-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

陶然女士 (Megan Tao)

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

分析師

本科畢業於新南威爾士大學會計金融系,碩士畢業於香港大學金融系。現為輝立証券持牌分析師,主要負責TMT及半導體板塊的研究,曾在證券公司和家族辦公室工作。

| Phone: | 22776515 | Email: | megantao@phillip.com.hk | |

BANK OF CHINA (3988.HK) - Other non-interest income increased strongly, and the scale of assets and liabilities grew steadily

Thursday, January 9, 2025  2311

2311

BANK OF CHINA(3988)

| Recommendation | Accumulate |

| Price on Recommendation Date | $3.790 |

| Target Price | $4.430 |

Weekly Special - 175 Geely

Overview

Bank of China (3988.HK) has institutions in mainland China and 64 overseas countries and regions. BOC HK and BOC Macau serve as the local note-issuing banks. Bank of China has a relatively comprehensive global service network. It has formed a comprehensive financial service system which takes the commercial banking businesses such as corporate finance, personal finance and financial markets as the main body and covers multiple fields such as investment banking, direct investment, securities, insurance, funds, aircraft leasing, asset management, financial technology and financial leasing. Bank of China provides customers with financial solutions of "one-point access, global response, and comprehensive services."

Q3 Performance review

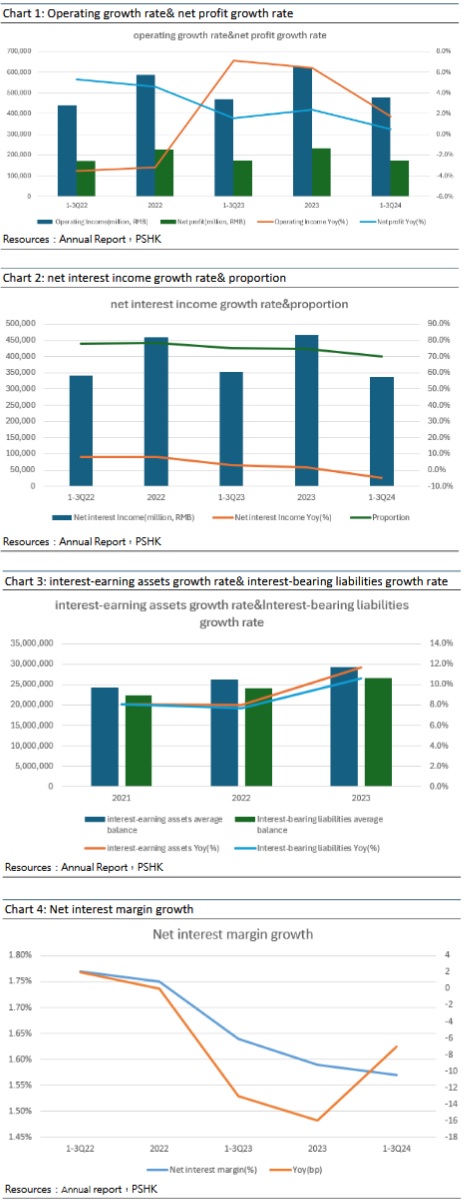

In the first three quarters of 2024, the company achieved operating income of 479.1 billion yuan (RMB, the same below) with a year-on-year increase of 1.74%; after-tax profit was 187.5 billion yuan with a year-on-year increase of 0.53%; net profit attributable to the parent company was 175.8 billion yuan with a year-on-year increase of 0.52%; basic earnings per share was 0.55 yuan.

Other non-interest income increased strongly.

