-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Le Saunda Holdings Limited (738.HK) - Take Away from FY2012 Annual Result

Wednesday, September 19, 2012  20233

20233

Le Saunda Holdings Limited(738)

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.030 |

| Target Price | $2.380 |

Weekly Special - 3606 Fuyao Glass

Company Overview

Le Saunda Holdings Limited (Le Saunda) is a Hong Kong-listed footwear retailer that applies a vertically integrated business model with a focus on Hong Kong and China markets. As of 29th Feb 2012, the Company had a network of 921 retail outlets in the China, Hong Kong and Macau. Beside, Le Saunda also undertakes OEM business.

FY2012 Annual Result Highlights

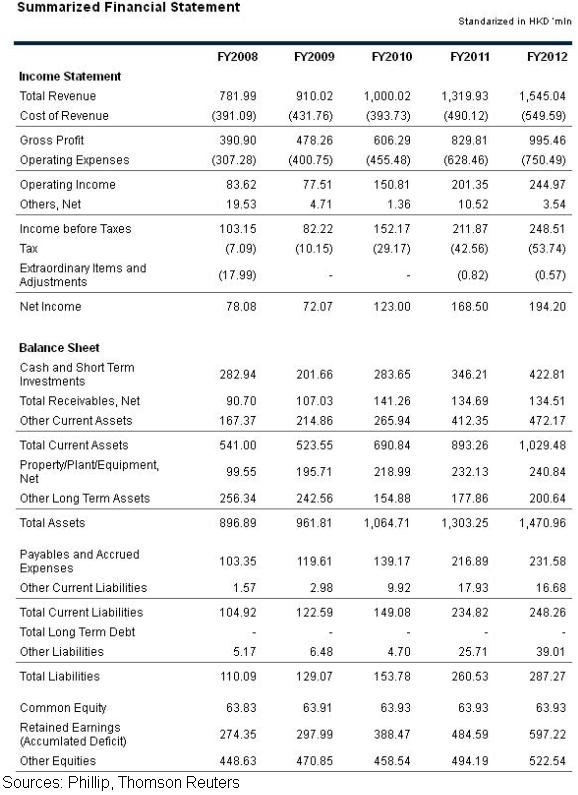

- Revenue in 2012 was HK$1,545.0 million (2011: HK$1,319.9 million), increasing 17.1% y/y.

- Gross Profit was HK$995.5 million (2011: HK$829.8 million), up 20% y/y

- Gross Profit Margin was 64.4% in 2012 (2011: 62.9%), stretching 1.5 percentage points

- The total dividend per share is HK$13.7 cents, which is 45% in terms of payout ratio

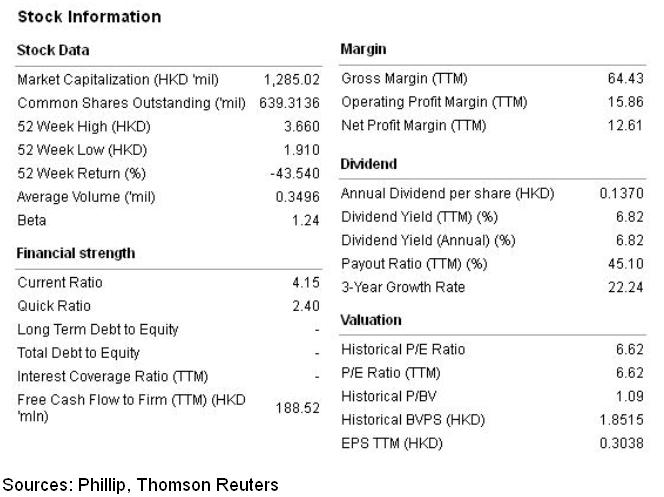

- Strong financial position with net cash 0.66 per share, improving 21.9% y/y

- Inventory was HK$433.2 million (2011: HK$386.9 million), increasing 12% y/y.

