-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Canvest Environmental Protection Group Co., Ltd. (1381.HK) - Exceptional Results with Enormous Market Potential

Thursday, July 21, 2016  27624

27624

Canvest Environmental Protection Group Co., Ltd.(1381)

| Recommendation | Buy |

| Price on Recommendation Date | $3.400 |

| Target Price | $4.700 |

Weekly Special - 2333 Great Wall Motor

Rapid Growth in Operating Results

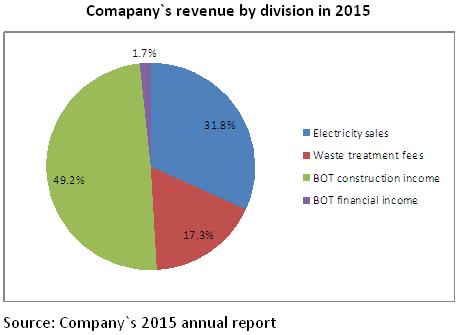

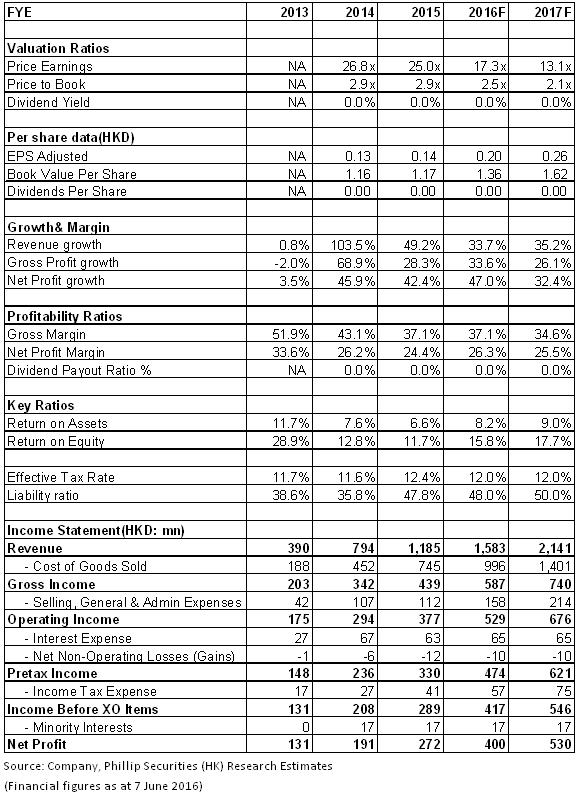

Canvest Environmental Protection Group Company Limited is a leading pure waste-to-energy (WTE) provider focused solely on the development, management and operation of WTE plants. In 2015, the revenue of Canvest amounted to HK$1.19 billion, representing a year-on-year increase of 49.2%, which was mainly attributable to the following two factors: i) The revenue derived from BOT construction of Zhanjiang WTE plants skyrocketed by 135.4%, reaching HK$580 million and accounting for 49.2% of the total revenue; ii) The efficient operations of two WTE projects Kewei and China Scivest. During the reporting period, the company processed a total of 1.5 million tones of harmless waste and achieved a total power generation of 660 million kwh.

The company's gross profit was HK$440 million, an increase of 28.3% year-on-year. Its gross profit margin dropped from 43.1% in 2014 to 37.1% in 2015, mainly because the gross profit margin of the BOT construction business (16.7%) was far lower than that of WTE electricity sales and waste processing (55.4%). During the reporting period, the company's financial expenses declined by 16.8%. Besides, net profit attributable to parent company amounted to HK$270 million, surging by 42.4% year-on-year. Basic EPS was HK$13.6 cents.

Abundant Project Reserve

The company now is present on the market in Guangdong Province, Guangxi Zhuang Autonomous Region and Guizhou Province. As at the end of 2015, the daily municipal domestic waste (MSW) processing capacity of the company's operations, together with the daily MSW processing capacity of the secured contracts, increased by approximately 80% to 12,400 tonnes on a year-on-year basis. The processing capacity of operations soared from 3,600 tonnes to 5,400 tonnes, up by 50%. In 2016, the company accelerated the pace of expansion. It successfully acquired the approved expansion of China Scivest and the acquisition of Xingyi project and obtained the BOT concession right of Beiliu WTE plant, which will further increase the total capacity to 15,700 tonnes. Rapid expansion of reserved projects will give a definite opportunity for growth in the future. Echo-Tech phase I, after technological upgrade this year, will be put into operation. In addition, Zhanjiang project began to be put into operation in Q2, making the total projects capacity surge to 7,600 tonnes per day, much larger than 2015. The company is therefore expected to record a large increase in operating result in 2016. Besides, given the increasingly intense competition in the industry over the past two years, some companies secured projects by means of lowering the waste processing fee. But the company indicated that it would not greatly cut the waste processing fee in order to acquire a certain project. The waste processing fee of projects obtained in the past 15 months was high. In some underdevelopped areas, if the price was too low, the company would not participate in the bidding.

Huge Market Potential of Technological Upgrade

In 2014, about 25% of domestic WTE plants adopted fluidized bed technology. However, since the moving grate technology is more environmentally friendly and causes fewer pollution problems, the existing WTE plants that run on the fluidized bed technology will have to undergo technological upgrade of moving grate technology. Canvest has an edge over other WTE enterprises in terms of technological upgrade market. The company has rich experience in upgrading circulating fluidized bed to moving grate with Eco-Tech and China Scivest subject to major technological upgrade. Therefore, the company has accumulated abundant experience in technological upgrade. After the upgrade, the projects of Eco-Tech and China Scivest reached an exceedingly high level of operation. The auxiliary power consumption rate is as low as 12%, well below the industry average level of 15% -18%. In this way, economic efficiency is not only greatly enhanced, but better environmental benefits are created as well. In addition, the company also plans to undertake technological upgrade of Guangxi Laibin and Guizhou Xingyi projects in order to improve its overall performance.

Evaluation

The WTE market in Guangdong Province is growing rapidly, and the compound annual growth rate of its daily processing capacity from 2015 to 2020 is anticipated to reach 18%.

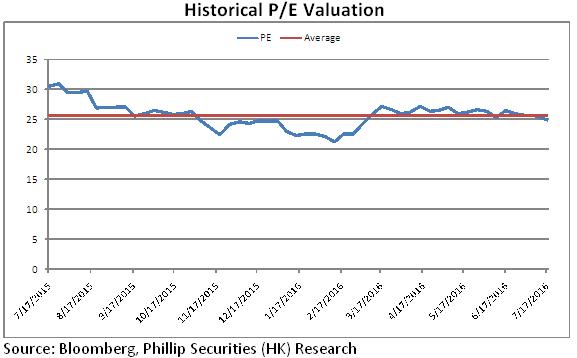

Canvest is equipped with rich experience and advantages of mature technological upgrade in respect of project implementation, so it is expected that the company will benefit from the fast-growing market of Guangdong Province. We give the company the target price of HK$4.7, equivalent to 18X P/E in 2017. The "Buy" rating is maintained. (Closing price as at 18 July 2016)

Risk warnings

New projects fell short of expectation;

RMB devaluation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()