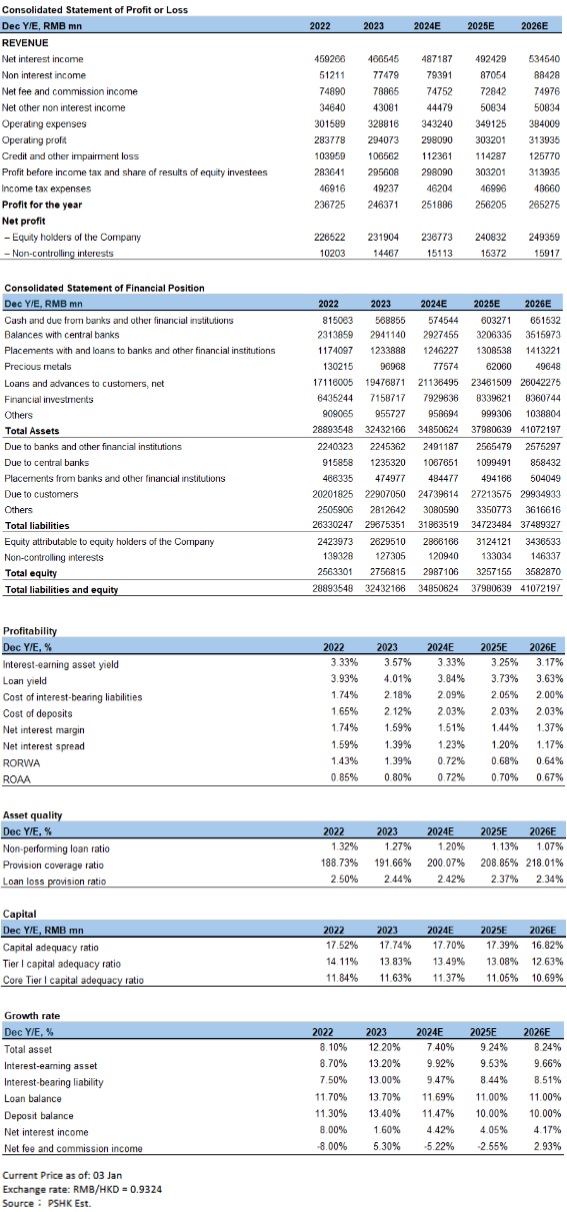

The company's net interest income in the first three quarters of 2024 was 336 billion yuan with a year-on-year decrease of 4.81%, mainly due to the net interest margin decrease slightly to 1.41% compared with the first half of the year, as the U.S. dollar faced with interest rate cut cycle, which reduced the contribution of foreign currencies to the net interest margin. In the future, factors such as existing mortgage interest rates and LPR cuts will continue to put pressure on domestic asset yields, but the slowdown in interest rate cuts by the Federal Reserve may relieve the pressure on overseas asset yields. The company's non-interest income was 143.1 billion yuan with a year-on-year increase of 21.32% which showed strong growth in non-interest businesses. Among them, net fees and commissions were 60.7 billion yuan with a year-on-year decrease of 3.93%, the decrease narrowed compared with 2024H1, mainly due to the impact of capital market fluctuations; other non-interest income (mainly including net transaction income, net income from financial asset transfers and other operating income) were 82.4 billion yuan with a year-on-year increase of 50.43%, mainly due to a year-on-year increase of 114.2% in investment income. The company's operating expenses were 172.7 billion yuan with a year-on-year increase of 10.13%. The company's impairment losses on assets amounted to 85.8 billion yuan with a year-on-year decrease of 5.78%, of which credit impairment losses amounted to 85.7 billion yuan with a year-on-year decrease of 5.86%.

The scale of assets and liabilities grew steadily, and the provision coverage ratio was at a good level.

As of the end of September 2024, the company's total assets amounted to 34,069 billion yuan, an increase of 5.05% from the end of 2023. The total liabilities amounted to 31,195 billion yuan, an increase of 5.12% from the end of 2023. Total customer deposits amounted to 23,710.6 billion yuan, an increase of 3.51% from the end of 2023, among which, corporate deposits amounted to 11,512.6 billion yuan, personal deposits amounted to 11,476.8 billion yuan, and certificates of deposit and other deposits amounted to 386.1 billion yuan. The asset and liability structure was relatively stable, with the ratio of deposits to liabilities being 76.01%, a decrease of 1.18 percentage points compared with the end of 2023. The company's loans and advances to customers amounted to 21,435.9 billion yuan, an increase of 7.38% from the end of 2023, among which, corporate loans amounted to 14,596.5 billion yuan and personal loans amounted to 6,783.3 billion yuan. The company's main risk indicators performed steadily, and its risk compensation capabilities continued to improve. The company's reported non-performing loans amounted to 270 billion yuan, and the ratio of non-performing loans to total loans was 1.26%, a decrease of 0.01 percentage point compared with the end of 2023. The ratio of allowance for loan impairment losses to non-performing loans was 198.86%, an increase of 7.20 percentage points compared with the end of 2023, the ratio was at a good level closing to 200.00%, which effectively proved that the company tried its best to deal with non-performing assets.

Company valuation

Over the past 12 months, the company's dividend yield was 6.84%, indicating a high dividend feature. The company maintains a leading global advantage, with overall stable fundamentals. Considering that non-interest income growth is slightly better than previously expected, we are optimistic about the company's medium to long-term growth. However, considering the risk of RMB depreciation affecting Hong Kong stocks significantly, and the fact that the company's main customers are physical economy enterprises, the performance may be affected by US tariffs. Therefore, we expect the company's net profit attributable to the parent company for 2024-2026 to be 236.8/240.8/249.4 billion yuan, with predicted EPS of 0.75/0.77/0.80 yuan respectively. The current stock price corresponds to PB ratios of 0.44/0.41/0.38x. Overall, we assign the company a 0.5x PB for 2024, corresponding to a target price of HKD 4.43 per share, with an "Accumulate" rating.

* The analyst has a financial interest in the listed corporation covered in this report.

Charts:

Risk factors

Overseas macroeconomic affects the company's asset quality, interest rate risk, and credit risk.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()