-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Cinda Asset Management Co., Ltd. (1359.HK) - Unique business model with obvious competitive advantages

Friday, November 29, 2013  9439

9439

China Cinda Asset Management Co., Ltd.(1359)

| Recommendation | Buy |

| Target Price | $4.500 |

Weekly Special - 2333 Great Wall Motor

Company introduction

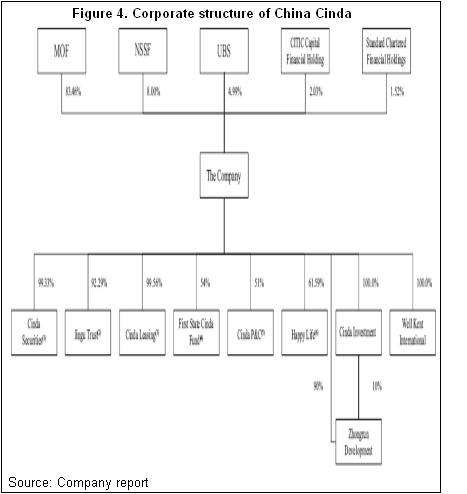

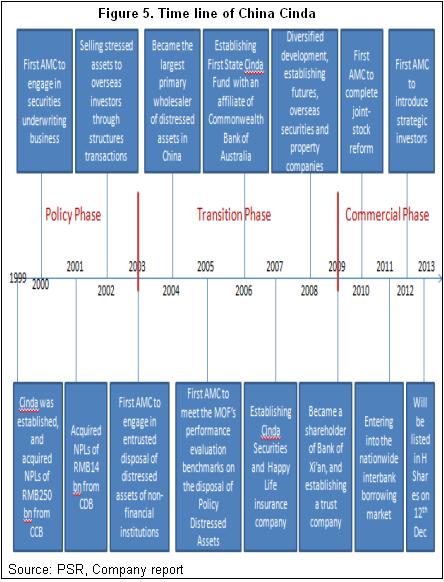

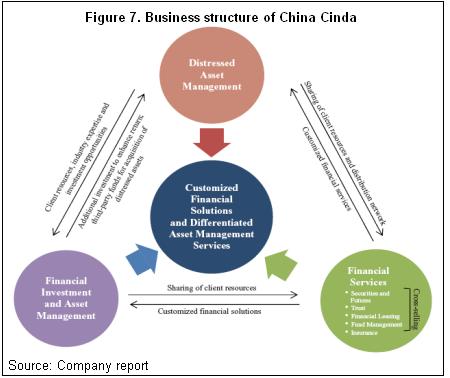

After the approval of the State Council, China Cinda Asset Management Co., Ltd was established by the MOF in Beijing on 29th June 2010. The company is the leading AMC in China, and focuses on distressed asset management and provides customized financial solutions and differentiated asset management services to the clients through the synergistic operation of the diversified business platforms. The main businesses are: distressed asset management, investment and asset management and financial services. In 2012, China Cinda introduced four strategic investors such as NSSF, UBS and so on with the total shares of 16.54%.

Summary

-China Cinda (or the Group) announced that it would make the IPO application on 28th Nov 2013, and planed to listed in H Shares on 12th Dec 2013, which is the first domestic AMC listed in Hong Kong;

-China Cinda will issue 5,318.84 million shares in H shares with the offering price range between HK$3 and HK$3.58. The funds will be used for increase the capital, 60% for expanding the core businesses, 20% for developing financial investment and asset management, and the rest for the Group's financial affiliates and improving the operating efficiency;

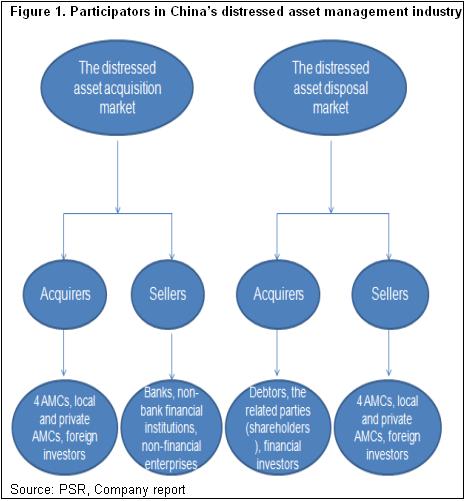

-China Cinda is the leading AMC in China, and initially aims to manage the distressed assets of China's large-sized financial institutions, mainly for state-owned banks, and therefore it has the strong governmental background;

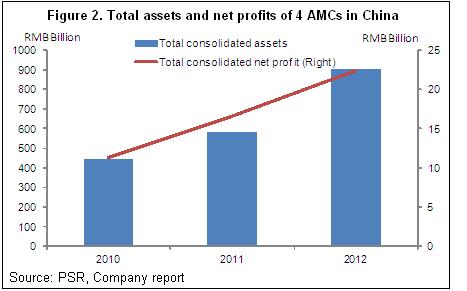

-China Cinda is the leader of China's distressed asset management industry in terms of income, profit, business scale and cash recovered. By the end of 2012, it had acquired distressed assets with an aggregate Original Value of RMB1.11 trillion, representing a market share of 35.5% among the 4 AMCs, and it also had cumulatively recovered cash in the amount of RMB276.9 billion from the disposal of distressed assets, around 38.3% among the Big-4;

