-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CECEP COSTIN New Materials Group (2228.HK) - A industrial leader with stable profit growth

Friday, October 18, 2013  8324

8324

CECEP COSTIN New Materials Group(2228)

| Recommendation | Buy |

| Price on Recommendation Date | $4.230 |

| Target Price | $5.600 |

Weekly Special - 175 Geely

Company Introduction

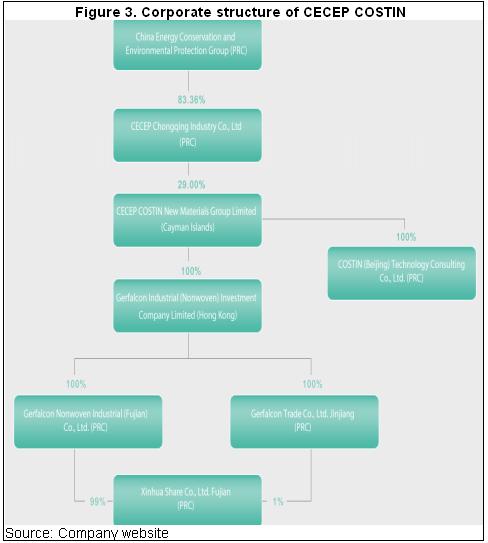

CECEP COSTIN New Materials Group Limited ("CECEP COSTIN" or "the Group"), China's first non-woven materials company listed on the Hong Kong Stock Exchange's IPO Main Board, is a pioneer in the non-woven materials industry, committed to using advanced and innovative technology for the production of non-woven materials. The Company is China's first non-woven materials company to receive the "carbon footprint" certificate, and is a SCS Recycled Environmental Protection certified enterprise, and entitled as Fabric China Pioneer Plant of Environmentally-friendly Filtering Materials. The Company's headquarters is located in Hong Kong, its manufacturing base is located in Jinjiang city, Fujian province, and its industry consultation division is located in Beijing. CECEP COSTIN's two pillar industries are the production of recycled chemical fiber using renewable materials and 3-dimension structural non-woven materials through clean manufacturing processes.

Summary

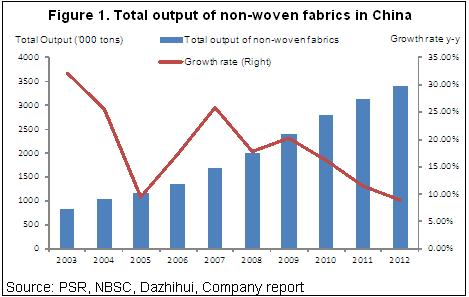

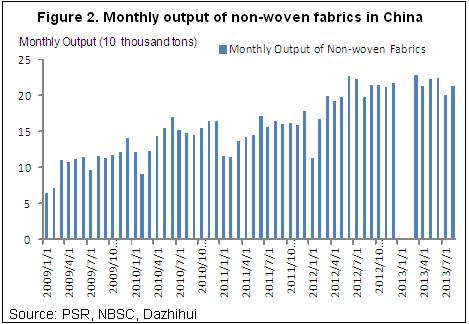

-China's non-woven fabrics industry improved consistently in recent years, by the end of 2012, we estimate total output of China's non-woven fabrics enterprises reached to 3.4 million tons, up 9% y-y approximately. According to monthly data of NBSC, the output of China's non-woven fabrics maintained on the top in 2013, which amounted to 0.217 million tons by the end of this August;

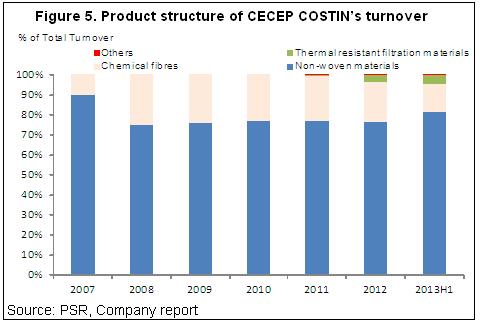

-Non-woven fabric is the main profit source of CECEP COSTIN, around 75% of total turnover. By the end of 1H2013, turnover of non-woven materials recorded RMB500 million, around 81.7% of the Group's total revenue;

