-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Vitasoy International (345.HK) - Revenue Growth and Margin Expansion Enhance Profitability

Thursday, March 6, 2025  3078

3078

Vitasoy International(345)

| Recommendation | Buy |

| Price on Recommendation Date | $9.370 |

| Target Price | $11.660 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

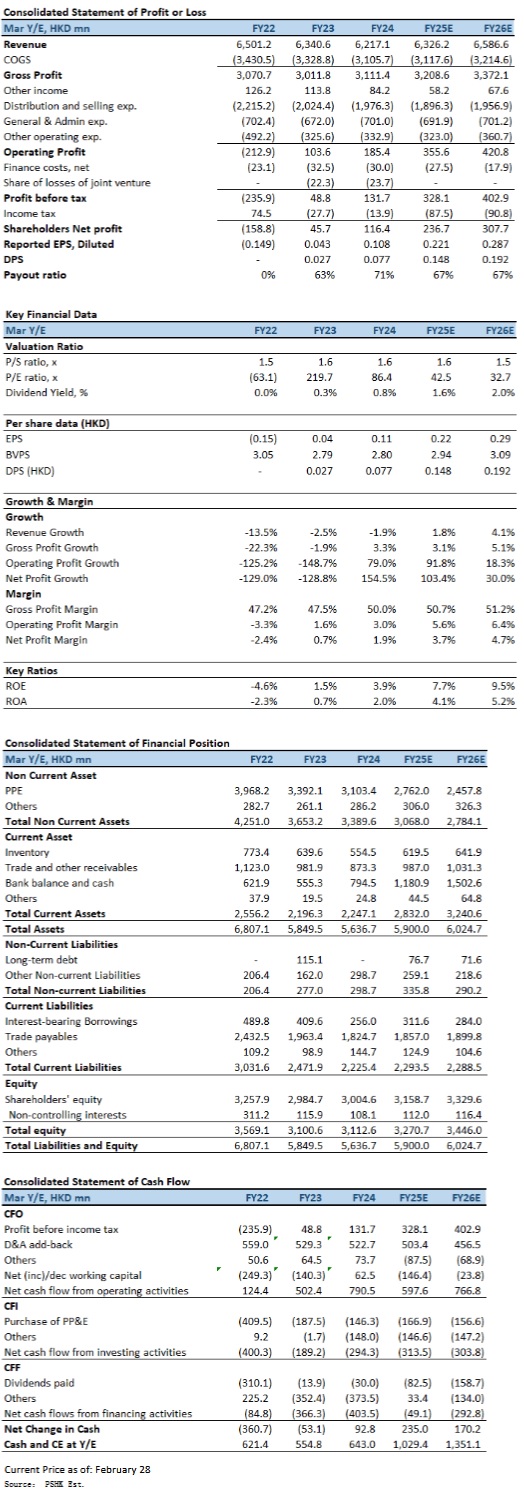

Vitasoy International (00345.HK) reported revenue of HKD 3.443 billion for 1H2025FY, representing a year-on-year (YoY) growth of 2%. While overall topline growth remained modest, gross margin expanded significantly to 51.6% (1H2024FY: 50.5%), reflecting the positive impact of lower raw material costs and production process optimization. Operating profit surged by 50% to HKD 257 million, primarily driven by strong performances in Mainland China and Hong Kong. In Mainland China, the company leveraged an optimized online and offline sales mix and improved production efficiency, leading to a 15% increase in operating profit, with an operating margin of 11%. The Hong Kong segment also delivered robust results, with operating profit rising by 44%, supported by revenue growth and lower raw material costs. Meanwhile, the Australia and New Zealand markets resumed revenue growth as production issues were resolved, while the Singapore market saw increased revenue from its tofu business, leading to a significant narrowing of operating losses. Earnings per share (EPS) stood at HKD 0.159, reflecting a YoY increase of 4.6%. The company declared an interim dividend of HKD 0.04 per share, marking an impressive 186% YoY increase. This underscores management's confidence in the company's stable cash flow outlook and its commitment to maintaining a consistent shareholder return policy.