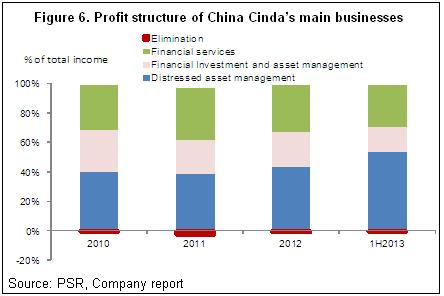

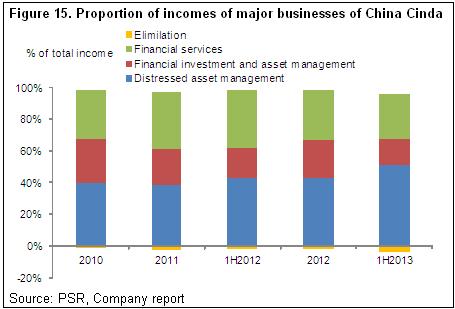

-China Cinda's main businesses include: Distressed asset management, investment and asset management and financial service, and distressed asset management is the major part, by the end of 1H2013, the proportion of the incomes of these three businesses to the Group's total income recorded 53.8%, 17.7% and 29.5%, and the EBTs of each part were 72.3%, 22.3% and 5.5% of the Group's total EBT respectively;

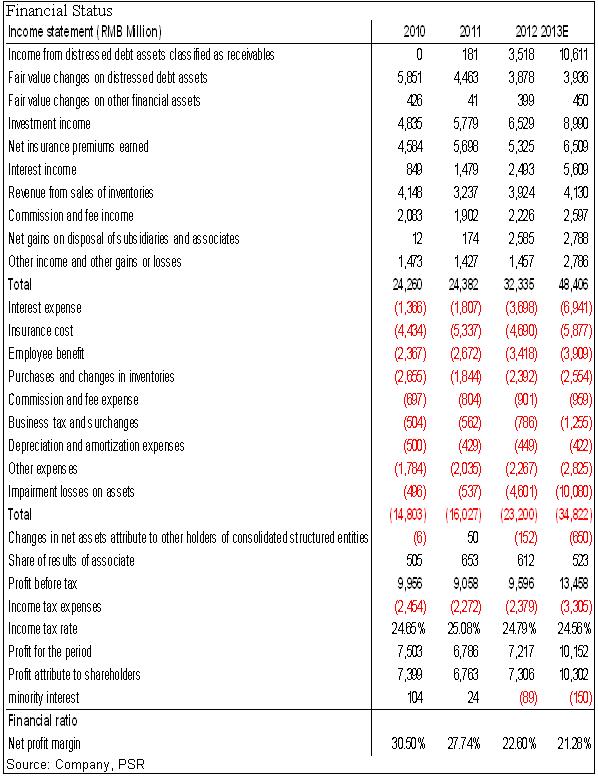

-From 2010 to 2012, the balance of the distressed debt assets, income from distressed debt assets, and investment gain from the DES Assets recorded a CAGR of 164.3%, 17.8% and 25.9% respectively;