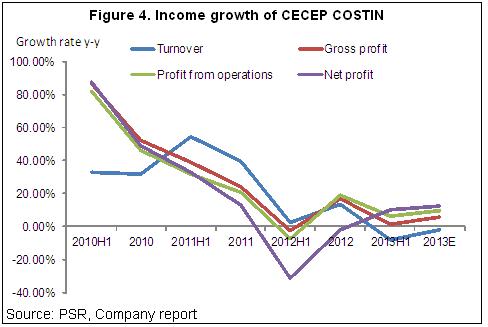

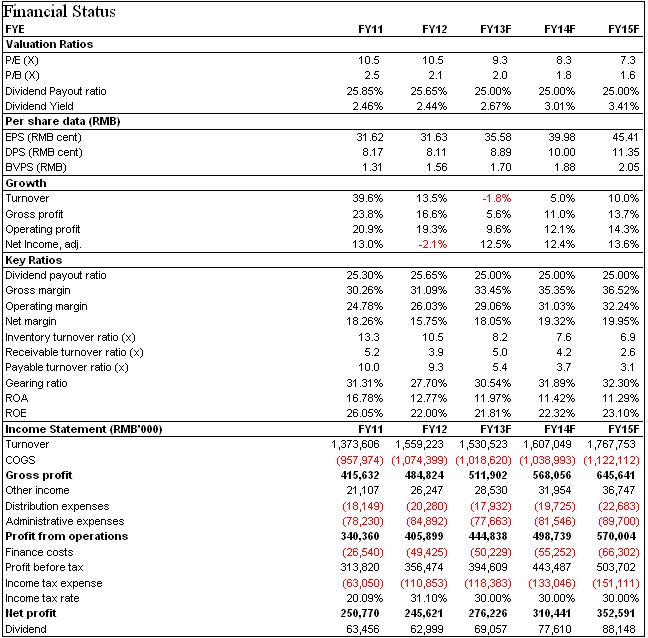

-In all, CECEP COSTIN's profit remains stable, by the end of 1H2013, the operating performance was better than that of 1H2012 obviously benefited from the efficient cost control although the Group's turnover dropped slightly. The Group's gross profit increased by 1.3% y-y to RMB201 million with net profit of RMB98 million, up 10.46% y-y compared with -31% in 1H2012;

-However, we noted that the Group's business had diversified after CECEP Chongqing became the single largest shareholder since April 2012. The major products expanded from the previous non-woven fabric and chemical fibres to thermal resistant filtration materials and other products. Especially, the revenue of thermal resistant filtration materials increased significantly from RMB4.2 million in 2011 to RMB48.6 million in 2012. By the end of 1H2013, such products` revenue amounted to RMB26.8 million, and we estimate it will up 13% approximately in 2013. Although its profits recorded the negative and we believe such relative products have wide prospect of the development in future as the PRC government raises the smoke and dust emission standards of pollutant-discharging industries;

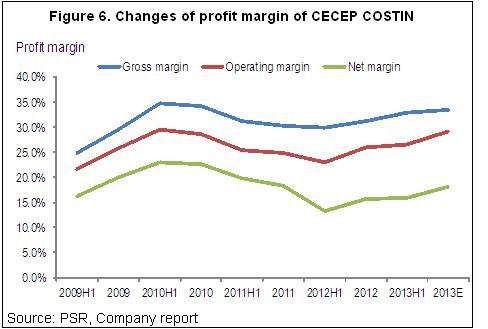

-The Group's profitability continued to increase when rhe incomes rebounded stably. By the end of June 2013, the Group's gross margin and net margin recorded 32.9% and 15.9%, up 3ppts and 2.6ppts y-y respectively;