Revenue Growth and Margin Expansion Enhance Profitability

For the six months ended September 30, 2024, Vitasoy recorded revenue of HKD 3.443 billion, up 2% YoY. The Mainland China segment remained broadly flat at HKD 1.958 billion, reflecting intensified market competition. Notably, the decline in online sales exerted pressure on overall growth, attributed to increased competition on e-commerce platforms and evolving consumer purchasing behavior. However, through product portfolio optimization and enhanced production efficiency, the Mainland China segment achieved an operating profit of HKD 218 million, up 15% YoY, with an operating margin improvement to 11%.

The Hong Kong market remained resilient, with revenue increasing by 3% YoY to HKD 1.156 billion, driven by strong brand equity, broad market influence, and product innovation. Demand for new offerings, such as Vitasoy Banana Soy Milk, Vitasoy Strawberry Soy Milk, Vita 0 Sugar Lemon Tea, and Vita 0 Sugar Sparkling Lemon Tea, was robust, boosting sales volume. Operating profit in Hong Kong surged by 44% YoY to HKD 159 million, with an operating margin improvement to 14%. This strong performance was underpinned by core product sales growth and the tailwind from lower raw material costs. Additionally, increased demand from export markets provided incremental revenue support.

The Australia and New Zealand segment resumed revenue growth, rising 7% YoY to HKD 273 million. However, the business still recorded an operating loss of HKD 45.51 million, with the loss widening compared to the prior period. This was primarily due to operational disruptions in the first half, though management has successfully resolved the issues and restored production capacity. A return to profitability is anticipated in the second half.

The Singapore segment recorded revenue growth of 6% YoY to HKD 55.85 million, primarily driven by strong tofu export demand. Despite ongoing challenges in the beverage business, operating losses narrowed significantly to HKD 2.10 million, reflecting increased tofu revenue and improved cost control measures. Nevertheless, further strengthening of distribution channels will be required to restore overall profitability in this segment.

Benefiting from lower raw material costs and production process optimization, the group's gross margin expanded to 51.6%, marking a 1.1 percentage point improvement YoY. This highlights Vitasoy's strong cost management capabilities.

Solid Financial Position with Strong Cash Flow Generation

Vitasoy's cash flow position improved significantly during the period. As of September 30, 2024, cash and bank balances (net of bank borrowings) increased to HKD 935 million, a substantial 74% surge from HKD 538 million as of March 31, 2024. This improvement was primarily driven by enhanced operating cash flow and disciplined capital expenditure management.

While bank borrowings increased from HKD 256 million to HKD 405 million, the stronger cash position allowed the company to maintain a solid financial profile, with net cash holdings improving meaningfully. This demonstrates a reduced financial risk profile and enhanced liquidity resilience.

Investment Thesis and Valuation

A key challenge for Vitasoy in the second half of the fiscal year remains the intensifying competitive landscape in Mainland China. While the company has enhanced profitability through product mix optimization and production efficiency, the decline in online sales necessitates further strategic adjustments. Strengthening brand influence and refining e-commerce strategies will be crucial to sustaining long-term growth momentum. The Hong Kong market continues to perform steadily, but given a challenging retail environment, further strengthening of market positioning and exploring additional growth avenues will be necessary. The Australia and New Zealand segment is expected to return to profitability following the resolution of production issues, while the Singapore segment's performance hinges on the successful restructuring of its beverage distribution network.

Vitasoy delivered resilient earnings growth and strong cash flow improvements in 1H2025FY, while significantly increasing dividend payouts, reflecting management's confidence in the business outlook. Despite competitive pressures in China, the company has effectively managed product portfolio optimization and cost control, leading to a notable operating margin expansion. Based on Vitasoy's robust financial position, consistent earnings growth, and stable dividend policy, and we expect the company's earnings per share (EPS) for FY2025 and FY2026 to be HKD 0.221 and HKD 0.287, respectively. Our target price is set at HK$ 11.66, corresponding to a 40.7x forward P/E ratio for FY2026, which is in line with the company's five-year historical average valuation. Our investment rating is “Buy”.

Risk factors

1) Intensified Competition in Mainland China; 2) Cost Pressures and Gross Margin Risks; and 3) Uncertainty in Overseas Market Expansion.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()