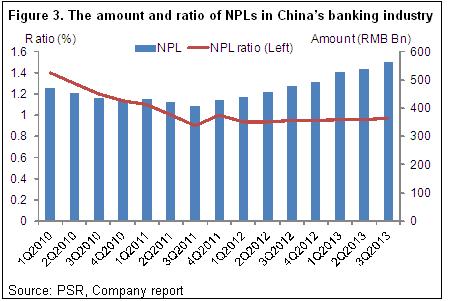

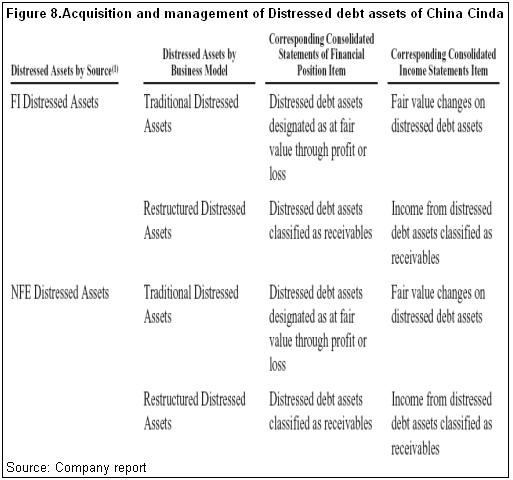

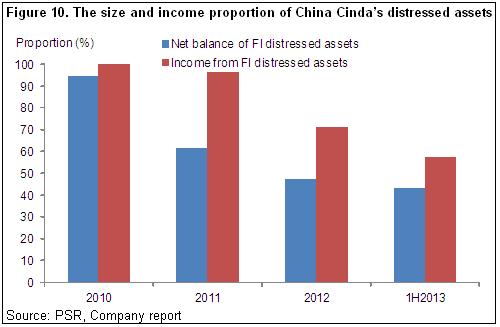

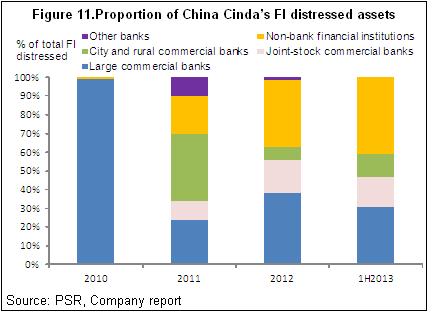

-China Cinda's FI Distressed Assets primarily include NPLs and other distressed debt assets from banks, especially from Large-sized Commercial Banks, but the proportion dropped from 98.9% in 2010 to 30.3% in 1H2013, and the portions of Small and middle-sized Commercial Banks, and City and Rural Commercial Banks appeared increase, especially the portion of other Non-bank Financial Institutions increased significantly from 1.1% to 12.6%;

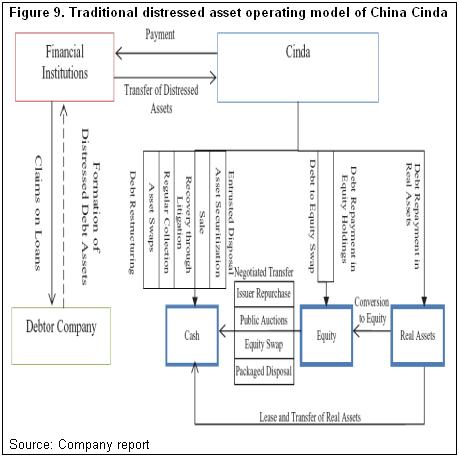

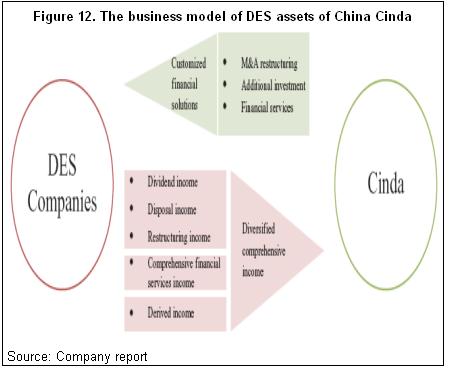

-Additionally, DES Asset Management also is one of the major businesses of China Cinda, and it gains a large amount of DES Assets primarily through D/E swap, receipt of equity in satisfaction of debt and other distressed assets related transactions, and owns diversified comprehensive income through dividend income, disposal income and restructuring income and so on;

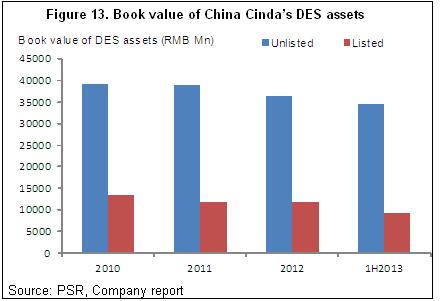

-The Group's DES Assets are mainly unlisted shares of DES Companies, by the end of 1H, China Cinda held 182 DES Companies with total book value of RMB34.38 billion and Listed DES Assets in 67 DES Companies, with total book value of RMB9.28 billion. It is worthy of noting that the calculated value of China Cinda's top 20 Unlisted DES Asssets was RMB62.3 billion from the third-party valuation specialist, compared with acquisition costs of RMB27.7 billion, representing the huge opportunity of the profitability;

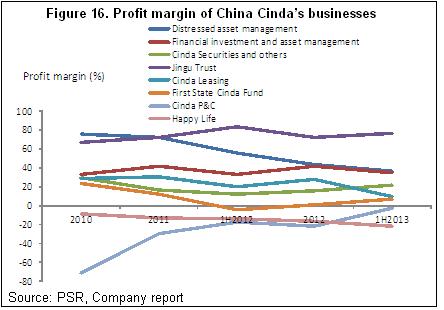

-Overall, the businesses of China Cinda increased significantly due to the rich supply in the market, and the profit maintains quite high growth rate. By the end of 1H2013, incomes of Distressed Asset Management increase strongly by 87.6% y-y to RMB10.049 billion, and the proportion up from 43.9% in 1H2012 to 53.8%. The EBT increased by 23.7% y-y approximately to RMB37.11 billion, and the proportion down to 72.3% slightly;

-We believe the performance of China Cinda will maintain stable improvement with quite high growth rate of profits, which may record the y-y growth rate of 40% approximately in net profit this year;

-It has quite large uncertainty of the performance estimation for China Cinda due to its unique and complicated operating model, which is difficult to find the benchmark, based on the current range of the offering price, equivalent to 1.1-1.3xP/B in 2013, and we think the valuation is quite reasonable considering the level of the P/Bs in current domestic listed banks and insurers. However, we have the confidence in China Cinda's future performance due to its strong shareholders` background, unique business model and obvious competitive advantages, give the 12-m target price of China Cinda to HK$4.5, around 26% higher than its upper offering price, initially recommend Buy rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()