration of intelligent driving solutions in lower-tier markets and the advancement of high-end intelligent driving.

Company valuation

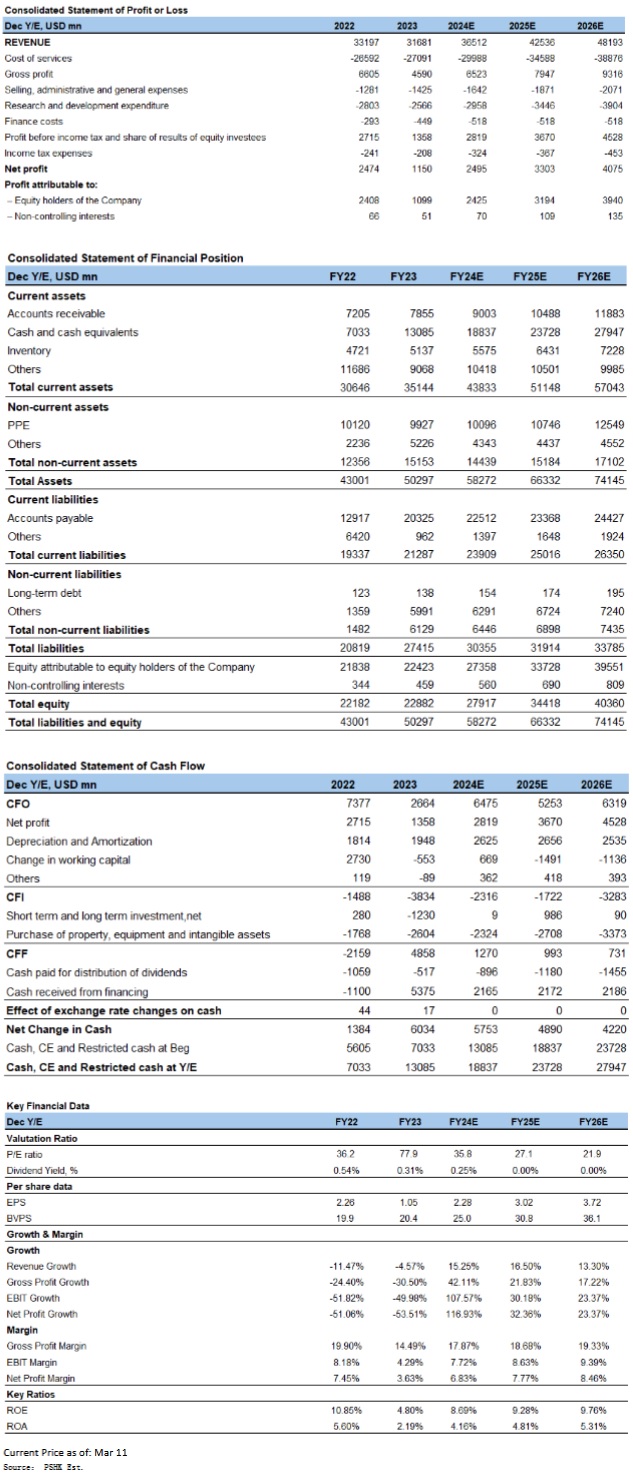

Considering the recovery in consumer electronics demand and the company's continued push towards high-end smartphone products, which is expected to optimize product portfolio, coupled with the growth in automotive products driven by the penetration of intelligent driving, we anticipate revenue growth. Therefore, we forecast the company's revenue for 2024-2026 to be 36.51/42.54/48.19 billion RMB, with net profits attributable to the parent company of 2.43/3.19/3.94 billion RMB, corresponding to EPS of 2.28/3.02/3.72 RMB. The current stock price corresponds to a PE ratio of 36.0/27.2/22.0x. Overall, given the company's solid leading position, we apply a valuation slightly above the industry average, at 30 times the 2025 PE, resulting in a target price of 97.32 HKD per share. We initiate coverage with an "Accumulate" rating.

Exchange rate: HKD/RMB=0.93

Risk factors

1) The recovery in demand for the smartphone market falls short of expectations; 2) Delays in the delivery of automotive-related projects; 3) Intensified competition in the lens industry.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()