-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Meituan (3690.HK) - 4Q25 Results Exceeded Market Expectations; Increased Overseas Expansion For New Business

Wednesday, May 28, 2025  7331

7331

Meituan(3690)

| Recommendation | Buy |

| Price on Recommendation Date | $136.000 |

| Target Price | $193.000 |

Weekly Special - 2333 Great Wall Motor

Company profile

Meituan (03690.HK) was founded in 2010 and merged with Dazhong Dianping in 2015 to become China's largest comprehensive local life service platform, offering a one-stop "eat, drink, play, and entertainment" service. Through products such as Meituan, Meituan Delivery, and Dazhong Dianping, Meituan serves over 10 million annual active merchants, nearly 700 million annual active users, and over 7 million active delivery riders. The broad and deep coverage of merchants, accumulation of user data assets, and efficient delivery network form a solid moat for Meituan's business.

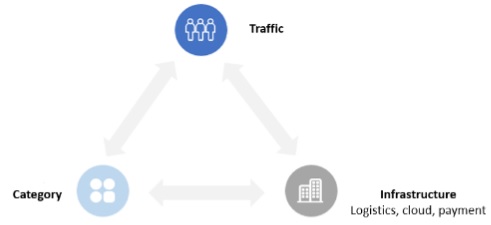

Introduce the concept of e-commerce triangle to analyze transactional platform-type companies from three perspectives

We take categories, traffic, and infrastructure as the core competitiveness of transactional platform-type companies. Meituan, as a transaction platform centered around Location (with a large offline team), leverages platforms such as Dianping and Tencent to make its online traffic more precise compared to "Ele.me". In terms of categories, local business resources and local user groups form a two-sided network, with Meituan's network effect stickiness stronger than physical e-commerce platforms like Taobao. Regarding infrastructure, Meituan has independently developed the "Super Brain" real-time delivery system, with the exclusivity of the fulfillment process and the economies of scale from order density creating core barriers that help Meituan maintain a competitive advantage as a leader in food delivery.