- Deterioration in export business: the group has recorded a significant drop in the export business to HK$36.1 million from HK$115.3 million in 2012. The export business only accounted for less than 3% of the total revenue

Summary

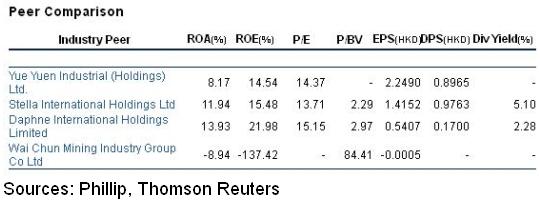

Despite the well-flagged headwinds ahead, the Company is currently trading at P/E ratio of merely 6.62x, well below the industrial average. We recommend to hold inside the portfolio for diversification, as the Company is better valued than the industrial peers possessing upside potential should the market condition turn out better than expected. The current industrial average P/E is 14.41x and we forecast that the valuation gap will be contracted by 15%, implying a trailing P/E of 7.84x and target price of HK$2.38 with 17.2% upside potential. We forecast our 12-month target price of Le Saunda be to HK$2.38 with an “Accumulate” rating.

Operation Overview

The revenue of the Company was made up of retail business and export business by which the retail business is the group's major revenue contributor accounting for 97% of the total revenue. Hong Kong & Macau and Mainland china recorded double-digit increased in revenue which was 24.2% and 25.4% respectively.

Key Take Away from FY2012 Annual Result

The management expressed that the underlying profit, which is used to measure the Company's core business performance, merely grew by 1.7% with the effect of inflation and rise in labor cost. In order to secure a high profit margin and steady growth rate in terms of revenue and ASP, the Company will extent its existing mid-to-high end business to the range of high-end market with their new brand “Linea Rosa” to the china market and the Company will source raw-material not only from external suppliers but also some high quality local suppliers for a better profit margin. Also, the Company will expand its business in the focus of the men's footwear by targeting young and stylish executive that we see is differentiate to the market competitors targeting casual and/or classic footwear market segment.

The management shares their view toward the market in the coming year amid the concern of the persisting raise in labor and rental costs and the waning consumption due to the EURO and U.S. economic woe. However, they saw China as a bright market that they believed consumers in china market with strong purchasing spree will bolster its revenue.

From our point of view, we are wary about the consumption trend in the coming year. With all the uncertainties abroad, sluggish stock and housing market internally would also affect the wealth effect of consumer and particularly harmful to higher-end consumer sector. Exporting business had literally diminished to a level we can treat Le Saunda a sheer retailer which spikes the operating risk if the retail business does not go well.

Le Saunda's financial position remains solid, cash per share was HKD 0.66 and NAV per share was HK$1.87. The Company is currently trading at HK$2.03 with trailing dividend yield of 6.82%, which makes it defensive enough to resist further tumble in share price.

The management of Le Saunda did not impress us during the presentation. They admitted that it is hard maintain the growth momentum as previous good years. However, they are satisfied with the gross margin (64.4%) and should not have problem to maintain this figure. What they will be concentrating this year is cost cutting and shutting down underperforming stores. However, they did not elaborate how they are going to implement the strategy in details. Some new stores will be opened and by the end of the year, the number of stores would increase about 5% y/y. We doubt if FY2013 will be a good time to expand further.

Summary

Despite the well-flagged headwinds ahead, the Company is currently trading at P/E ratio of merely 6.62x, well below the industrial average. We recommend to hold inside the portfolio for diversification, as the Company is better valued than the industrial peers possessing upside potential should the market condition turn out better than expected. The current industrial average P/E is 14.41x and we forecast that the valuation gap will be contracted by 15%, implying a trailing P/E of 7.84x and target price of HK$2.38 with 17.2% upside potential. We forecast our 12-month target price of Le Saunda be to HK$2.38 with an ` Accumulate ` rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()