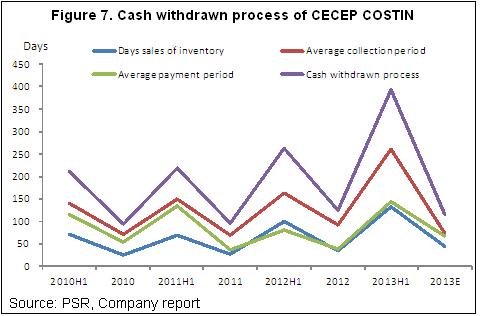

-Due to the stronger market competition and continual increase of price, the Group's operating environment faces larger challenges, and the speed of cash withdrawn slows down. By the end of 1H2013, CECEP COSTIN's inventory turnover ratio and account receivable turnover ratio were 2.7 and 1.4, down 0.9 and 0.8 y-y respectively;

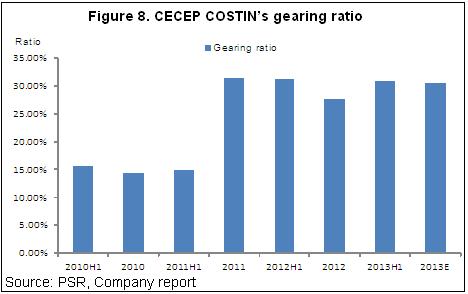

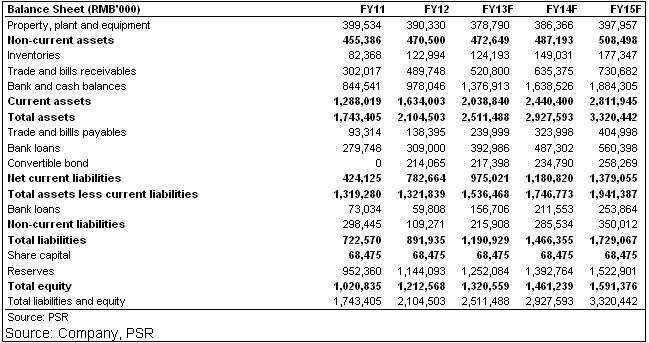

-The Group's cash flow maintains stable growth, by the end of June, the cash amounted to RMB1.237 billion, up 28.43% y-y largely. On the other hand, the gearing ratio increased from 27.7% in 2012 to 30.8%, of which the bank loans recorded RMB497 million, and 70% of such loans were the short-term loans. Therefore, we believe the Group will have capital pressure in the short run to some extent, but the debt is still at the reasonable level considering the rich cash flow;

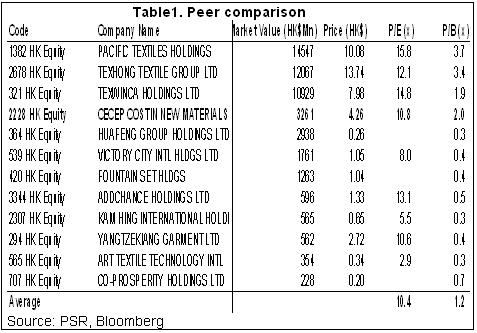

-In summary, CECEP COSTIN has quite good operating performance, and the profit grow starts to go up, and the annual performance in 2013 would be better than that of last year. Meanwhile, the synergy between the Group and CECEP began to take shape, and an annual cap of sale and supply should increase stably within the next three years. Additionally, the PRC government pays more attention to the issues of environmental protection, and announced several stimulus policies, which provides the wide prospect for the development of environmental protection companies in future. Therefore we hold the cautiously optimistic view on CECEP COSTIN's future performance, and estimate the profits will continue to increase in the next three years, and give its 12-m TP to HK$5.60, around 32% higher than its latest closing price, and equivalent to 11.0xP/E and 2.3xP/B in 2014 respectively, recommend Buy rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()