4Q24 Performance Exceeds Market Expectations, Share Buyback Efforts Intensified

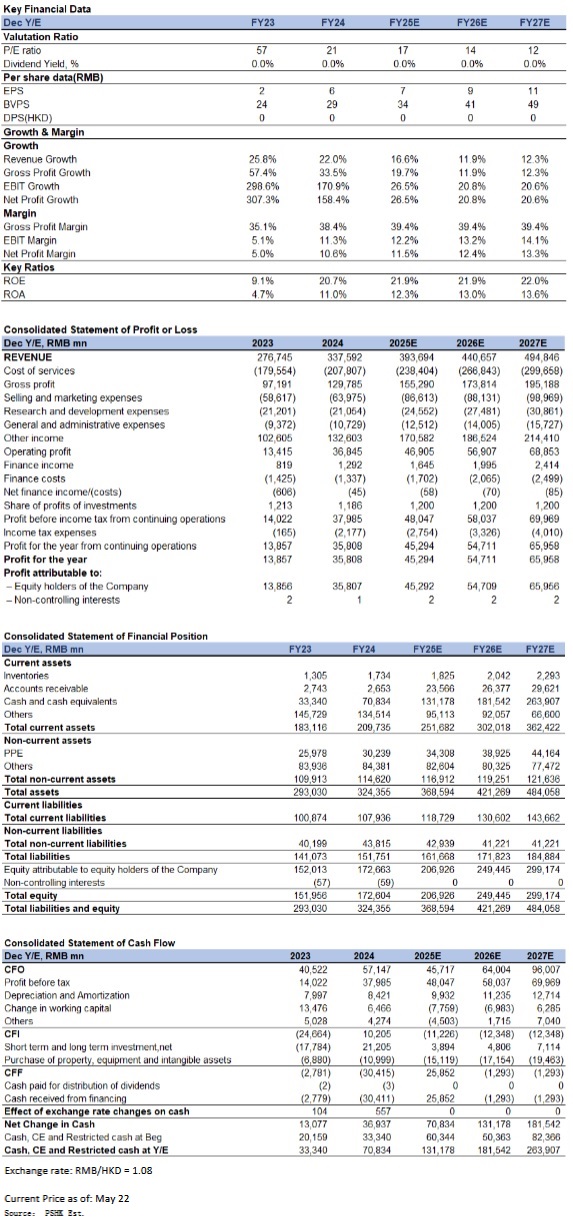

In the fourth quarter of 2024, Meituan reported total revenue of RMB 88.5 billion (Chinese yuan, same below), representing a year-on-year increase of 20.1% but a quarter-on-quarter decline of 5.4%. In terms of profitability, operating profit surged to RMB 6.7 billion, up 280.7% year-on-year, while adjusted net profit reached RMB 9.8 billion, marking a 125.1% year-on-year growth. By segment, core local commerce revenue in Q4 2024 rose 18.9% year-on-year to RMB 65.6 billion, with operating profit climbing 60.9% to RMB 12.9 billion. The new business segment generated revenue of RMB 22.9 billion, up 23.5% year-on-year, while its operating loss narrowed significantly to RMB 2.2 billion, reflecting a 55.0% year-on-year reduction in losses.

For the full year of 2024, the company achieved total revenue of RMB 337.6 billion, a 22.0% year-on-year increase. Operating profit soared 174.6% to RMB 36.8 billion, and adjusted net profit grew 88.2% to RMB 43.8 billion.

In 2025, Meituan plans to repurchase 1.5 billion worth of convertible bonds. Additionally, the company issued 2.5 billion in preferred notes at the end of 2024 to bolster its overseas cash reserves.

Core Local Commerce: Instant Delivery Services Surge, In-Store Dining & Travel Services Hit Record Highs

In 2024, China's total retail sales of consumer goods grew steadily by 3.5%. According to the National Bureau of Statistics, annual service retail sales rose 6.2% year-on-year (YoY), while catering revenue increased 5.3% YoY. For the full year of 2024, driven by higher online penetration and robust consumer demand, the core local commerce segment achieved revenue of RMB 250.2 billion, up 20.9% YoY, with operating profit surging 35.4% YoY to RMB 52.4 billion. The operating profit margin improved from 18.7% in 2023 to 20.9% in 2024. In the fourth quarter of 2024, when analyzing revenue by category, delivery service revenue reached 26.2 billion yuan, representing 19.5% year-on-year growth that outpaced order volume growth. This was primarily driven by reduced user subsidies for Shen Membership promotions and increased contribution from the 1P model boosting revenue. Commission income totaled 25.0 billion yuan, up 24.9% year-on-year, while online marketing service revenue amounted to 13.0 billion yuan, growing 17.9% year-on-year. Breaking down by service type:

Food Delivery & Instashopping Business: On the merchant side, the company launched a 1 billion yuan merchant support program in the fourth quarter, providing cash assistance and platform subsidies to help merchants improve service quality, optimize efficiency, and explore innovation. For delivery riders, the company has cumulatively provided 1.4 billion yuan in occupational injury insurance for all riders across seven pilot provinces and cities, with plans to roll out a social insurance pilot program for riders in selected cities in the second quarter of 2025, which may have a marginal impact on short-term profitability. In 2024, the company introduced the "Brand Satellite Store" rebate program covering ten thousand stores, helping chain merchants optimize their cost structures and strengthening partnerships with merchants. Meanwhile, the "Shen Qiang shou" platform addressed high-frequency promotional needs in the catering industry by launching livestreaming to complement content offerings, which is expected to enhance merchant stickiness. Considering that the expansion of Pin Hao fan's business has lowered average order values - partially offset by Meituan reducing subsidies and merchants increasing customer acquisition investments that drove advertising revenue growth, along with rising rider costs - we estimate that food delivery profit per order in the first quarter of 2025 will decline year-on-year. However, we expect this situation to ease over the next few quarters as reduced user subsidies and increased advertising revenue help normalize the comparable base. Therefore, we forecast that daily food delivery orders in 2025 could reach 57.71 million, with operating profit per order potentially reaching 1 yuan. At the same time, considering that changes in the competitive landscape in early 2025 may lead the company to increase subsidies, we predict that food delivery revenue growth may experience a short-term year-on-year decline.

