-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Want Want China (151.HK) - Pushing innovations but not price deductions as the key to success while facing potential market challenges, entering new overseas market in Vietnam and ASEAN countries

Monday, December 17, 2018  7158

7158

Want Want China(151)

| Recommendation | Neutral |

| Price on Recommendation Date | $5.680 |

| Target Price | $6.470 |

Weekly Special - 002050 Sanhua

Investment Summary

-In the first half of the year, revenue increased by 3.2% y.o.y to RMB 9.25 billion, which is lower than the guidance of the medium to high-single-digit growth given by the management team earlier. In accordance with the old accounting standards, revenue recorded a medium-single-digit growth. Milk drinks and rice crackers businesses performed not as expected. According to the management team, there were negative impacts of product price increase in Q2, as well as the company's shipment adjustment for rice crackers. In the 1H, the contribution of new products was less than expected, accounting for only 3% of total revenue. Earlier, the guidance was higher than low-single-digit growth of previous years.

According to management, the business performance in Q3 (July-September) was similar to that in Q2, maintaining a single-digit growth. The profit margin improved compared to Q2, mainly due to the improvement in product mix that was not fully reflected in Q2.

We expect top line growth in 2H of the year to be higher than 1H. As near the Lunar new year, rice crackers business is entering peak season, the management team is doing lots of preparation works. The milk beverage is expected to be better than the first half of the year, driven by new products and base factors. The company plans to focus on the promotions of New Year products including gift packs, “Lonely God” series and jellies to start off the busy peak season.

- In 1H, benefiting from the launch of high-margin new products, as well as the price decrease in sugar, palm oil and rice in raw materials, the gross profit margin increased by 1.1 ppt to 44.5%. We expect the sugar and carton to be flat in 2H compared with 1H, and the overall raw material pressure will be flat or down. The GPM for 2H and the full year is expected to be better than 1H.

In 1H, distribution costs increased by 12% y.o.y., and as a percentage of revenue increased by 1.3ppt to 15.6% as compared to that of the same period in the previous year. It was mainly due to an increase of advertising and promotion expenses as a percentage of revenue by 0.7ppt to 3.7%, as a result of the company's increased investment in promotion resources for new products and channels.

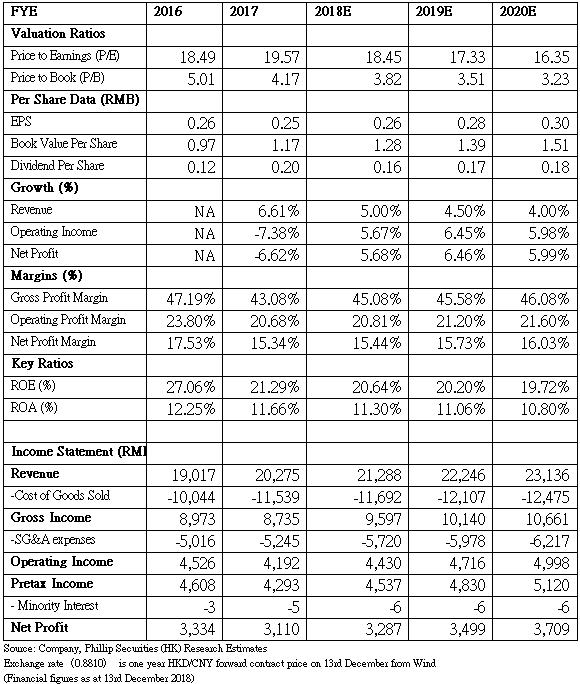

Want Want has invested in 3,000 vending machines this year, inside schools, office buildings and ect. in 34 cities. It is expected to increase to 10,000 to 20,000 vending machines in the next two years. If each machine's sales can reach RMB2,000 per month, the payback period is only about 9 months. The company will also extend its establishment in overseas market. The Vietnamese plant is expected to be put into operation in February to March in 2021. We expect this year's profit to resume growth, ending the declining trend in profits for four consecutive years since 2014. We give forecast P/E ratio 21.5 times, the corresponding target price HKD6.47. (current price as of December 13, 2018)

Business Overview

First half of the performance review

Revenue of rice crackers business declined by 0.7% y.o.y., mainly due to the sales order shipment adjustment in regions outside China which had a temporary negative impact on rice crackers export sales and the company's strategic decision to limit the low-margin sub-brand rice crackers sales from profitability consideration. However, it still achieved a single-digit growth in mainland China region. In terms of traditional channels and emerging e-commerce channels, it recorded growth too.

Revenue of dairy products and beverage increased by 2.8% y.o.y.. Revenue of “Hot-Kid milk”, which accounted for over 90% of the segment's revenue, increased by 3.3% y.o.y. while sales through all channels, including traditional channels as well as the emerging channels, also achieved growth. The company actively cooperated with major e-commerce platforms and explored emerging retail methods. Revenue of dairy and beverages through e-commerce channels continued to maintain a doubling growth momentum. Through constantly investing resources in modern channels, and the success of differentiated strategy, led to a mid-single-digit growth. Sales through traditional channels made steady progress, particularly in second-and third-tier cities.

Revenue of snack foods business increased 7.2% y.o.y. Sales of candies, its key products, achieved a double-digit growth, sales of beans, nuts and others(mainly jellies and biscuits) achieved a high-single-digit growth and sales of popsicles also enjoyed a high single-digit growth. The company launched a new popsicle product “Dongchi” during the period. It achieved revenue of over RMB100 million. “QQ gummy” achieved double-digit growth in all channels.

Expand emerging channels and digital marketing

In 1H, revenue from traditional channel recorded a single-digit growth, while e-commerce channels maintained a doubling of growth, accounting for about 5% of total revenue. The development of maternity and other emerging channels was also in swift progress.

Want Want was named as one of the top three food and beverage brands by well-known short video social media called “Douyin”. The company has carried out marketing activities towards brand rejuvenation and marketing customization in diversified forms to get closer to the young generation. After creating an online topic of “Want Want's New Products Release” on April Fools` Day, releasing serial products online including skincare products and apparels which aroused heated discussion on the internet. The jock materialized on 11th November. The products were promptly sold out after the launch.

Investment Thesis & Valuation

We expect this year's profit to resume growth, ending the declining trend in profits for four consecutive years since 2014. We give forecast P/E ratio 21.5 times, the corresponding target price HKD6.47. Potential investment risks include revenue growth or channel expansion missing expectation, raw material cost with huge volatility. (current price as of December 13, 2018)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()