Regarding the Instashopping business, as of the end of 2024, Meituan Instashopping has established partnerships with over 5,600 large chain retailers, 410,000 local small merchants, and more than 570 brands. Its warehouse network now covers more than 200 cities nationwide, with the number of warehouses exceeding 30,000 and daily order volume surpassing 10 million orders. We believe that although the weak macroeconomic environment may impact consumption, the company's accumulated experience from past operations and its deepening collaboration with all participants in the ecosystem will help explore more growth opportunities.

In-store and Travel Business: According to management, Meituan's in-store dining, hotel, and travel business achieved over 65.0% year-on-year growth in annual order volume, with both annual transacting users and active merchants reaching record highs. While the expansion of the direct sales model to more cities has impacted short-term profitability due to one-time investments, it has simultaneously increased penetration in lower-tier cities and created cross-selling synergies with food delivery services by extending membership benefits from delivery programs to in-store scenarios. Additionally, the company continues to enhance marketing capabilities for merchants by increasing livestreaming frequency, expanding city coverage, and conducting integrated online-to-offline promotional campaigns. These efforts have reinforced users` perception of the platform's high cost-performance ratio. With the competitive landscape stabilizing and strategic changes beginning to yield results, management remains optimistic about the segment's long-term gross GTV growth. Consequently, we project the in-store dining, hotel, and travel business will maintain healthy revenue growth in 2025, with an estimated year-on-year increase of 17.0%.

New Business: Overseas Expansion Leads to Sequential Increase in Losses

In 2024, the New Initiatives segment reported revenue growth of 25.1% year-on-year to RMB 87.3 billion. Operating losses narrowed to RMB 7.3 billion, with the operating loss margin improving to 8.3%, primarily driven by enhanced operational efficiency.

In the fourth quarter of 2024, revenue from the New Initiatives segment increased by 23.5% year-on-year to RMB 22.9 billion, though the growth rate slowed compared to the previous quarter, as contributions from overseas operations remained relatively limited at this stage. Operating losses narrowed by 55.0% year-on-year to RMB 2.2 billion but expanded sequentially, mainly due to the costs associated with overseas expansion. Keeta has expanded to all major cities in Saudi Arabia, with increased investments driving rapid order volume growth. However, given JD.com's entry into the food delivery market, Meituan may further ramp up its investments, putting short-term profitability under pressure.

Company valuation

Meituan is a leading internet services platform that adopts a "Retail + Technology" strategy. The company has maintained its leading position in food delivery, achieved manageable competition with Douyin in local in-store services, expanded through its comprehensive city-level business model, and possesses a strong balance sheet. We project the company's 2025-2027 operating revenues to reach 393.7/440.7/494.8 billion yuan respectively, with net profits attributable to shareholders of 45.3/54.7/66.0 billion yuan, corresponding to EPS of 7/9/11 yuan.

Based on our SOTP valuation methodology, we estimate Meituan's total target market capitalization at 1,106.2 billion yuan for 2025, with a target price of HK$193. At current share price, the implied 2025-2027 P/E multiples are 17x/14x/12x. We initiate coverage with a "Buy" rating. The company's segment valuation comprises the following components:

1)Core Local Commerce is valued at 872.8 billion yuan, using an 8% weighted average cost of capital and 5% perpetual growth rate;

2)New Initiatives are valued at 102.2 billion yuan, applying a 1x 2025 P/S multiple;

3)Net cash amounts to 131.2 billion yuan.

Risk factors

1) New business performance below expectations; 2) Intensified competition in the food delivery and travel industries; 3) Weaker than expected recovery in consumer demand.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()